On November 4, 2019, Gov. Brian Kemp and the Georgia Department of Community Health released two new health care proposals: draft applications for an 1115 Medicaid waiver and a 1332 state innovation waiver. The 1115 Medicaid waiver focuses on coverage options for people with incomes below the poverty line ($12,000 for an individual or $20,000 for a family of three), and the 1332 waiver focuses on private insurance options for people making above the poverty line.

The public comment period for both waivers opened on November 4, 2019, and will end on December 3, 2019. Public comments can be submitted here. The state is planning to respond to themes from these comments and finalize the waiver by Dec. 11, with a targeted date for submission on December 20, 2019.

These waiver plans were meant to expand eligibility for Medicaid coverage to Georgians living in poverty and stabilize the individual health insurance market through a reinsurance program. However, the full details reveal that, under the state plans, only a small fraction of people would be eligible for coverage, and efforts to stabilize the marketplace could be undermined by shifting healthier people to plans with fewer benefits, leaving people who need comprehensive benefits like prescription drugs and mental health care with higher premium costs.

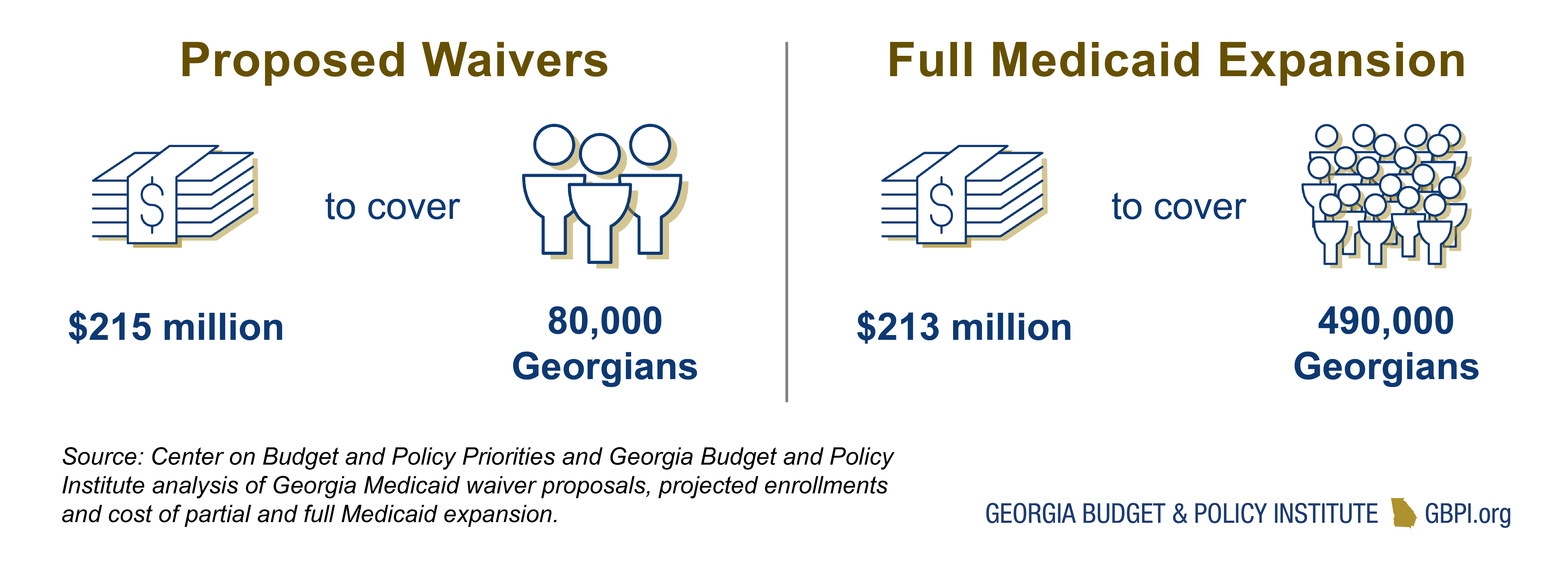

The following analysis provides a summary of each draft waiver plan and some potential effects of these proposed changes for Georgians seeking health coverage. These two waivers will cost the state about $215 million to cover roughly 80,000 people. This is compared to about $213 million to fully expand Medicaid coverage to at least 490,000 people. The state innovation waiver could also leave people paying higher premiums for health coverage by shifting people to skimpier plans and capping the availability of premium subsidies many Georgians need to afford their private health coverage.

Overview of the Waiver Proposals

Overview of the Waiver Proposals

Section 1115 Medicaid Waiver Summary

As proposed, the 1115 waiver creates a new eligibility category for Medicaid. Enrollment would begin on July 1, 2021. To qualify for Medicaid under the new criteria, you must not currently be eligible for Medicaid in Georgia. You will also need to be a U.S. citizen between ages 19 and 64, with income below 100 percent of the federal poverty line ($12,000 a year for an individual or $26,000 for a family of four) and the ability to document that you are working or engaged in a qualifying activity for at least 80 hours a month. The qualifying activities are full- or part-time employment, on-the-job training, job readiness, community service, vocational educational training and full-time enrollment in a higher education institution. Enrollees will be required to report their hours to the state each month along with supporting documentation such as a paystub or transcript. Medicaid coverage will be suspended the first month the reporting requirements are not met. If the reporting requirements are not met after three months, the person would lose their health coverage.

How much will enrollees be expected to pay for coverage?

Under the current proposal, people making between 50 and 100 percent of the federal poverty line will have to pay monthly premiums ranging from $7 to $11 a month. Coverage is suspended after two months of a missed premium. After three months of non-payment, the person is disenrolled. Copayments are also required for those who pay premium, and ranges from $0 for primary care up to $30 per visit for non-emergency use of the emergency department. Together, copayments and premiums must not exceed 5 percent of an enrollee’s income. Copayments will be paid out of a member rewards account funded by the premiums and any points enrollees are awarded for certain activities like completing annual well care visits or maintaining a certain body mass index range.

What benefits are included?

The current plan includes current Medicaid benefits, except for non-emergency medical transportation and certain vision and dental services for 19- and 20-year-olds. If an enrollee has a health insurance offer through their employer, the state will determine if it is more cost-effective for the person to enroll in their employer plan (with the state covering premiums and providing cost-sharing assistance) rather than Medicaid. In this case, the benefit package varies by employer.

Section 1332 State Innovation Waiver Summary

Phase One: Reinsurance Program

Reinsurance programs use public funding to help cover some costs associated with people who have high health care expenses. By reducing the claims expenses for the highest-cost enrollees, insurers are protected from losses and can reduce their overall premiums. Because reinsurance programs reduce premium costs, the federal government spends less on tax credits. These savings, known as federal pass-through funding, can be passed on to states, which can then use the funding to help pay for the costs of running the reinsurance program.

The current 1332 proposal would create a reinsurance program starting January 1, 2021. The reinsurance program will pay insurance companies a percentage of the claims costs for their enrollees who have claims between $20,000 and $500,000. The percentage of claims paid will be higher in regions of the state with higher premium costs. This includes some of the more rural counties in Georgia. According to the state’s analysis, premiums in the individual marketplace are expected to be reduced by an average of 10 percent statewide. The estimated reductions by region range from 5 percent to 25 percent.

Phase Two: Georgia Access

The second phase would start in the 2022 plan year, with open enrollment beginning November 1, 2021. In the current proposal, this phase transitions the individual health insurance market from the federal exchange (healthcare.gov) to a state-based model called Georgia Access. Georgians would no longer be able to enroll for coverage through healthcare.gov and the federal premium subsidies that most current marketplace enrollees receive would now be managed by the state. Instead of a centralized enrollment platform, consumers would buy their plans from web brokers or directly from insurance companies. Outreach and enrollment will be conducted by these private sector entities. The structure of the subsidies will be the same in the first year but could change in future years. The state will have a cap on subsidy spending, so if more people are eligible for subsidies than expected, they will be placed on a waiting list.

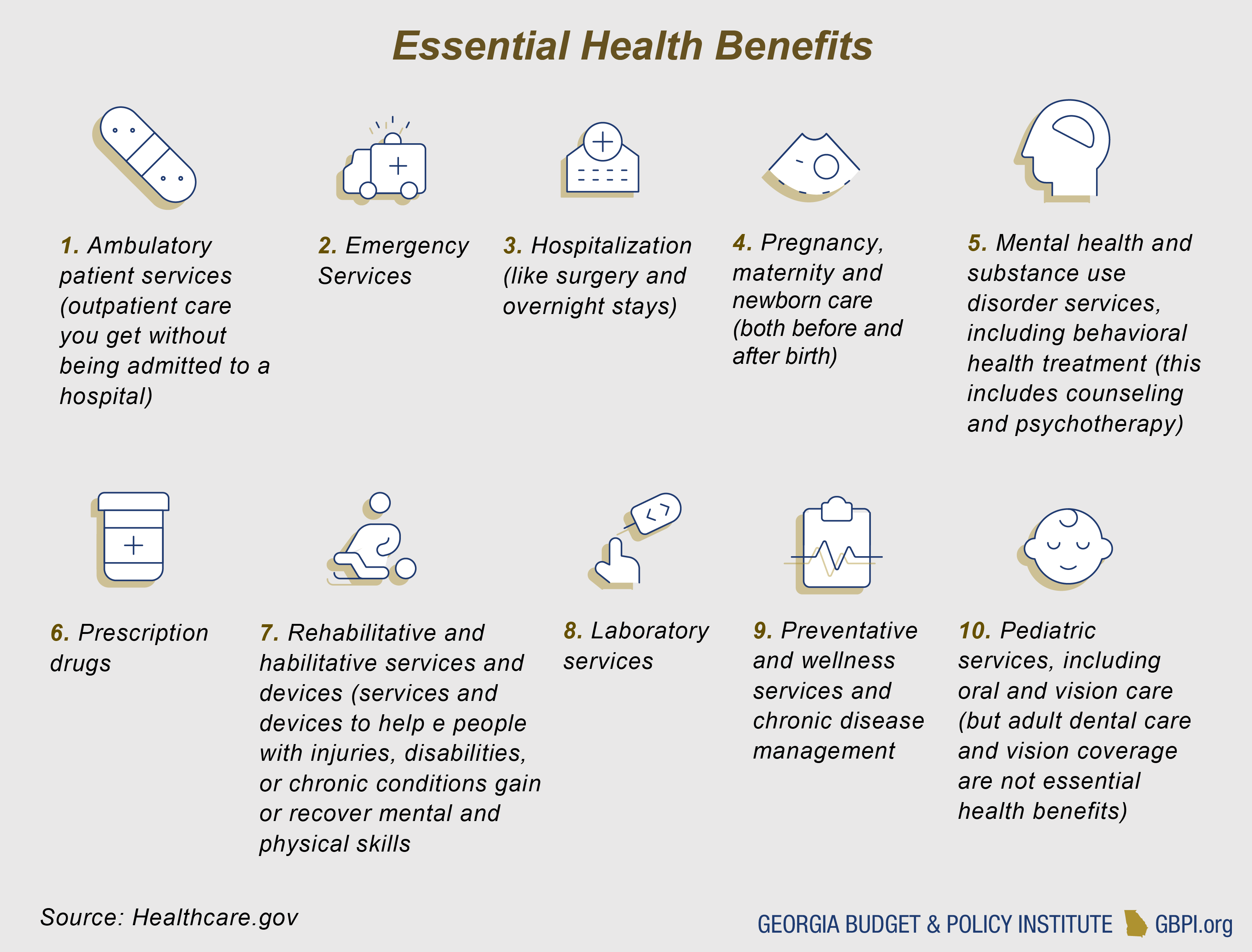

The second biggest change in this phase is allowing the premium subsidies to be used to purchase non-comprehensive health insurance plans, such as association health plans and short-term plans. If the proposal goes into effect, plans will maintain protections for people with pre-existing conditions, but they will not be required to cover all the essential health benefits that people with pre-existing conditions typically need. Many of these plans do not cover prescription drugs, maternity care, substance abuse treatment or mental health care. Additionally, by waiving the section of the Affordable Care Act requiring states to have health care exchanges (Section 1311), the state aims to waive the mental health parity requirements for comprehensive Affordable Care Act compliant plans. Mental health parity requires health insurance plans to cover mental health and substance abuse treatment at the same level as physical health treatment.

Proposed Waivers Cover a Limited Number of Georgians

Gov. Kemp stated that 408,000 Georgians living under the poverty line that do not currently qualify for Medicaid would have the opportunity to get health insurance through the Georgia Pathways 1115 waiver. However, the state estimates show that only 25,028 individuals would be enrolled at the beginning of the first year of the program. By the end of year five, the state only expects 52,509 people to be enrolled.

This means that, of the 408,000 uninsured Georgians under the poverty line, the state is expecting only about 13 percent of them to meet the work eligibility requirement of 80 hours a month. However, the state acknowledges in the 1115 application that 60 percent of uninsured Georgians over age 16 are employed at least part-time. Given these low enrollment estimates, it is very likely that the costs will be much higher than proposed, although it is unclear how many people who are employed would struggle to adequately report their work. Below is an outline of the enrollment estimates and costs of both waivers as stated in the draft application plans.

Georgia Expects to Spend $215 Million in 2022 to Cover Only About 80,000 People

| Medicaid 1115 Waiver | 1332 Private Insurance Waiver | Combined Both Waivers | |

| Estimated enrollment increases in 2022 | 47,362 | 32,444 | 79,806 |

| State cost in 2022 | $66,398,458 | $149,000,000 | $215,398,458 |

Source: Draft waiver applications posted by the state on November 4, 2019

When Georgia leaders decided to pursue a partial Medicaid expansion, the state took a risk by trying to receive the 90 percent federal match that typically only comes with a full Medicaid expansion. This year, after Utah submitted a similar plan, the federal government stated they will not be approving partial Medicaid expansions at the 90 percent matching rate. Georgia is still aiming to get this approval but is budgeting to only receive the state’s regular 67 percent matching rate.

Fully expanding Medicaid and receiving the 90 percent match is still an option that can receive federal approval. Georgia is currently one of only 14 states that has not expanded Medicaid. To pursue this, Georgia lawmakers would need to amend the Patients First Act to change the Medicaid income eligibility from 100 percent to 138 percent of the federal poverty line. With the additional federal money, Georgia could extend coverage to hundreds of thousands more people than under the current proposed waiver. This would also make a greater dent in the state’s high uninsured rate and bring significantly more revenue to hospitals and health care providers across the state.

Georgia Could Cover Over 400,000 More People for the Same or Less Cost by Fully Extending Medicaid Eligibility

| Both Proposed Waivers | Full Medicaid Expansion | |

| Estimated enrollment increases in 2022 | 79,806 | 486,503 |

| State cost in 2022 | $215,398,458 | $213,100,000 |

Source for full Medicaid expansion numbers, using the lowest enrollment estimate and the highest net state cost estimate: Georgia Department of Audits and Accounts Fiscal Note on HB 37 (LC 46 0015)

Georgians Seeking Comprehensive Private Health Insurance Coverage Could Face Higher Costs

One of the goals from the draft 1332 waiver application is “to spur innovation while not eroding the availability and affordability of QHPs.” QHPs are qualified health plans, which are the plans compliant with ACA protections and include the ten essential health benefits. The proposed changes in this waiver are likely to work against this goal and result in the qualified health plans becoming more expensive. The waiver allows people to use their premium subsidies to purchase non-qualified health plans. These plans do not have to cover all the essential health benefits. Because of this, the plans are expected to have premiums that are about 10 percent lower than the comprehensive qualified health plans. People with fewer health concerns could be steered towards these plans because of the lower cost, which would drive up costs for people who need to have comprehensive plans.

People could also face higher costs as the result of a cap the state plans to put on the premium subsidies. If more people use the premium subsidies than expected, additional enrollees would be able to enroll in plans but would only receive subsidies if more state funding becomes available. This includes people who would have otherwise been eligible for subsidies under the current federal structure. By capping the subsidies, there is a risk that some people could face higher premiums as a result of not receiving the subsidies they are qualified for.

Recommendations

Even after the state has spent years—and millions of dollars—talking about and looking into Georgia’s health care problems, these proposals do not come close to fully addressing the state’s health care crisis. These proposals are unlikely to stem the closure of rural hospitals. The state is required to solicit public feedback on these drafts, so there is opportunity for them to make changes to these proposals based on comments they receive. The public comment period for both waivers opened on November 4, 2019 and will end on December 3, 2019. Public comments can be submitted here. The state is planning to respond to themes from these comments and finalize the waiver by December 11, with a targeted date for submission on December 20, 2019.

State leaders must consider some key recommendations to make sure these proposals take a more significant and cost-effective step to cover more Georgians and pursue efforts to strengthen, not undermine, the private health insurance markets.

Section 1115 Medicaid Waiver Recommendations

- Amend the Patients First Act to allow the state to fully extend Medicaid eligibility and qualify for the 90 percent federal match. This would allow to state to cover over 400,000 more people at a lower cost than the proposed waivers.

- Invest in workforce development for enrollees to meet the goal of increasing the number of people employed or engaged in employment-related activities instead of making people report qualifying activities as a condition of getting health care.

- Include all traditional Medicaid benefits, specifically non-emergency medical transportation, to help enrollees with transportation barriers get to their appointments.

- Allow for retroactive coverage and hospital presumptive eligibility to ensure people get covered sooner and hospitals receive payment for services they provide to the uninsured.

Section 1332 State Innovation Waiver Recommendations

- Keep the proposed structure of the reinsurance program, including directing more funding to areas with higher premiums.

- Do not allow premium subsidies to be used for non-qualified health plans. Doing so could create a shift in the market and increase costs for comprehensive qualified health plans.

- Remove the cap on the premium subsidies to ensure that everyone eligible for subsidies can continue to receive them and afford their health coverage.

- Maintain a centralized enrollment experience such as healthcare.gov and invest in outreach and enrollment assistance to help more people get enrolled, instead of relying on a decentralized system of private entities to be responsible for all outreach and enrollment.

Methodology

The Georgia Budget and Policy Institute worked with the Center on Budget and Policy Priorities to estimate the total cost of Georgia’s proposed 1115 and 1332 waivers using the following methodology. Draft waiver documents can be found on the Georgia Medicaid website here.

Calculating the cost of the proposed 1115 waiver:

The state’s 1115 waiver application document includes total cost estimates for each of the five years of the program on page 27. These estimates are included in the table below. The state makes their calculations by multiplying the per member, per month (PMPM) Medicaid cost by the total number of member months for that year. For example, the member months in year 2025 are based on an estimated enrollment of 52,509 multiplied by an average of per year in which each of those enrollees will receive Medicaid coverage—resulting in 525,094 member months in that year.

For each year, we calculated the state’s share of these costs by applying the state’s standard Medicaid match rate (67.30%). The state’s calculations assume Georgia will receive the standard matching rate instead of the 90 percent match available to states that fully expand Medicaid. GBPI’s projections of the state share of the waiver cost do not include new administrative costs, such as the potential costs of administering work reporting . For 2022, which is demonstration year 2 in the table below, we calculated the state cost for the proposed 1115 waiver to be $66,398,458. The estimated enrollment increases in 2022 under the 1115 waiver are on page 9 of the application.

Calculating the cost of the proposed 1332 waiver:

To understand the cost to the state of the 1332 waiver, we cite the estimates that the state provides on Table 8 of the 1332 waiver document (p. 24). According to this table, the state plans to use three funding sources to fund activities related to the 1332 waiver: assessing a user fee on insurers selling plans in the individual market (“State User Fees” in the table), spending state general funds (“Cost to State”), and receiving federal pass through dollars (“Net Pass Through Funding”).

The state is proposing to set a budget cap for its spending on the 1332 waiver. According to page 19 of the waiver application document, “The state’s total 1332 program cap is projected to be $255 million in state funds for Plan Year (PY) 2022 and will be adjusted on an annual basis in subsequent years. The funding cap will cover state funding for both the reinsurance program and state subsidies under Access Georgia.” The program funding will be funded by the state user fees and state general fund spending. Because the state proposes no longer using the federal exchange in 2022, they assume that instead of the federal government collecting a fee from insurers on the individual market, the state would now be collecting these fees. The state’s own estimates for user fee spending and state general fund spending are represented in Table 8, copied below. However, our total cost estimate only includes the state general fund spending—$149 million in 2022. The estimated enrollment increases in 2022 under the 1332 waiver are on page 20 of the application.

We did not incorporate the state user fee spending because it is neutralized by the newly collected revenue. Our total cost estimates also do not include the net federal pass through funding, because this money would come from the federal government. The 1332 waiver is projected to save the federal government money, mostly by reducing the amount the federal government spends on the premium tax credits available to people between 100% and 400% of the federal poverty line buying an individual market plan. Because the waiver must be budget neutral to the federal government, the state is asking to receive these savings back in the form of pass through funding. The expected federal savings are outlined in Table 2 on page 44 of the waiver document.

Calculating the cost of both the 1115 waiver and the 1332 waiver:

The two sections above explain how we obtained costs for each waiver. Our total state cost estimate in 2022 for the 1115 waiver is $66,398,458 and the cost estimate for the 1332 waiver is $149,000,000. By adding these two numbers together, the combined total cost for both waivers is estimated to be $215,398,458.

Calculating the cost of full Medicaid expansion:

In our table that includes the costs of full Medicaid expansion, we used estimates from the state’s most recent fiscal note for a bill expanding Medicaid eligibility up to 138 percent of the federal poverty line. The state auditor submitted the fiscal note for the legislation (HB 37) on January 18, 2019. The fiscal note can be accessed on the Governor’s Office of Planning and Budget website here. In Exhibit 1 on Page 2 of the fiscal note, the net cost of Medicaid expansion in fiscal year 2022 ranges from $188.4 million to $213.2 million. Exhibit 1 also includes estimated enrollment, which ranges from 496,503 to 598,329 in fiscal year 2022. For comparison to the proposed waivers, GBPI used the most conservative estimates from the fiscal note. For comparing the increase in enrollment under both options, we used the lowest estimated enrollment increase under Medicaid expansion. For comparing the state cost for both options, we used the highest net cost estimate for Medicaid expansion.

{kind=link}