During the 2026 legislative session, members of the General Assembly have introduced an array of proposals that would dramatically change how Georgia raises and budgets public funds. Gov. Kemp has proposed accelerating the multi-year tax cut legislation enacted during his first term to reach a flat personal and corporate income tax rate of 4.99%. Some state leaders have proposed fully eliminating or significantly scaling back the income tax, Georgia’s largest source of revenue. Other legislators have zeroed in on how structural reforms to the state’s revenue system could meaningfully address child poverty while putting more money in the pockets of working and middle-class families.

Lawmakers seeking sweeping changes to the cornerstone of the state’s revenue system would be wise to consider the broader fiscal implications. Last year, Georgia raised more than half ($19.5 billion) of general fund revenues from income taxes.[1] That revenue was split between $16.2 billion in personal income taxes (47% of general funds) and $3.3 billion in corporate income tax collections (9% of general funds).

With the seventh lowest level of state taxes per person in the nation, Georgians paid an average of $3,009 in overall taxes in 2024.[2] Georgians also continue to outperform our neighbors economically, earning a higher median income than residents of Florida, Tennessee and Texas.[3] Looking ahead, state leaders must carefully weigh how trade-offs from abandoning Georgia’s balanced revenue system could cause irreparable harm to the state’s economy and residents through deep cuts to education and health care and with offsetting tax increases that transfer vast amounts of wealth from working and middle-class Georgians to those already at the top of the economic ladder.

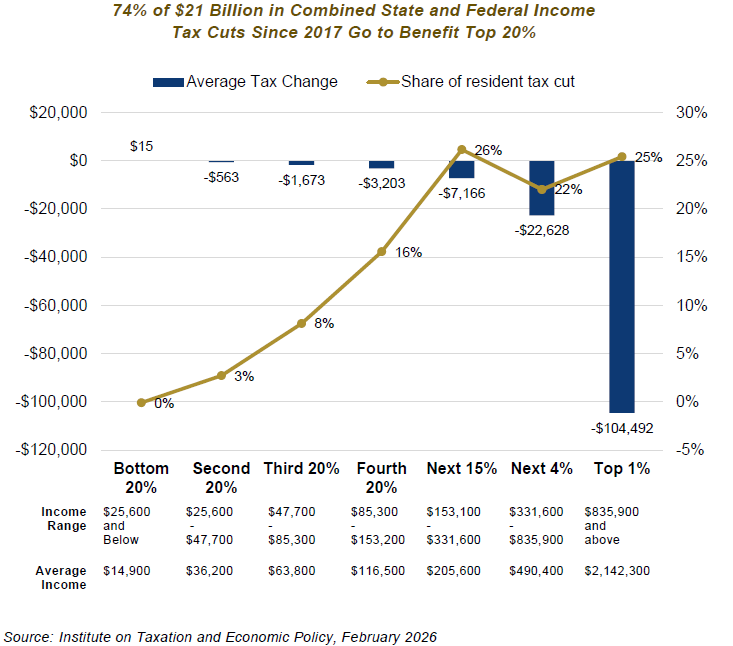

Over the past decade, Georgia lawmakers have approved $6.5 billion in personal and corporate income tax reductions. On top of this, the federal government has reduced taxes by $14.5 billion through the Tax Cuts and Jobs Act (TCJA) of 2017 and H.R. 1 of 2025. Out of $21 billion in recent tax cuts, the 20% of households who earn the most (over $153,000 per year) have gained $15.4 billion or 74% of the benefits. The first 80% of Georgians who earn low-to-middle incomes have gained roughly the same share of benefits as the small group earning more than $836,000 who comprise the top 1%, receiving 26% and 25% of total tax cuts, respectively. Now legislators are debating whether to double down on highly regressive tax cuts that further redistribute resources to those at the very top of the economic ladder.

Comparing Income Tax Bills Introduced During 2026 Session

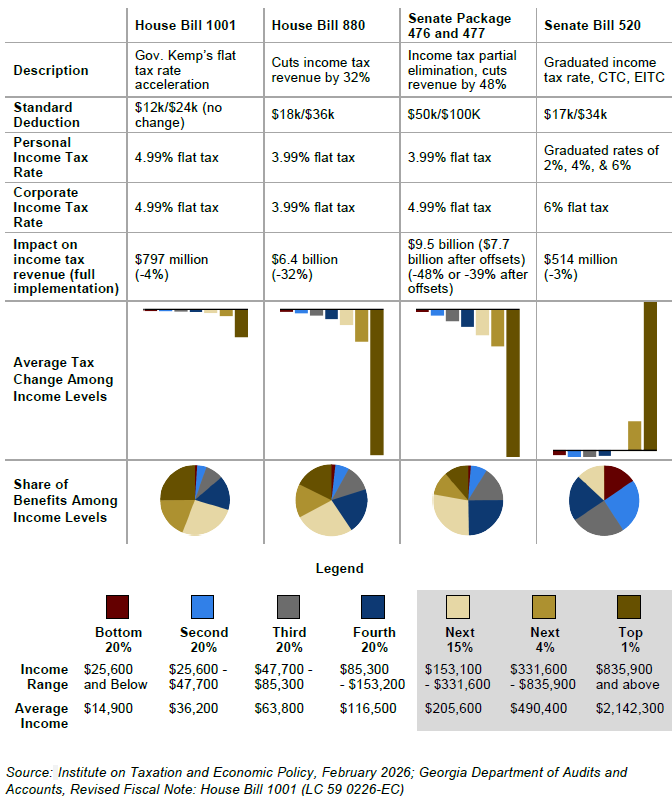

Income tax cut proposals like House Bill 1001, House Bill 880 and Senate Bill 477 focus on cutting Georgia’s income tax from the top down by reducing the state’s flat income tax rate. This is an extremely costly and highly inefficient way to deliver meaningful savings to most Georgians. Rate cuts disproportionately benefit those who earn the highest incomes because filers do not start seeing savings from cuts to the existing flat income tax rate until after they arrive at their state taxable income by applying any deductions, exclusions and other eligible tax credits. For example, under current law, a family of four with two children does not start paying income taxes until after they exceed $32,000 in income. A better approach is to cut taxes from the bottom up through increases to the standard deduction, tax credits that help families afford the cost of raising children and reduce poverty, and by improving the structure of the state’s income tax to prioritize working and middle-class Georgians.

Income tax cut proposals like House Bill 1001, House Bill 880 and Senate Bill 477 focus on cutting Georgia’s income tax from the top down by reducing the state’s flat income tax rate. This is an extremely costly and highly inefficient way to deliver meaningful savings to most Georgians. Rate cuts disproportionately benefit those who earn the highest incomes because filers do not start seeing savings from cuts to the existing flat income tax rate until after they arrive at their state taxable income by applying any deductions, exclusions and other eligible tax credits. For example, under current law, a family of four with two children does not start paying income taxes until after they exceed $32,000 in income. A better approach is to cut taxes from the bottom up through increases to the standard deduction, tax credits that help families afford the cost of raising children and reduce poverty, and by improving the structure of the state’s income tax to prioritize working and middle-class Georgians.

Measures like Senate Bill 520 would help to level the playing field by addressing the fact that 95% of working and middle-income families currently pay a higher share of their income in total state and local taxes, on average, than those at the very top of the economic ladder.[4] Instead of doubling down on regressive income tax cuts for those making the highest incomes and corporations, policymakers should focus their attention on savings for working and middle-class families. State leaders must also recognize that large scale tax cuts without offsetting revenues directly threaten funding for health and education, which comprise three-quarters of state spending in FY 2027.

House Bill 1001

The 2026 legislative session opened with Gov. Kemp’s proposal to reduce the state’s flat personal and corporate income tax rate to 4.99%, retroactively effective as of January 2026. This would mark the final step of the flat tax legislation approved in Gov. Kemp’s first term through House Bill 1437 (2022), three years ahead of the timeline initially approved.[5]

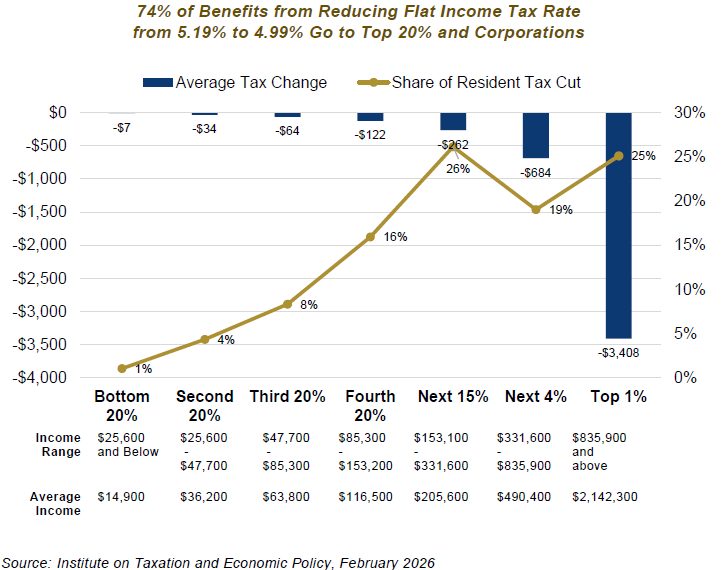

Under House Bill 1001, the state’s personal and corporate income tax rate would both shift from 5.19% to 4.99% at an estimated cost of $797 million over a full year. [6] Approximately 74% of these benefits ($593 million) would go to the 20% of Georgia households that earn the most and corporations, while the remaining 80% of Georgians would see average savings of less than $122 in per year ($204 million total). The state anticipates that the legislation would reduce corporate and personal income tax revenues by $948 million in Fiscal Year (FY) 2027 (5%) and $797 million in FY 2028 (4%).[7]

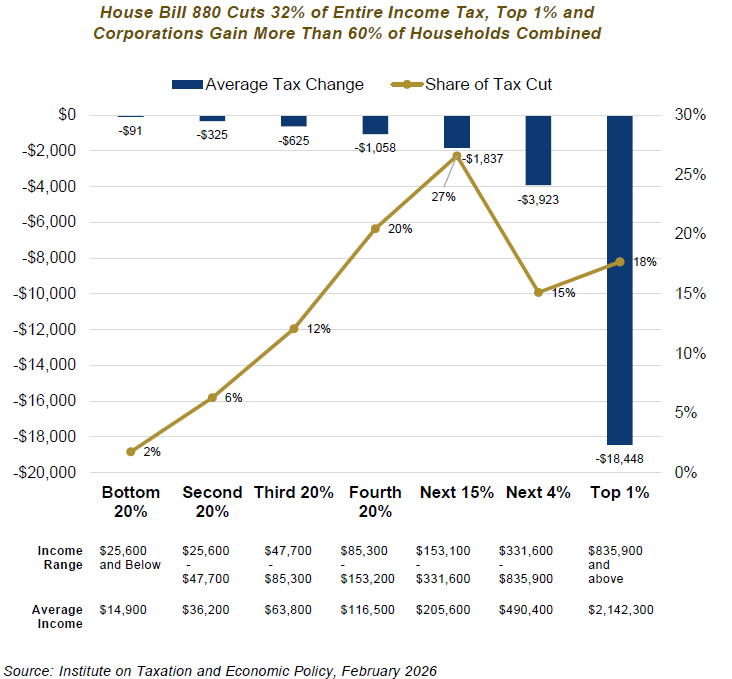

House Bill 880

GBPI estimates that House Bill 880 would cut total personal and corporate income tax revenues by about 32% by lowering the top personal and corporate income tax rate to 3.99%, increasing the state standard deduction from $12,000 to $18,000 for individuals and from $24,000 to 36,000 for married couples, increasing the dependent exemption by $2,000 and increasing the retirement exclusion by $5,000 per person. The legislation phases in these changes over 10-years.

About 63% of $6.4 billion in benefits ($4 billion) would go to the top 20% of Georgians who earn the highest incomes and corporations. Georgians in the top 1% who earn more than $836,000 per year would see an average savings of $18,500 for a total in excess of $1 billion annually, along with more than $500 million going out of state to benefit corporate interests.

Overall, the top 1% of earners and out of state corporations would benefit from $1.6 billion in tax cuts, significantly more than the cumulative total in tax reductions for the first 60% of Georgians who earn low-to-middle incomes. These three million working and middle-class households would see an average savings of less than $400 per year for a total of $1.2 billion.

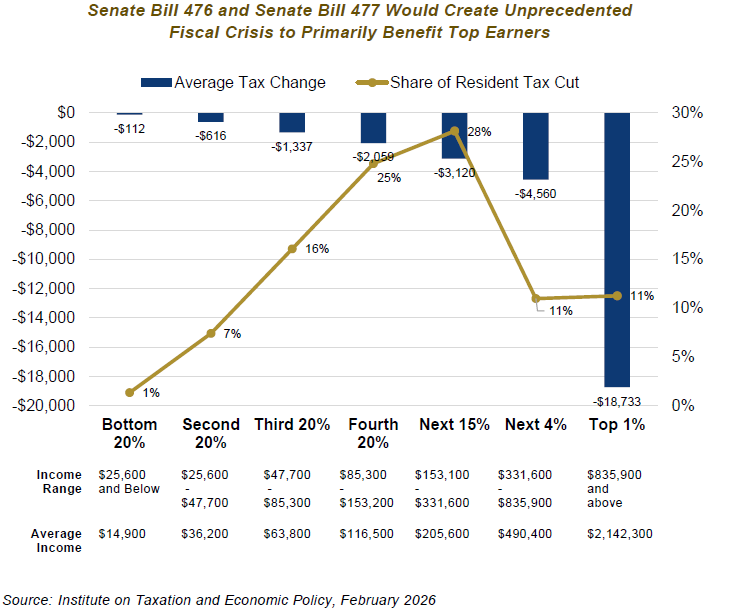

Senate Bill 476 and Senate Bill 477

After a rushed legislative process with no fiscal note to assess the cost of the measures, the Senate passed a partial income tax elimination package that includes Senate Bill 476 and Senate Bill 477. The same measures were also passed through the Senate as House Bill 134 and House Bill 463 to satisfy constitutional constraints that require revenue legislation to originate in the state House.

This legislative package would cut the personal income tax rate from 5.19% to 3.99% (Senate Bill 477), cut the corporate income tax rate from 5.19% to 4.99% (Senate Bill 476) and increase the state standard deduction to $50,000 for individuals and to $100,000 for couples (Senate Bill 476). Although the package is split into two bills, its structure matches the recommendations of the special study committee appointed by Lt. Governor Jones that was charged with producing a plan to fully eliminate Georgia’s personal income tax, which the committee proposed completing by 2032, despite not issuing specific recommendations to replace billions in lost revenue.[8]

Notwithstanding the legislation’s sweeping impact, the measures were passed without fiscal notes. However, a fiscal note produced after the legislation was passed by the Senate estimates that the revenue raising provisions included in Senate Bill 476 could generate up to $1.8 billion by 2031 through eliminating a series of income and sales tax breaks.[9] This includes ending sales tax exemptions for data centers and technology companies, eliminating tax exemptions for insurance companies, cutting the state’s affordable housing tax credit in half and repealing about two dozen other income and sales tax credits or exemptions.[10] In January 2032 all other individual and corporate tax credits would expire without further action by the General Assembly.

The package’s tax cutting provisions would cost $9.5 billion if fully implemented, which is equivalent to 48% of all income tax revenues. Combining this figure with revenue estimates provided by the fiscal note means that Georgia could see an annual budget deficit greater than $7.7 billion if these bills are enacted (39% of all income tax revenues).[11] That is more than Georgia spends to insure more than two million residents through Medicaid. It’s also more than the state spends on all higher education programs to educate more than 500,000 students. Not only would this legislative package jeopardize funding for programs that all Georgians rely on by creating the largest budget deficit in modern state history, but the majority of tax cuts would go to benefit the 20% of Georgians who already earn the most money.

Earlier this year, the final report released by the special study committee appointed to study eliminating the income tax called into question the potential benefits of pursuing a 0% state income tax rate. The report noted that the first 71% of Georgia households with taxable incomes of less than $100,000 pay just 26% of all income taxes, while 74% of income taxes are generated from those earning upwards of six-figures annually. The offsets proposed through Senate Bill 476 would fail to raise more than one-fifth of the revenues necessary to eliminate the income tax, so future proposals are likely to include a broad array of tax increases or require massive spending cuts to satisfy Georgia’s constitutional requirement for a balanced budget.

A recent report from the White House Council of Economic advisors encouraged states to consider sales taxes as a substitute for income taxes.[12] To avoid raising Georgia’s sales tax rate directly, legislative proponents for eliminating Georgia’s income tax have repeatedly claimed that the state offers “special credits and exemptions totaling approximately $30 billion in estimated forgone revenue” that could be used offset the $16.2 billion cost of eliminating the state’s personal income tax.[13]

This “$30 billion” figure has grown slightly to $33.4 billion in total tax expenditures for FY 2027.[14] However, at least $5.9 billion of these tax breaks would not exist under a 0% income tax rate. That leaves $27.5 billion in total tax breaks for FY 2027, with 87% of these tax expenditures ($23.8 billion) comprised of sales tax exemptions that largely help to drive down the cost of living.[15] About $16 billion in these Georgia sales tax exemptions are for purchases related to health care, schools, groceries, business inputs and construction. Another $6.5 billion of these sales tax breaks are for other services Georgians rely on.

Simply put, it would not be possible to eliminate most state tax expenditures without raising the cost of living for Georgians through higher sales taxes. If Georgia switches to a sales tax-based revenue system similar to Florida, Tennessee or Texas, which all raise at least 75% of general fund revenues from sales taxes, it is estimated that the first 80% of Georgia households would see an average tax increase of $1,000 per year.[16]

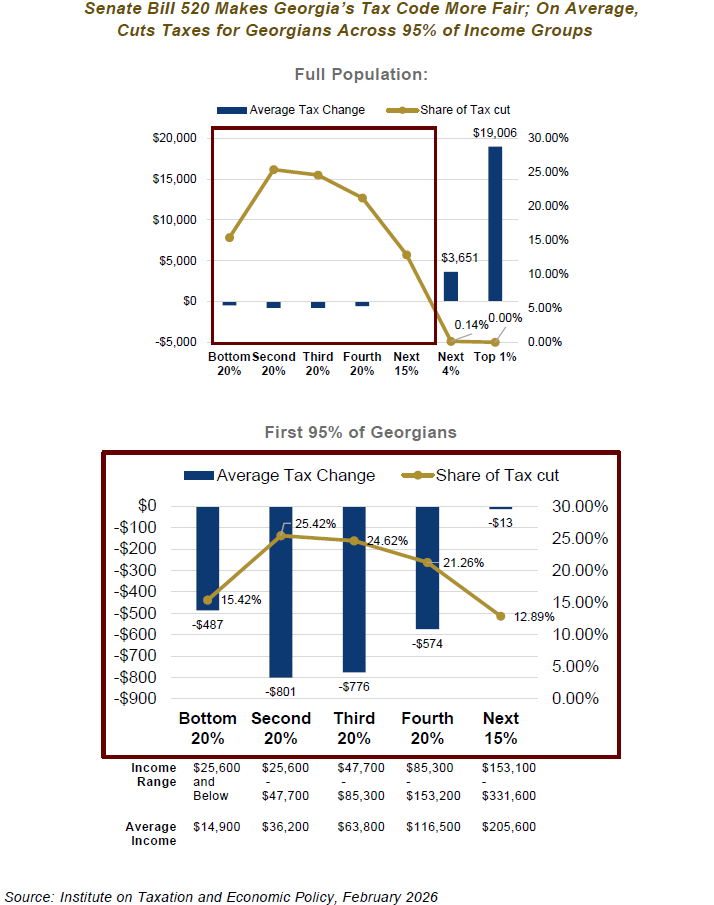

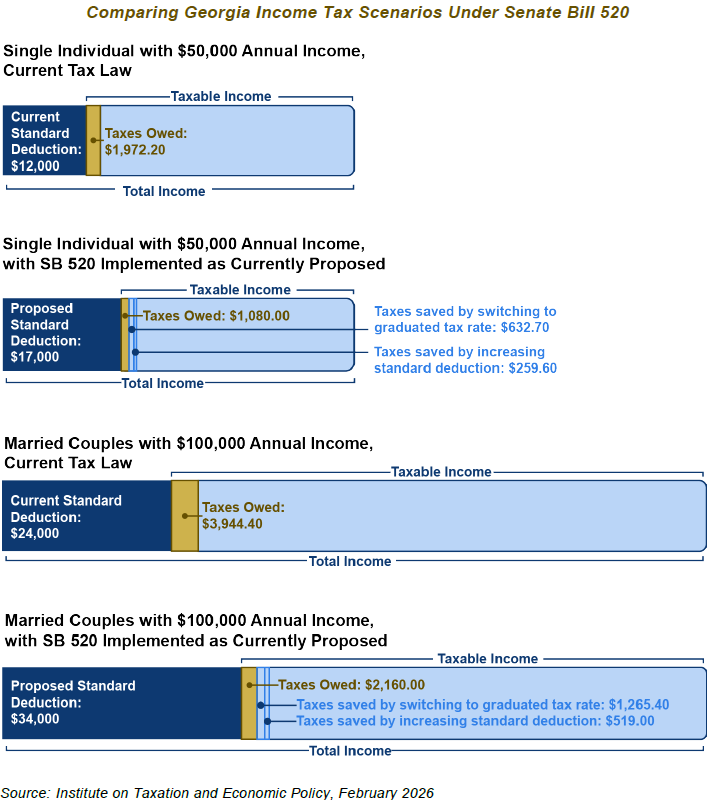

Senate Bill 520

Senate Bill 520 proposes a series of common-sense measures to make Georgia’s tax code more fair. The legislation would shift Georgia from a flat tax system to a graduated personal income tax system, with income taxed at rates that gradually increase from two to six percent. The legislation increases the standard deduction to $17,000 for individuals and $34,000 for married couples. It would also increase Georgia’s dollar-for-dollar Child Tax Credit by $1,000 per child to $1,250, make it fully refundable, and create a refundable Earned Income Tax Credit (EITC) worth 20% of the federal level (up to $1,650).

On average, the first 95% of Georgians who earn up to $331,000 per year would benefit from tax cuts, with the first 80% of households making up to $153,000 saving the most. In comparison to current law, Senate Bill 520 cuts income taxes on the first $50,000 for single filers and the first $100,000 for married couples by up to 45% by taxing income at lower graduated rates and increasing the standard deduction. Multiplying Georgia’s existing Child Tax Credit by a factor of five and enacting an EITC would add up to $4,000 in fully refundable benefits for a family of four.

On average, the first 95% of Georgians who earn up to $331,000 per year would benefit from tax cuts, with the first 80% of households making up to $153,000 saving the most. In comparison to current law, Senate Bill 520 cuts income taxes on the first $50,000 for single filers and the first $100,000 for married couples by up to 45% by taxing income at lower graduated rates and increasing the standard deduction. Multiplying Georgia’s existing Child Tax Credit by a factor of five and enacting an EITC would add up to $4,000 in fully refundable benefits for a family of four.

The proposal also includes lifting Georgia’s tobacco user fee to the national average, eliminating the state’s tax credit for vouchers as well as taxing corporations and incomes over $208,000 for single Georgians and $416,000 for couples at an effective rate closer to 6%. Under Senate Bill 520, even the relatively small share of taxpayers earning incomes above this threshold would continue to pay lower state taxes, on average, than in 2017. These offsets make the plan essentially revenue neutral with a net cost of just $514 million, despite significantly cutting taxes for most Georgians. In fact, because Gov. Kemp’s revenue estimate for FY 2027 factors in the higher cost of implementing House Bill 1001, enacting Senate Bill 520 would result in higher-than-expected revenues.

Because Georgians would pay income taxes at rates that progressively increase from between 2% and 6%, single Georgians would save $633 on the first $30,000 of taxable income, while married taxpayers would see $1,265 in savings on their first $60,000 of taxable income in comparison to Georgia’s current flat income tax rate of 5.19%.

Increasing Georgia’s standard deduction by $5,000 for single Georgians and $10,000 for married couples adds up to $260 in additional benefits for single filers and $519 for married couples for a total of $892 and $1,784, respectively. These changes help to protect Georgians earning less than $208,000 (single) or $416,000 (married) from seeing a tax increase due to the legislation’s proposed phase-out of the standard deduction for those earning incomes in the top 5%.

Since 2017, those with incomes in the top 1% have seen an average of $25,500 in state tax cuts and an additional $78,800 in federal tax cuts. Whereas those in the next 4% have seen an average of than $5,140 in state tax cuts and $17,500 in tax cuts at the federal level. This is a significantly greater amount of savings than the $690 in average state tax cuts and approximately $980 in federal tax cuts directed to middle-income households over the past decade.

Since 2017, those with incomes in the top 1% have seen an average of $25,500 in state tax cuts and an additional $78,800 in federal tax cuts. Whereas those in the next 4% have seen an average of than $5,140 in state tax cuts and $17,500 in tax cuts at the federal level. This is a significantly greater amount of savings than the $690 in average state tax cuts and approximately $980 in federal tax cuts directed to middle-income households over the past decade.

Under Senate Bill 520, Georgians at all income levels, including those in the top 1%, would continue to pay significantly less in income taxes at both the state and federal levels than in recent years due to $6.5 billion in state income tax cuts and $14.5 billion in federal income tax cuts adopted since 2017. Approximately 47.5% of this total, equivalent to about $10 billion in combined annual tax cuts, has gone to benefit those in the top 5% alone. Rather than cutting state revenues to further enrich those at the top of the economic ladder, Senate Bill 520 responsibly reforms the state’s income tax code to put more money back in the hands of working and middle-class Georgians.

Endnotes

[1] Georgia State Accounting Office. (2025, October 15). State of Georgia Revenue and reserves report, fiscal year ended June 30, 2025. https://sao.georgia.gov/swar/grr

[2] U.S. Census Bureau. (2025, April). 2024 Annual survey of state government tax collections and 2024 state intercensal population estimate, as calculated by author. https://www.census.gov/programs-surveys/stc/data/datasets.html; https://www.census.gov/data/tables/time-series/demo/popest/2020s-state-total.html

[3] U.S. Census Bureau. (2025, September). Household income in states and metropolitan areas: 2024. https://www.census.gov/library/publications/2025/demo/p60-286.html

[4] Kanso, D. (2025, November 17). Breaking the bank: Eliminating the state income tax harms most Georgians and increases the cost of living. Georgia Budget & Policy Institute. https://gbpi.org/breaking-the-bank-eliminating-the-state-income-tax-harms-most-georgians-and-increases-the-cost-of-living/?_gl=1*xqing0*_up*MQ..*_ga*MTg4NTYyMDQzNy4xNzY0NjA4NDky*_ga_ZWZC5HZ1YJ*czE3NjQ2MDg0OTIkbzEkZzEkdDE3NjQ2MDg1MDkkajQzJGwwJGgw#_edn15

[5] House Bill 1437 (2022), as signed by Gov. Kemp

[6] Georgia Department of Audits & Accounts. (2026, February 24). Revised fiscal note: House Bill 1001 (LC 59 0226-EC)

[7] Ibid.

[8] Georgia Senate Special Committee on the Elimination of Georgia’s Income Tax: Final report and recommendations. (2026, January). Georgia Senate. https://www.legis.ga.gov/api/document/docs/default-source/senate-study-committees-document-library/2026-special-committee-to-eliminate-income-tax-final-report.pdf

[9] Department of Audits and Accounts. (2026, March 5). Fiscal Note, Senate Bill 476 (LC 59 0312)

[10] Senate Bill 476 (2026), as passed by the Senate

[11] Department of Audits and Accounts. (2026, March 5). Fiscal Note, Senate Bill 476 (LC 59 0312); Georgia Senate Special Committee on the Elimination of Georgia’s Income Tax: Final report and recommendations. (2026, January). Georgia Senate. https://www.legis.ga.gov/api/document/docs/default-source/senate-study-committees-document-library/2026-special-committee-to-eliminate-income-tax-final-report.pdf

[12] Tuccille, J.D. (2026, February 2). Dumping state income taxes could mean high sales Taxes—or an opportunity for smaller government. Reason. https://reason.com/2026/02/02/dumping-state-income-taxes-could-mean-high-sales-taxes-or-an-opportunity-for-smaller-government/

[13] Georgia Senate Special Committee on the Elimination of Georgia’s Income Tax: Final report and recommendations. (2026, January). Georgia Senate. https://www.legis.ga.gov/api/document/docs/default-source/senate-study-committees-document-library/2026-special-committee-to-eliminate-income-tax-final-report.pdf

[14] Georgia Department of Audits & Accounts. (2026, January 12). Georgia tax expenditure report for FY 2027. https://opb.georgia.gov/budget-information/budget-documents/tax-expenditure-reports

[15] Kanso, D. (2026, January 23). Overview of Georgia’s budget for Amended Fiscal Year 2026 and the full 2027 Fiscal Year. Georgia Budget & Policy Institute. https://gbpi.org/overview-of-georgias-budget-for-amended-fiscal-year-2026-and-the-full-2027-fiscal-year/

[16] Kanso, D. (2025, November 17). Breaking the bank: Eliminating the state income tax harms most Georgians and increases the cost of living. