Comparing Income Tax Bills Introduced During 2026 Session

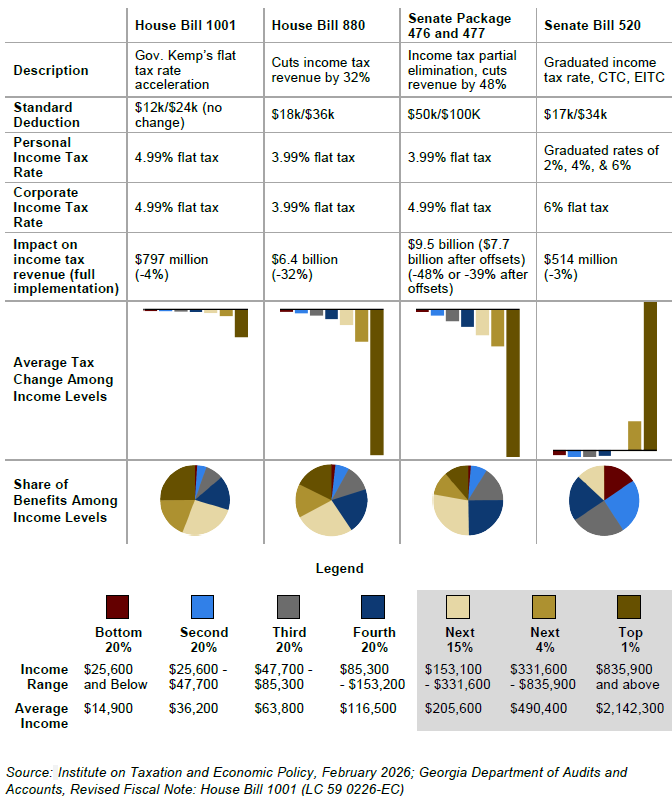

During the 2026 legislative session, members of the General Assembly have moved several bills forward that would dramatically change how Georgia raises and budgets public funds. Gov. Kemp has proposed accelerating the multi-year tax cut legislation enacted during his first term to reach a flat personal and corporate income tax rate of 4.99%. Other state leaders have proposed fully eliminating or significantly scaling back the income tax, Georgia’s largest source of revenue.

Income tax cut proposals like House Bill 880 and Senate Bill 477 dedicate billions in resources to cut Georgia’s income tax from the top down by reducing the state’s flat income tax rate. This is an extremely costly and highly inefficient way to deliver meaningful savings to most Georgians. Rate cuts disproportionately benefit those who earn the highest incomes because filers do not start seeing savings from cuts to the existing flat income tax rate until after they arrive at their state taxable income by applying any deductions, exclusions and other eligible tax credits.

Lawmakers seeking sweeping changes to the cornerstone of the state’s revenue system would be wise to consider the broader fiscal implications. Last year, Georgia raised more than half ($19.5 billion) of general fund revenues from income taxes.[i] That revenue was split between $16.2 billion in personal income taxes (47% of general funds) and $3.3 billion in corporate income tax collections (9% of general funds).

With the seventh lowest level of state taxes per person in the nation, Georgians paid an average of $3,009 in overall taxes in 2024.[ii] Georgians also continue to outperform our neighbors economically, earning a higher median income than residents of Florida, Tennessee and Texas.[iii]

Instead of doubling down on regressive income tax cuts for those making the highest incomes and corporations, policymakers should focus their attention on savings for working and middle-class families. State leaders must also recognize that large scale tax cuts without offsetting revenues directly threaten funding for health and education, which comprise three-quarters of state spending in FY 2027.

Get the full analysis here: https://gbpi.org/racing-to-the-bottom/

Endnotes:

[i] Georgia State Accounting Office. (2025, October 15). State of Georgia Revenue and reserves report, fiscal year ended June 30, 2025. https://sao.georgia.gov/swar/grr

[ii] U.S. Census Bureau. (2025, April). 2024 Annual survey of state government tax collections and 2024 state intercensal population estimate, as calculated by author. https://www.census.gov/programs-surveys/stc/data/datasets.html; https://www.census.gov/data/tables/time-series/demo/popest/2020s-state-total.html

[iii] U.S. Census Bureau. (2025, September). Household income in states and metropolitan areas: 2024. https://www.census.gov/library/publications/2025/demo/p60-286.html