This analysis was co-authored by Daniel Kanso, PhD; Leah Chan, MPH; and Ashley Young

![]()

In signing the Fiscal Year (FY) 2027 budget approved by the General Assembly through House Bill 974, Gov. Kemp issued a combined 157 budget disregards and line-item vetoes to cut more than $344 million in spending. Budget disregards act similarly to line-item vetoes and allow the governor to withhold funding for certain line items in the budget approved by the General Assembly. Most of these sweeping cuts removed funding for public education ($87.5 million), healthcare ($81.8 million) and human services ($15.8 million).

Gov. Kemp made clear that these spending cuts are intended to partially offset the cost of more than $1.2 billion in income tax cuts approved this year through HB 463.[1] In its first full year of implementation, this legislation delivers more tax cuts to those in the top one percent and out-of-state corporate interests than to the first 60% of Georgia households combined.[2] As a result, Georgia’s tax system will be further skewed toward those already earning the highest incomes and away from meeting the needs of working and middle-income families.

On average, Georgia households will see $196 in savings next year from HB 463, while countless Georgians are harmed by budget cuts to essential services ranging from student transportation to domestic violence and sexual assault centers. For middle-income households, the average tax change from the $1.2 billion package amounts to less than $10 per month or $119 per year. If the remainder of this legislation is implemented over the next eight years, it would cost an additional $5.1 billion annually.

FY 2027 Budget Disregards and Line-Item Vetoes by Category:

- Employees’ Retirement System: $100 million (29%)

- Health: $81.8 million (24%)

- PreK-12 Education: $61.5 million (18%)

- Higher Education: $26 million (8%)

- Public Safety/Corrections: $31.4 million (9%)

- Human Services: $15.8 million (5%)

- Transportation: $11 million (3%)

- Other Areas of State Government: $16.7 million (5%)

- Total: $344.2 million

Health:

Georgia is in a healthcare affordability crisis. This year, over half a million working Georgians with household incomes above the poverty level have dropped their Georgia Access marketplace health insurance coverage due in large part to rising premiums.[3] At the same time, Georgia’s costly experiment with a Medicaid work requirement for able-bodied adults 19-64 years old with household incomes below the poverty level, known as Pathways to Coverage, has enrolled less than 15% of eligible uninsured adults from working households as of April 2026.[4] Now, Gov. Kemp’s budget cuts leave the state with a weakened healthcare safety net and inadequate access to the home- and community-based services that reduce reliance on more costly institutionalized care. Overall, health agencies lost approximately $81.8 million in funding from the FY 2027 budget approved by the General Assembly.

Significant changes include:

- Disregards $48 million in new Medicaid reimbursement rate increases that support a range of providers and facilities from primary care and dental care to psychiatric residential treatment. The largest single reimbursement rate increase would have been for autism services. These cuts come as providers that serve children with autism and other special needs are already feeling financial pressure due to 20% reimbursement rate cuts for certain services announced by two of Georgia’s Medicaid care management organizations, CareSource and PeachState.[5]

- Disregards $9 million in new funds that would allow more Georgians with intellectual and developmental disabilities to receive services in their homes and communities. This reduces the number of new NOW/COMP waiver slots from 500 to 100, which represents a mere one percent of the approximately 7,800 Georgians on the planning list of Georgians who have applied and been determined pre-eligible.[6]

- Disregards $4 million for a rural hospital solvency evaluation plan. Changes to Georgia’s state directed payment program will result in the loss of an estimated $626 million in supplemental federal provider payments for rural Georgia providers over the next decade and, without intervention, more rural hospitals could be forced to reduce services (like St. Mary’s in Lavonia) or close altogether.[7]

Education:

Gov. Kemp’s executive budget disregards and line-item vetoes reduced funding for education by $87.5 million from the FY 2027 budget passed by the General Assembly, cutting $61.5 million for PreK-12 education and $26 million for higher education. Already, local public school districts were facing significant funding constraints in the years ahead due to the passage of SB 33, which caps annual homesteaded property tax assessment increases at three percent. Although SB 33 will limit funding for all levels of local government, this measure is likely to have the greatest effect on school districts, which raise about 71% of total local tax revenues from property taxes.[8] Now, schools will also have fewer resources to contend with rising student transportation costs, higher health insurance premiums and lower levels of state funding for essentials like school safety.

