Twelve days into the 2020 session of the Georgia General Assembly, legislators voted to take a week-long break from regular business to allow extra time for deliberations over Georgia’s fiscal priorities and annual appropriations bills. State leaders continue to express concerns over Gov. Kemp’s executive budget proposals, which include the first mandatory agency budget cuts and reduced mid-year revenue estimate since the Great Recession. Beyond agreeing on an appropriations plan for the next six months, Georgia’s leaders must also consider the precedent set by the $28.1 billion budget proposal for next year, which includes not only $300 million in across-the-board agency budget cuts, but also $400 million in pay raises for teachers and state employees.

At the same time, members of Georgia’s House of Representatives are set to begin debate over proposed income tax changes that could upend the state’s revenue system in order to give large tax cuts to the state’s top income earners. These same legislative changes would provide relatively small benefits to most Georgians at a significant cost to the state or, under a flat tax scenario, would likely raise taxes on hundreds of thousands of middle-class families.

Georgia relies heavily on income taxes to fund essential services and programs such as education, health care and public safety. Making large-scale changes to cap or reduce the revenue raising potential of the personal and corporate income tax would damage Georgia’s fiscal position in the years ahead. Fortunately, lawmakers seeking to make a targeted investment in low- and middle-income families have other options to reduce taxes without initiating the same level of large-scale revenue losses that would accompany cuts to the top income tax rate.

Three major proposals being considered by the Legislature could have significant implications for taxpayers and state revenues:

- House Bill 918 was enacted in 2018-2019 to restructure the state’s personal and corporate income tax provisions. It could still serve as the basis for a vote on an additional reduction to lower the state’s top income tax rate from 5.75 to 5.5 percent if a joint resolution is passed by both chambers of the General Assembly and signed into law by the governor. This change to both the personal and corporate income tax would cost the state approximately $615 million per year.

- House Bill 432 (LC 43 1488S) would abolish the state’s current system of tax rates that increase from 1 to 5.75 percent as incomes rise—known as a graduated tax system—in favor of a 5.5 percent flat tax structure.[1] After accounting for the bill’s other provisions, which include a non-refundable credit that essentially serves as a de-facto second bracket to help mitigate widespread tax increases that would otherwise be experienced by millions of Georgians, the legislation would still result in a net-tax increase for more than 646,000 Georgia households. These tax increases are largely distributed among middle class families and would help finance about $280 million in tax cuts that would largely benefit the state’s top earners.

- House Bill 588 proposes a non-refundable Georgia Work Credit modeled after the federal EITC to provide targeted tax cuts to more than two million low- to moderate-income people across the state at an annual cost of about $140 million.

Recent Major Developments in Georgia’s Appropriations and Tax Policies

The passage of the federal Tax Cuts and Jobs Act (2017) helped initiate some of the largest structural changes to Georgia’s income tax in decades. Although many provisions of the personal and corporate income tax are antiquated, balancing Georgia’s already-lean budget requires consistent growth in the state’s largest source of revenue. For the 2021 Fiscal Year, out of $26.6 billion in General Funds raised, the state projects about 48 percent of state revenues will be generated by the personal income tax and 6 percent from the corporate income tax.

- Fiscal Year 2011: By fiscal year 2011, in the wake of the Great Recession, state revenues have declined by more than 18 percent from the previous positive baseline. By the time the state’s period of recovery begins, Georgia’s Revenue Shortfall Reserve is depleted from $1.5 billion to $116 million and K-12 Education is underfunded annually by $1.355 billion below the level demanded by the Quality Basic Education (QBE) formula.[2]

- Fiscal Years 2011-2018: In fiscal years 2011-2018, Georgia’s tax and fee collections increase by an average of 6.1 percent, helping the state grow spending by more than 40 percent between AFY 2011 and FY 2018 while accruing significant savings to the state Revenue Shortfall Reserve.[3]

- December 2017: The Federal Tax Cuts and Jobs Act (TCJA) is signed into law by President Donald J. Trump after receiving Congressional approval. The TCJA fundamentally changes how millions of Georgians and state-based businesses will calculate their income taxes from 2020 to 2025, reducing federal revenue collections from Georgians by more than $43 billion and reshaping the structure of the state’s main source of revenue. The law’s provisions carry an outsized effect in Georgia, as significant changes restructure most personal income tax brackets with lower rates, add new limits for itemized deductions, eliminate the personal exemption and double the value of the standard deduction, permanently reduce the federal corporate tax rate and eliminate the tax penalty used to enforce the Affordable Care Act’s health coverage mandate.[4]

- February 2018: The Georgia General Assembly reaches an agreement with Gov. Deal to advance HB 918 as the state’s response to the federal TCJA, rather than adopting standard conformity legislation that would have increased baseline revenues. Effective February 2018, the first phase of the law updates Georgia’s state income tax code to include several key changes originally included in the federal legislation to roll-back some of the most costly personal income tax deductions, which increases the state revenue baseline by $1.1 billion. It also doubles the state standard deduction to $4,600 for individuals and $6,000 for married couples through 2025, lowering the state revenue baseline by $515 million. Notably, these changes maintain the marriage penalty built into the state’s standard deduction and preserve Georgia’s personal exemption. The number of filers itemizing is reduced from an estimated 31 percent of taxpayers to 14 percent, with 86 percent of Georgians utilizing the standard deduction once the TCJA-initiated changes go into effect.[5]

- March 2018: Nathan Deal increases the state’s revenue estimate by $167 million, allowing the General Assembly to approve a $26.2 billion budget that fully funds Georgia’s public schools under the QBE formula for the first time in 16 years.