Significant changes include:

- Disregards $30.7 million for additional school transportation and support for bus operations.

- Vetoes $12 million in bonds for financing $50 million in school safety equipment grants.

- Disregards $5 million for equipment needs at Central Georgia Technical College that would support Georgia’s healthcare workforce.

- Disregards $2.7 million for one one-time grants that would allow school systems to purchase vision and auditory screening equipment, which was part of the General Assembly’s literacy package.

- Disregards $5 million in additional out-of-school care for statewide and community grantees.

- Disregards $2 million for the Georgia Student Finance Commission to support the Service Cancelable Loan Program for behavioral health professions.

Human Services and Supports for Georgians:

When the General Assembly convened for the 2026 legislative session, Georgia was in the midst of a child welfare crisis, staring down an agency budget shortfall of approximately $86 million.[9] Gov. Kemp’s executive budget disregards will withhold $15.8 million from the budget approved by the General Assembly for the Department of Human Services, while also cutting millions more from supporting state agencies for services that range from feeding students from households with low incomes to meeting urgent needs through domestic violence shelters and sexual assault centers. Funding removed for foster children, community youth wellness and child abuse and neglect prevention could reignite the child welfare crisis that lawmakers had just begun to address.

Significant changes include:

- Disregards $9.4 million in funding for domestic violence shelters and $3.3 million for sexual assault centers.

- Disregards $2.5 million that was intended to help support veterans struggling to maintain housing.

- Disregards $2 million to halt the state’s participation in the SUN Bucks summer nutrition program that would provide meals and snacks to students.

- Disregards $2 million to support caregiver support services for Georgia seniors.

- Disregards $1.5 million for child welfare services to support family reunification, youth exiting foster care and at-risk families.

- Disregards $1.2 million for child abuse and neglect prevention programs.

Income Tax Cuts from HB 463 Lead to Budget Cuts

Without accounting for the implications to Georgia’s state budget, lawmakers approved a sweeping income tax plan (HB 463) designed to reduce the state’s flat income tax rate over nine years, while simultaneously increasing a range of income tax deductions, exemptions and exclusions.[10] GBPI estimates that the legislation will reduce state revenues by $1.2 billion over its first full year and $6.3 billion if fully implemented. However, these tax cuts are heavily skewed to benefit those earning the highest incomes and corporations.

Although the legislation eliminates 13 income and sales tax credits, the revenues raised total just $10.4 million in FY 2027 and do not even scratch the surface of covering the cost of the tax cuts approved.[11] As a result, Gov. Kemp determined that HB 463 pushes Georgia’s budget out of balance and issued more than $344 million in executive budget disregards and line-item vetoes to partially cover the cost of lost income tax revenues.