- November 2018: In response to Hurricane Michael, Gov. Deal raises the state’s revenue estimate by $271 million to $26.5 billion, allowing legislators to approve a major disaster recovery package in Georgia’s first Special Session since 2011.

- January 2019: Phase two of HB 918 automatically goes into effect, completing the implementation of the legislation’s authorized provisions by reducing the state’s top income tax rate from 6 percent to 5.75 percent through 2025. This change reduced the state’s revenue baseline by approximately $456 million per year.[6]

- May 2019: Kemp signs the state’s FY 2020 budget into law, approving $530 million to increase the state base salary schedule to provide a $3,000 pay raise for certified teachers and certified employees effective July 1, 2019 and approves a 2 percent merit pay increase for state employees at a cost of $116 million.

- June 2019: FY 2019 concludes with Georgia’s personal income tax falling short of FY 2019 estimates by more than $130 million. The state Department of Revenue reported $12.176 billion in annual collections, significantly lower than the $12.3 billion projected under Gov. Kemp’s FY 2019 revenue estimate.

- September 2019: State agencies submit plans at Gov. Kemp’s request for 4 percent cuts for FY 2020 and reductions of 6 percent in FY 2021. These spending cuts are applied to discretionary spending, which represents about $5.5 billion, or less than 20 percent of the state’s total $26.6 General Fund budget for FY 2021.[7] Programs that are enrollment-driven, such as Medicaid, are exempt.

- January 2020: Kemp reduces the current year revenue estimate by $417 million. Gov. Kemp also submits a 2021 budget request that includes $600 million to cover the costs of increased enrollment and mandatory spending growth for public schools, health care programs, higher education transportation and debt service payments on previously issued bonds.

- FY 2020-FY 2021: Kemp’s budget proposals call for more than $500 million in combined mandatory spending cuts over the next 18 months and a reduction of $417 million to the state’s revenue estimate for the current year that ends June 30, 2020. The proposals include $887 million in increased teacher pay and approximately $160 million in pay increases for state employees, adding more than $1.05 billion to the state’s annual appropriations baseline in increased salaries for educators and state employees. On the other side of the ledger, the cost of existing state tax expenditures also continues to climb, with the Film Tax Credit adding up to an estimated $474 million in lost revenue in 2020 and the state’s tax break on retirement income reaching nearly $1 billion.

Previous Tax Cuts, Spending Increases Complicate Viability of Further Tax Changes

From 2007 to 2018, the governor annually instructed state agencies to either cut spending or keep expenditures flat. In the middle of the 2020 fiscal year, Gov. Kemp’s office asked state agencies to prepare the first mandatory budget reductions since the Great Recession. Nearly every state agency has been called upon to implement budget cuts of 4 percent effective part-way into the 2020 fiscal year, with an additional 6 percent reduction called for in FY 2021. These across-the-board spending cuts take into account slowing economic activity, the costs of the governor’s priorities and the effects of recently approved tax changes that will lower revenue collections by an estimated $1 billion from the previous year’s baseline.[8]

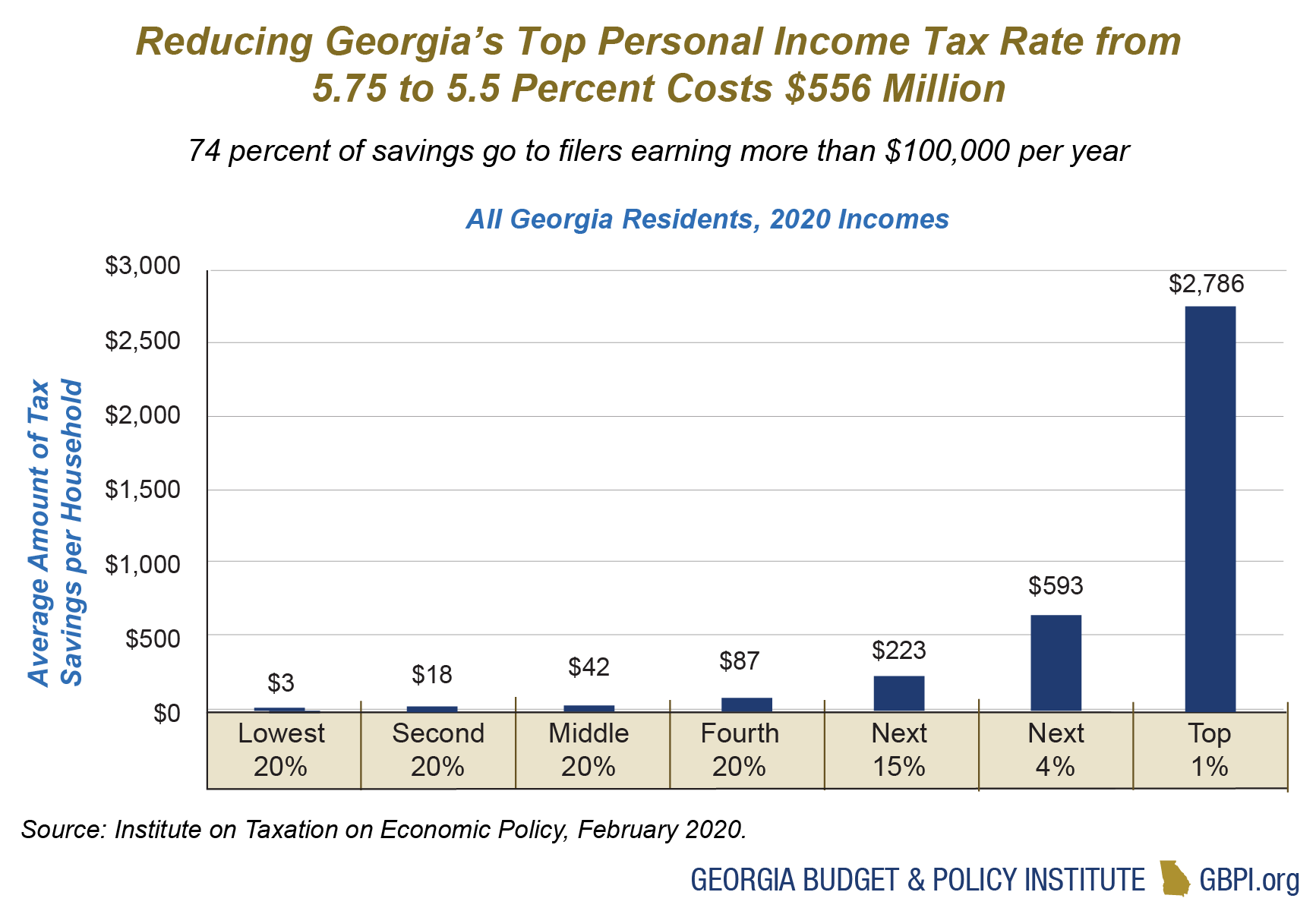

Due to these factors, the state is not in a fiscal position to absorb the $556 million in annual revenue losses that would accompany an additional quarter percentage reduction in the top income tax rate.[9] To meet the state’s constitutional obligation of a balanced budget, such a measure would likely require offsetting tax increases or drastic spending cuts. Similar tradeoffs will remain under any potential budget proposal that seeks to increase state spending or cut taxes in FY 2020 or FY 2021. It is especially clear that continuing to fully fund the QBE public education formula while providing for a $5,000 increase in state educator pay over two years would require Georgia to both preserve and expand revenue collections to fund current and future state priorities.

Going forward, the state projects that Georgia’s economy must grow by approximately 2.5 percent annually to preserve spending at the reduced baseline recommended in Gov. Kemp’s FY 2021 proposed budget. The baseline level of state expenditures is expected to rise by about 9 percent from $26 billion in the amended 2020 fiscal year to $29 billion by FY 2024. Consequently, Georgia’s revenues must continue to steadily increase in the years ahead to simply maintain the level of spending proposed in the governor’s relatively lean budget proposal.[10]

The following analysis considers the effects that three distinct tax proposals would have on Georgia’s fiscal health from the 2020 fiscal year forward. The estimates for pending proposals rely on data produced by Georgia State University’s Fiscal Research Center, estimates prepared by the Institute on Taxation and Economic Policy and GBPI’s analysis of other available information and data sources. A full methodology is published at the end of this report.

HB 918: Second Quarter-Point Cut Offers Few Benefits to Vast Majority of Georgians

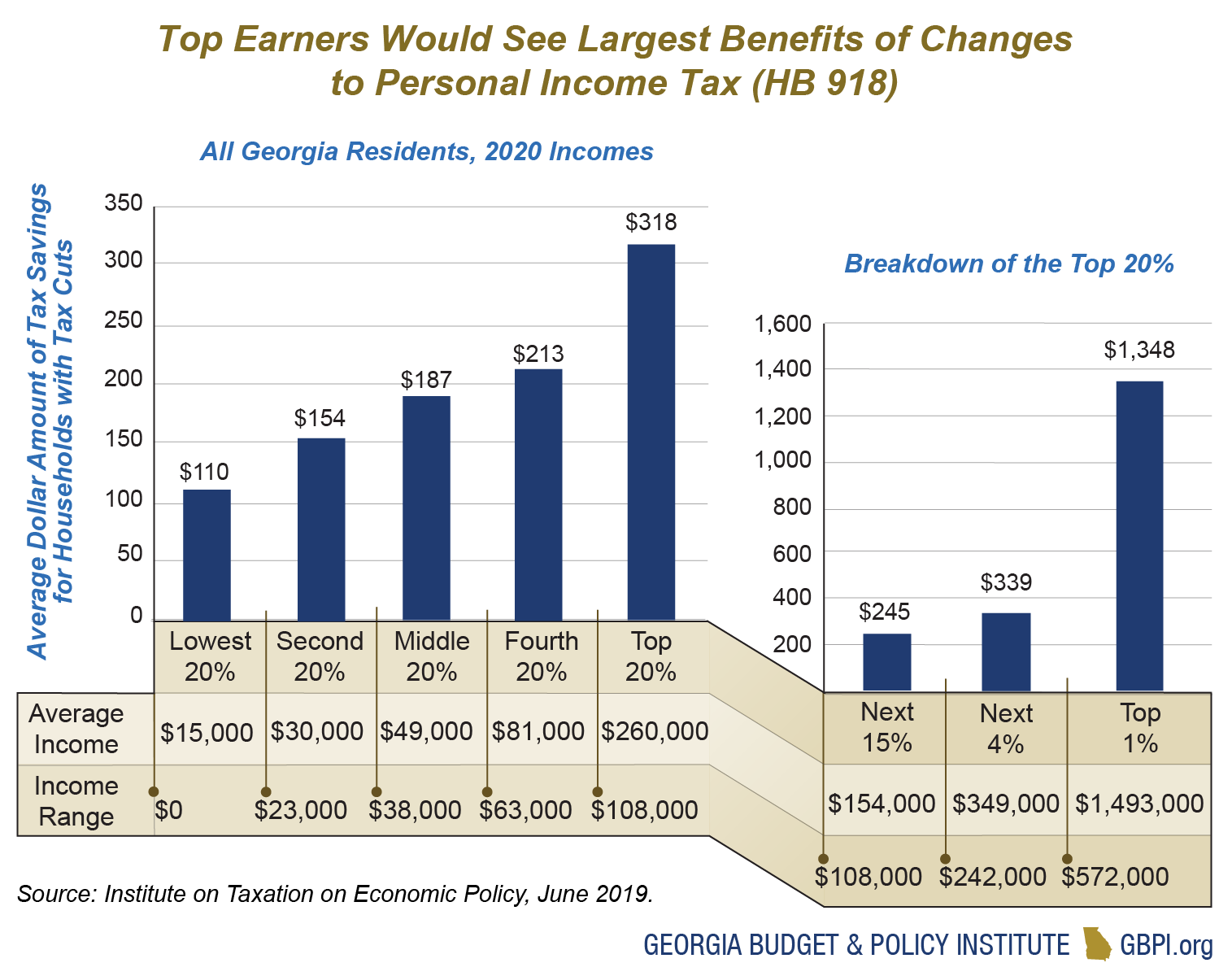

While the federal Tax Cuts and Jobs Act (TCJA) reduced federal personal income taxes for 88 percent of Georgia residents, Georgia’s upper-income households saw the greatest reduction. In 2020, about 75 percent of Georgia’s total $7.8 billion in annual federal tax savings will go to households earning more than $108,000 annually. The Georgians who gain the smallest share of these tax savings are the 1.9 million families and individuals with incomes less than $38,000 per year. These 40 percent of households collectively receive less than 6 percent of the total tax savings distributed across the state.[11]

In his 2020 presentation to Georgia’s legislative appropriations leaders, state fiscal economist Jeffrey Dorfman shared his assessment that most taxpayers did not feel the initial tax cut, the first change to the income tax since 1937. Speaking about the reduction that went into effect last year, Dorfman said:

“[I]t happened January 1st [2019] … [so] most Georgians probably had their take home paycheck actually go down, not up, because the Georgia state income tax cut was smaller than the increase in [the cost of] their health insurance premium. And so, nobody even knew they got a tax cut. And if they don’t know they got a tax cut, then there isn’t going to be any incentive, or any growth, because of that tax cut.”[12]

Overall, after reducing the top income tax rate to 5.75 percent, doubling the state’s standard deduction and offsetting changes made to cap or eliminate certain itemized deductions, Georgia’s tax changes reduced the amount of taxes owed by 55 percent of residents, with modest benefits distributed relatively equally across most income levels. On the other hand, about 24 percent of taxpayers experienced no change in tax liability, while 21 percent paid more than they otherwise would have prior to the passage of the TCJA.[13] Rather than significantly reducing taxes, the state’s already-implemented legislative tax changes primarily acted to prevent a majority of Georgians from experiencing a visible tax increase as a result of the federal changes.

Importantly, tax savings are not distributed equally when Georgia acts to lower its top personal income tax rate. Cutting the top income tax rate from 5.75 to 5.5 percent would cost the state an estimated $556 million per year. Simultaneously reducing the flat 5.75 percent corporate income tax rate to a matching 5.5 percent carries an added cost of $60 million per year, the vast majority of which would benefit large out-of-state corporations and shareholders.[14]

Importantly, tax savings are not distributed equally when Georgia acts to lower its top personal income tax rate. Cutting the top income tax rate from 5.75 to 5.5 percent would cost the state an estimated $556 million per year. Simultaneously reducing the flat 5.75 percent corporate income tax rate to a matching 5.5 percent carries an added cost of $60 million per year, the vast majority of which would benefit large out-of-state corporations and shareholders.[14]

More than 76 percent of the total share of $615 million in personal and corporate income tax savings would go to corporations and filers whose incomes fall within the top 20 percent of Georgians—more than $108,000 per year—while the remaining 80 percent of Georgians with lower incomes would only receive 24 percent of the total tax savings caused by lowering the income tax rate. Ultimately, the remaining $147 million in annual savings would be divided among Georgia’s nearly 3.9 million filers who earn less than $108,000 per year.[15]

Unlike the federal government, the state of Georgia is required by its constitution to balance its budget each year. If an additional income tax rate cut of 0.25 percent is adopted by the Legislature, the reduction in revenues would be equivalent to about twice the level of cuts already recommended in Gov. Kemp’s FY 2021 budget.

Unlike the federal government, the state of Georgia is required by its constitution to balance its budget each year. If an additional income tax rate cut of 0.25 percent is adopted by the Legislature, the reduction in revenues would be equivalent to about twice the level of cuts already recommended in Gov. Kemp’s FY 2021 budget.

Even if Gov. Kemp’s recommendation for $400 million in added pay raises for teachers and state employees is eliminated and replaced with the second phase of the rate cut in HB 918, trading this appropriation for a top income tax rate of 5.5 percent would carry with it more than $215 million in additional costs beyond the savings generated from forgoing the proposed pay raise. Notwithstanding the implications for revenue growth beyond next year, reducing the state’s top income tax rate to 5.5 percent would require state leaders to identify hundreds of millions in additional spending cuts, further affecting core government agencies through reductions in staffing, programs and services.