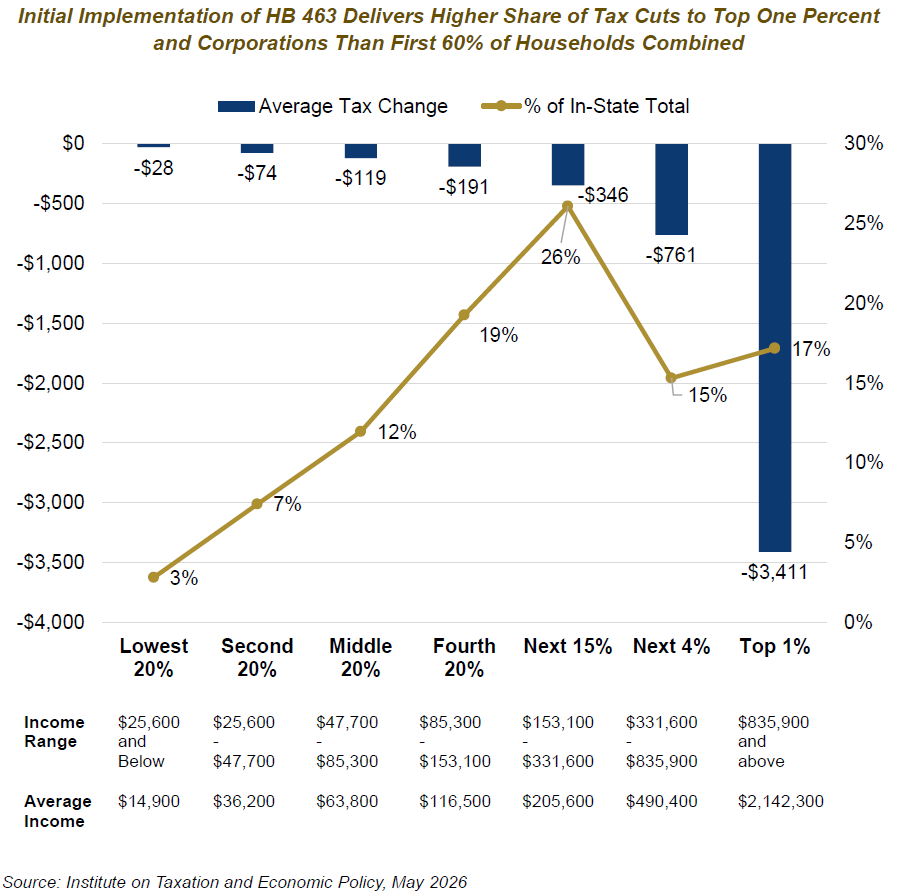

Those in the top one percent (making over $836,000 annually) and out-of-state corporate shareholders alone will see more than $279 million in tax cuts (23% of total) in the first full year of HB 463. This is significantly more than the combined $250 million (21% of total) split between the first 60% of Georgians earning up to $85,000 annually. Out-of-state corporate shareholders would see 7% of total benefits ($85.8 million), while those in the top one percent receive 16% of $1.2 billion in tax cuts, including $191.3 million in personal income tax cuts and $2.2 million in corporate income tax cuts.

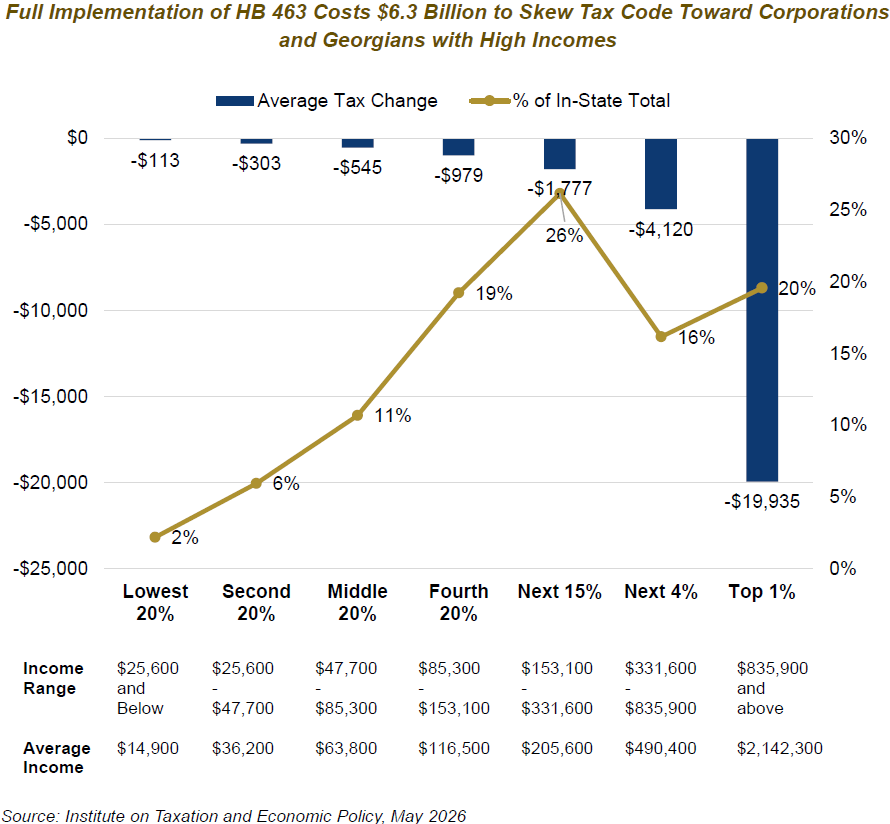

If the bill is fully implemented, this disparity would widen further, with $1.6 billion (26% of total) delivered to the top one percent and out-of-state interests in comparison to just $1.1 billion (17% of total) for the first 60% of Georgia households. Under the full bill, $514.9 million would go to out of state corporate interests (8%), while $1.1 billion goes to the top one percent of income earners (17%).

Retroactive to January 2026, the legislation lowers Georgia’s flat personal and corporate income tax rate from 5.19% to 4.99%. Beginning in January 2027, the standard deduction increases from $12,000 for singles and $24,000 for married couples to $15,000 and $30,000, while the dependent exemption increases from $4,000 to $5,000 and the retirement exclusion for seniors increases from $65,000 to $70,000 per person. Deductions, exemptions and exclusions allow Georgians to exempt a certain amount of their income from state income taxes. For example, under a 4.99% rate, a $3,000 increase to the standard deduction is worth up to $150 annually. For three years (2026-28), the legislation temporarily exempts up to $1,750 in tipped and overtime income from state income taxes.

Over the next eight years (2027-34), the legislation also lays out a framework to reduce the state’s personal and corporate income tax rate to 3.99% (lowered 0.125% per year), while increasing the standard deduction to $30,000 for single filers ($375 annually) and $36,000 for married couples ($750 annually) and increasing the dependent exemption to $6,000 ($125 annually).

These reductions should only take place if the state meets three triggers, including (1) raising higher net revenues in the prior year than during each of the preceding three fiscal years, (2) the governor issuing a revenue estimate for the next fiscal year that is at least 3% above the revenue estimate for the current fiscal year and (3) maintaining sufficient funding in the Revenue Shortfall Reserve (RSR) to cover the projected decrease in revenue from pending tax changes. However, due to the immediate deficit-causing impact of the legislation, it is unlikely that future decreases to the income tax rate, standard deduction or dependent exemption would be implemented without further legislative action and corresponding spending or revenue changes.

Ultimately, most Georgians are unlikely to notice significant savings from the income tax cuts enacted through HB 463. The approximately one million households in the lowest earning 20% of Georgians will see just $28 per year in average tax cuts, while middle income Georgians see an average of $119 annually. On the other hand, those in the top one percent will benefit from an average tax cut of $3,400 next year. For many Georgians, such as those with children enrolled in public schools or facing urgent health needs, the relatively small scale of these tax cuts pales in comparison to funding stripped from the FY 2027 budget to cover their cost.

If the legislation is fully implemented over the next eight years, those savings would grow but at a massive cost for the state, which has no set plan to recoup or offset the additional $5.1 billion in revenue necessary for HB 463 to be fully enacted. For context, that is more than Georgia spends on its university and technical college systems ($4.4 billion) and nearly as much as it costs the state to insure about 1.8 million Georgians through Medicaid ($5.5 billion). These costs would go towards providing an average of $19,935 in tax cuts to those in the top one percent in comparison to an average annual tax cut of less than $550 for middle-income households. Although the last-minute cuts made by Gov. Kemp are severe, they do not come close to the level of austerity required for the full bill to go into effect.

Conclusion

Georgia’s governor has broad authority to require agencies to reserve appropriations for budget reductions and to withhold agency allotments to maintain spending within projected revenues, which the governor also holds unilateral authority to set in establishing the state’s revenue estimate.[12] In practice, this authority offers wide latitude for the governor to exercise control over funding allotted to state agencies without issuing more traditional line-item vetoes to entirely strike spending from the budget. Nevertheless, Gov. Kemp’s extensive use of this authority overrides legislative control over state appropriations and threatens to disrupt the balance of power in setting fiscal policy between the state’s executive and legislative branches of government.

It is clear that the General Assembly recklessly approved HB 463 without establishing a plan to address billions in potential revenue losses facing the state. Lawmakers also passed additional measures that will cost the state revenue, including HB 328 which increases the cap on annual private school voucher tax credits from $120 million to $150 million.[13] As a result, Georgia is now facing a structural deficit that future state leaders must address.

At the same time, the state is currently spending down about $6.2 billion in one-time funds which will reduce general funds available in the RSR and unobligated surplus account from approximately $15 billion down to an estimated $8.7 billion. This spend-down is occurring as HB 463 also increases the limit on the amount of funds that can be stored in the state’s RSR from 15% to 20% of prior year revenues, which is projected to increase its balance from $5.6 billion to $7.4 billion at the end of the 2026 fiscal year.

As a result of this one-time spend down and change to the RSR, the state’s unobligated reserve account will be reduced from approximately $9.3 billion to about $1.3 billion. Notwithstanding this change, state law permits Georgia to spend down up to $4.5 billion in RSR funds, in addition to unobligated surplus funds, as long as it maintains a minimum balance equivalent to eight percent of prior year revenues ($3 billion).

Future lawmakers will need to confront difficult decisions over restoring fairness to the state’s tax code and raising sufficient revenue that Gov. Kemp and members of the General Assembly left unaddressed.

Endnotes

[1] Office of Georgia’s Governor. (2026, May 12). Gov Kemp signs FY 2027 budget. https://gov.georgia.gov/press-releases/2026-05-12/gov-kemp-signs-fy27-budget

[2] Institute on Taxation and Economic Policy. (2026, May).

[3] Hart, A. (2026, April 20). Georgia’s ACA enrollment plunges, raising concerns for rural hospitals. Georgia Recorder. https://georgiarecorder.com/2026/04/20/georgias-aca-enrollment-plunges-raising-concerns-for-rural-hospitals/

[4] GBPI analysis of April 2026 active enrollment data received through Open Records Request to Georgia’s Department of Community Health and of Center on Budget and Policy Priorities data on number of uninsured adults in Georgia’s coverage gap by work status. https://www.cbpp.org/research/health/closing-medicaid-coverage-gap-would-provide-over-15-million-uninsured-adults-path

[5] Medicaid cuts threaten to close South Georgia autism therapy clinics. (2026, May 5). WTXL ABC 27 Tallahassee News. https://www.wtxl.com/news/local-news/in-your-neighborhood/thomas-county/medicaid-cuts-threaten-to-close-south-georgia-autism-therapy-clinics

[6] Tanner, K. (2026, January 21). Department of Behavioral Health and Developmental Disabilities budget overview [Testimony for Joint Appropriations Committee starting at 18 minutes]. https://www.youtube.com/watch?v=PaNTtq8ks94

[7] Liacko, A. (2025, October 28). Lavonia Hospital closes labor and deliver unit, leaving rural families in crisis. CBS News. https://www.cbsnews.com/atlanta/news/lavonia-hospital-closes-labor-and-delivery-unit-leaving-rural-families-in-crisis/; Georgia Health Initiative (2025, November). Impact of Federal Policy Changes to Georgia’s health Care Landscape. _https://georgiahealthinitiative.org/wp-content/uploads/2025/11/Impact-of-Federal-Policy-Changes-to-Georgias-Health-Care-Landscape_Report_November_2025.pdf

[8] Georgia Department of Education. (n.d.) District Financial Information (2025). https://georgiainsights.gadoe.org/dashboards/district-financial-information/

[9] Kramon, C. (2026, February 27). Georgia’s child welfare system remains shaken after projected $85.7 million budget shortfall. The Associated Press. https://apnews.com/article/georgia-child-welfare-budget-shortfall-candice-broce-4b4e55a449b16f7ee51040f9e6105373

[10] Wickert, D. (2026, May 5). Georgia lawmakers vowed to cut tax breaks. They approved more instead. The Atlanta Journal-Constitution. https://www.ajc.com/politics/2026/05/georgia-lawmakers-vowed-to-cut-tax-breaks-they-approved-more-instead/

[11] Ibid.

[12] O.C.G.A. § 45-12-86.

[13] House Bill 328, as signed by Gov. Kemp, May 11, 2026.