One year after the state of Georgia implemented its first-ever cut to the top income tax rate, personal income tax revenues are set to increase at the slowest rate in a decade, with Gov. Kemp’s revised revenue estimate for FY 2020 projecting a tepid 1 percent growth rate. Simultaneously, the state’s budget estimates include an increase of nearly 11 percent in corporate tax revenues in FY 2020 and a 9 percent increase in FY 2021.

If this trend holds, from FY 2017 to FY 2021, corporate income tax revenues will increase by 58 percent. This significant spike stands in comparison to a 13 percent increase in overall General Fund revenues (excluding the corporate income tax). With the corporate income tax emerging as a bright spot amid Georgia’s flat current-year revenue collections, reducing corporate taxes by more than 4 percent is risky, would lower revenues by about $60 million per year and would not demonstrably benefit the state.

HB 432: Flat tax legislation raises taxes on middle class families to finance cuts for top income earners

Some legislators have proposed a flat tax, rather than the current system where tax rates increase as income levels go up, as an alternative to another reduction to the top income tax rate, noting that such proposals would carry a lower overall cost to the state or even generate revenue by increasing taxes for many low- and middle-income Georgians.

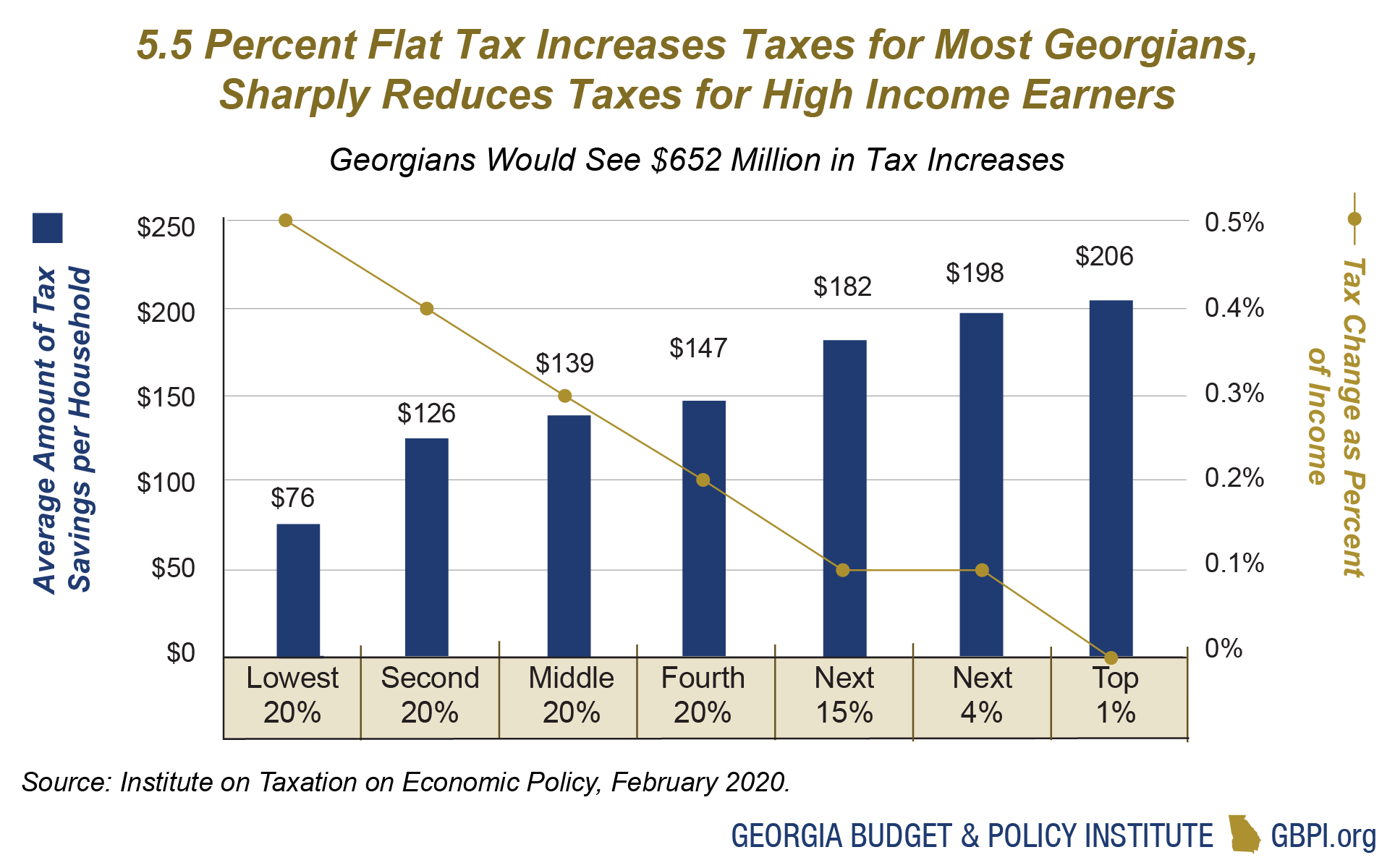

Raising taxes for an estimated 647,000 low- and middle-income households across Georgia, the most recent flat tax proposal—HB 432—would direct 84 percent of $283 million in net tax cuts to corporations and the top 5 percent of households, which earn more than $240,000 per year.[16] In fact, 55 percent of the total benefits arising from the legislation would go to the top 1 percent of households—those that earn a minimum of $572,000 per year—in the form of average annual tax cuts of about $2,700.[17]

HB 432’s provisions, which are outlined in a recent fiscal note, include: replacing the state’s current graduated personal income tax structure that currently taxes income at rates between 1 to 5.75 percent with a flat 5.5 percent rate, reducing the state’s already-flat corporate income tax rate from 5.75 to 5.5 percent, creating a non-refundable tax credit based on a maximum threshold of taxable income for both single and married households and eliminating the existing low income credit along with the state’s itemized deduction for Georgia income taxes paid.

Eliminating Georgia’s Graduated Personal Income Tax Brackets Means Increasing Taxes from the Bottom Up

The first step initiated under HB 432 is the elimination of Georgia’s graduated income tax structure, which currently taxes income at rates between 1 to 5.75 percent, in favor of adopting a single flat tax rate of 5.5 percent that would be applied to all taxable income.

In the research on HB 918 outlined above, the effects of lowering the state income tax by a quarter percentage-point are described. Under a flat tax rate of 5.5 percent, the individual effects of lowering the top rate from 5.75 to 5.5 percent remain the exact same, with $556 million in reduced personal income tax collections over a full year and about 74 percent of savings going to filers in the top 20 percent of earners.

However, eliminating the state’s existing graduated tax brackets of 1-5 percent to complete the state’s transition to a single flat personal income tax rate would result in a significantly larger $652 million statewide tax increase that affects more than 3.8 million Georgians. After factoring in the effects of the $556 million personal income tax cuts from reducing the top rate to 5.5 percent, an estimated 60 percent of Georgia taxpayers, or 2.9 million filers, would still experience a net tax increase under a 5.5 flat tax.

More Revenue Raisers Combine to Fund Newly Manufactured Tax Credit, but Focus Tax Cuts on High-Income Earners

More Revenue Raisers Combine to Fund Newly Manufactured Tax Credit, but Focus Tax Cuts on High-Income Earners

HB 432 also includes two additional revenue-raising provisions to help finance a non-refundable tax credit intended to mitigate the tax increases produced by a 5.5 percent flat tax. The legislation raises taxes on households that currently take advantage of Georgia’s itemized deduction for state income taxes paid, increasing revenues by $130 million by raising taxes on about 543,000 households. Georgia remains an outlier in allowing filers to write-off state tax payments through a loophole that was adopted to mirror the federal State and Local Tax (SALT) deduction. Although state leaders should, in fact, eliminate this provision from the tax code, using the resulting revenues to almost exclusively cut taxes for top earners in the state rather than fund state priorities does not represent a positive step forward. Finally, HB 432 would also eliminate the state’s existing but small low-income tax credit, increasing state revenues by about $5 million.[18]

Although HB 432 is marketed as a 5.5 percent flat tax rate, the legislation’s convoluted design uses these provisions to fund a second, lower tiered bracket of 5.25 percent by offering a non-refundable credit to single taxpayers earning under $69,000 per year and to married taxpayers earning below $94,000 annually. Notably, in addition to raising taxes on most of the middle-class families that would experience an observable tax change under the proposal, HB 432 would exacerbate the existing marriage penalty, which is created by the state’s extremely low standard deduction and causes married couples to pay a larger percentage of their income in taxes, on average, than single filers.

The only group of Georgians that will see an average annual tax cut greater than $5 if HB 432 becomes law are those earning more than $242,000 per year, enough to rank in the top 5 percent of the state’s filers. Most of the net tax savings—55 percent—will be shared by filers making more than $572,000 per year; the top 1 percent of income earners will, on average, benefit from a net tax cut of $2,650 per year. Georgians in the middle class—those earning between $38,000 to $108,000 per year—will pay an average of $20 more per year in taxes. Because this legislation would not actually reduce taxes for the vast majority of people, it would be more accurately described as a transfer of tax liability from Georgia’s highest income earning filers and corporations financed by middle class families.

The only group of Georgians that will see an average annual tax cut greater than $5 if HB 432 becomes law are those earning more than $242,000 per year, enough to rank in the top 5 percent of the state’s filers. Most of the net tax savings—55 percent—will be shared by filers making more than $572,000 per year; the top 1 percent of income earners will, on average, benefit from a net tax cut of $2,650 per year. Georgians in the middle class—those earning between $38,000 to $108,000 per year—will pay an average of $20 more per year in taxes. Because this legislation would not actually reduce taxes for the vast majority of people, it would be more accurately described as a transfer of tax liability from Georgia’s highest income earning filers and corporations financed by middle class families.

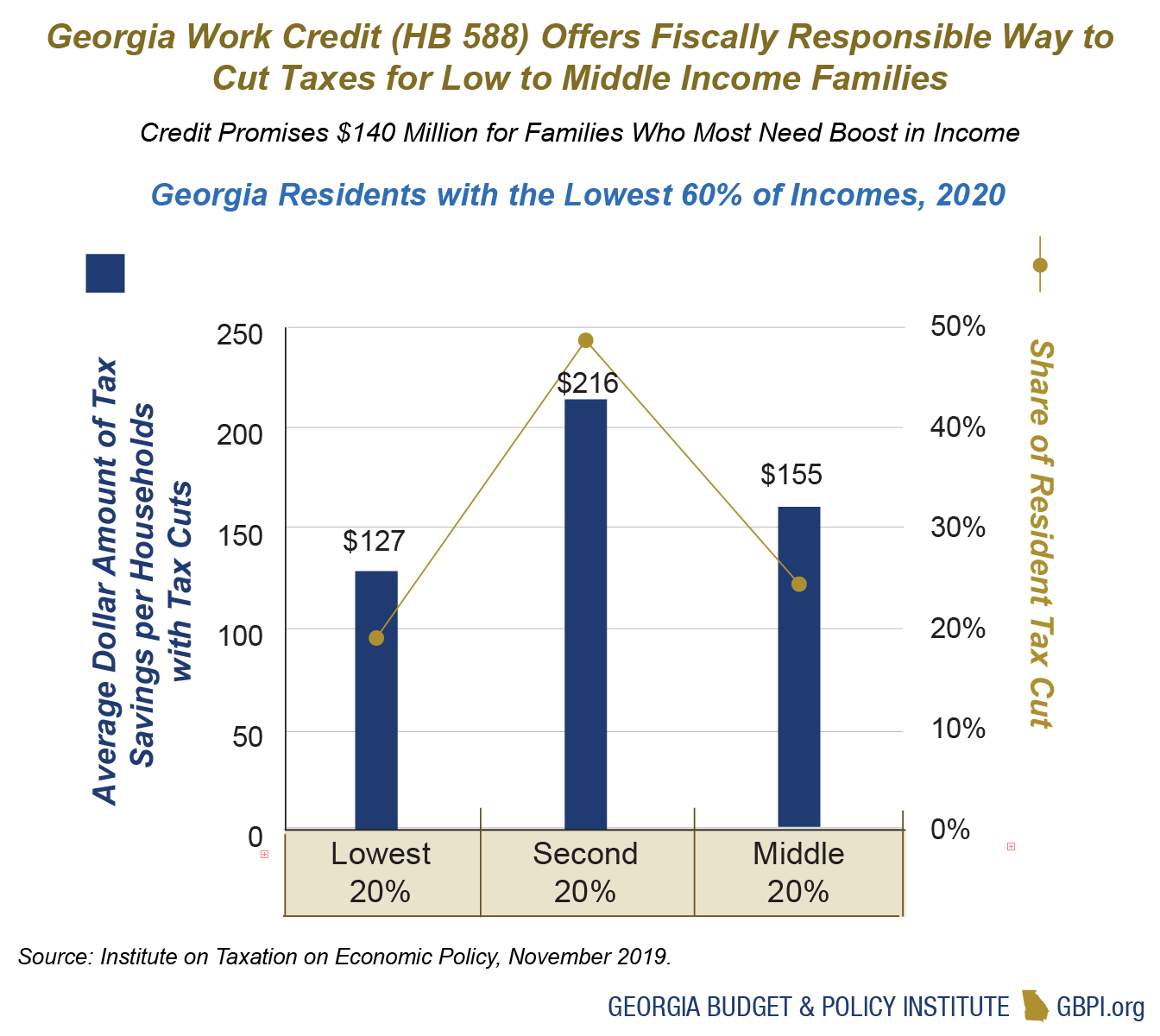

HB 588: Look to the Georgia Work Credit for a Relatively Low Cost, Sustainable Way to Cut Taxes for Families

Also known as the Georgia Work Credit, HB 588 is a bipartisan bill that has been introduced in the House of Representatives. The Georgia Work Credit would offer a modest, non-refundable tax cut of up to $500 for low- and moderate-income families earning up to $56,000 per year. By effectively targeting the tax cuts to follow guidelines established by the federal Earned Income Tax Credit, HB 588 provides a pathway to cutting taxes for two million Georgians, including the families of one million children, at a relatively low cost of $140 million per year in revenue lost to the state.

To provide genuine assistance to Georgia families who have not substantially benefited from recent federal and state tax reform efforts, lawmakers would be wise to enact the Georgia Work Credit. Moreover, the legislation’s relatively low cost and sustainable growth trajectory would allow members of the General Assembly to take a concrete step toward putting more money in the pockets of hard-working Georgians without taking on the same risks for potentially unintended effects that could follow more sweeping legislative changes.

To provide genuine assistance to Georgia families who have not substantially benefited from recent federal and state tax reform efforts, lawmakers would be wise to enact the Georgia Work Credit. Moreover, the legislation’s relatively low cost and sustainable growth trajectory would allow members of the General Assembly to take a concrete step toward putting more money in the pockets of hard-working Georgians without taking on the same risks for potentially unintended effects that could follow more sweeping legislative changes.

Conclusion: State Leaders Should Refocus on Making Tax Code More Fair Instead of Cutting Top Rate

No identifiable group in the state of Georgia has obtained a disproportionately larger share of the tax savings initiated by recent federal and state legislative changes than corporations and the highest-income earners. These are the same groups that would again primarily benefit from proposals like the flat tax under HB 432, the second rate cut contemplated by HB 918 or any other similarly narrow effort that focuses on lowering the state’s current 5.75 percent top income tax rate for households and corporations.

The only major distinction between the effects of these competing proposals is that HB 918’s provision for a second cut to lower the top income tax rate to 5.5 percent does not in any way seek to offset the cost of providing $615 million in new tax cuts that would primarily benefit corporations and high-income earners, while HB 432 seeks to help pay for the resulting revenue losses by raising taxes on middle class families. Neither of these bills offer effective ways to help remedy disproportionate costs absorbed by low- and middle-income Georgians who have experienced the smallest share of benefits—or whose taxes have increased—as a result of the combined effects of the federal TCJA and state response.[19]

Reductions to the top income tax also carry risks of limiting the revenue generating potential of the personal and corporate income tax as data shows top earners have experienced by far the largest rate of growth in income over recent years. From 2007-2019, wages for the top 5 percent of earners in Georgia grew by 17 percent. For middle-income earners at the 50th percentile, wages actually fell by 1 percent over the same time frame.[20]

Under Gov. Kemp’s proposed budget for the next fiscal year, the state of Georgia will spend slightly less per resident to operate state government than it did in the early 2000s.[21] Up to the current FY 2020 budget, when many state agencies began to experience 4 percent across-the-board budget cuts part-way into the fiscal year, Georgia’s annual appropriations bills had largely focused on restoring previously issued, much deeper cuts that were made a decade ago. With less than 20 percent of the state’s budget funding non-mandatory, but critically important functions of government across 45 state agencies, there is little room for error in the appropriations process.

Across the core areas of education, health care, public safety and programs targeted toward rural and low-income communities, members of the General Assembly will find recent priorities of the General Assembly included in the budget cuts recommended by the governor’s proposed budget for the next fiscal year. Beyond the threat of backsliding and reversing recent state advancements is the fact that state leaders can readily expect significant increases in spending in the years ahead based on recent legislative commitments, such as the state’s pending 1115 and 1332 waiver proposals, which, if approved, are certain to carry hundreds of millions in new costs each year, along with other frequently discussed but currently unenacted priorities such as deploying rural broadband. Raising enough revenue to meet Georgia’s basic obligations and proactively invest in other priority areas requires continued efforts to grow the state’s overall revenue collections.

There are opportunities for tax reform in Georgia that would allow the state to increase revenue collections, while simultaneously reducing the amount of taxes owed by many low- to middle- income taxpayers. For example, the vast majority of Georgians currently pay income taxes using the standard deduction, however, the state offers a credit that is far lower than its federal counterpart and not indexed to keep up with inflation, despite also offering an array of relatively generous itemized deductions, tax credits, and loopholes that most Georgians can’t access to reduce their tax liability. In addition to establishing a review process for future tax breaks, lawmakers should begin a thorough review of Georgia’s tax code to identify provisions that offer a poor return on investment to Georgians and consider ways to repurpose those revenues to ensure Georgians paid the lowest incomes do not end up paying a higher share of their incomes in state and local taxes than those who earn the most.

Over the nearer term, the state’s first priority should be to enact measures that will strengthen revenue collections and help the state avoid budget cuts that affect important functions of state government. After nearly 10 years spent building back from the Great Recession, regaining the state’s fiscal footing will allow for investments in the future and ensure Georgia remains prepared for any challenges that may arise as the state enters a new decade with optimism for continued growth.

Methodology

GBPI’s research on HB 918, HB 432 and HB 588 relies on data produced by Georgia State University’s Fiscal Research Center, estimates prepared by the Institute on Taxation and Economic Policy (ITEP), and GBPI’s analysis of other available information and data sources.

Unless otherwise noted, the specific effects to taxpayers—in the form of net-tax effects or offsetting tax cuts and tax increases—are sourced from ITEP estimates generated in February 2020. ITEP’s analysis simulates the effects of these legislative tax changes on more than 5 million Georgia tax filers to produce estimates for the average tax change across quintiles of income.

For components of income that are subject to income taxes, ITEP relies on information from the Internal Revenue Service’s “Statistics of Income” publication, which provides detailed state-specific information on components of income at different income levels. For components of income that are either fully or partially tax-exempt, ITEP uses data from the Congressional Budget Office and the Current Population Survey to estimate income levels in each state.

A Note on HB 432

GBPI’s research reveals that when fully implemented, HB 432 would cost the state a total of $191 million in lost revenue over the current Fiscal Year 2021 baseline, significantly more than the $40 million projected under the fiscal note attached to the legislation, which was prepared for the Department of Audits and Accounts by Georgia State University’s Fiscal Research Center (FRC).

Both GBPI’s research and the fiscal note project about $60 million in lost revenue from a 0.25 percent reduction in the state’s corporate income tax. However, GBPI’s research reveals that HB 432’s offsetting changes to the personal income tax would amount to $131 million in lost revenue, while the FRC projects a net increase of $17 million in tax revenue. This difference means that GBPI’s research on HB 432 likely projects that a lower level of offsetting tax increases will take effect for low- and middle-income families than what is projected in the state fiscal note attached to the current version of the legislation, although the FRC’s analysis does not include estimated effects for taxpayers by income group. GBPI’s findings are also informed by earlier estimates prepared by the FRC to assess the fiscal effect of flat tax proposals and the effects of reducing Georgia’s top personal income tax to 5.5 percent, as analyzed in the fiscal note for HB 918 (LC 34 5383-ECS).

Endnotes

[1] Research on House Bill 432 considers the February 3, 2020 Fiscal Note issued by the Georgia Department of Audits and Accounts, publishing an analysis conducted by Georgia State University’s Fiscal Research Center (FRC) on LC 43 1488S, House Bill 432. This analysis also utilizes data prepared by the Institution on Taxation and Economic Policy (ITEP) conducted on the same version of the legislation in February 2020; where appropriate, the FRC and ITEP are both cited as sources for the data included in this report.

[2] Presentation by Office of Planning and Budget Director Teresa MacCartney, “A Look Ahead: FY 2018 Year End to FY 2020 Budget Development,” Georgia Fiscal Management Council, April 26, 2018.

[3] Georgia Department of Revenue, Comparative Summary of State General Fund Receipts. GBPI analysis of reports from 2011-2020.

[4] Institute on Taxation and Economic Policy, June 2019.

[5] “Fiscal Note House Bill 918 (LC 34 5383-ECS,),” Department of Audits and Accounts. February 2018.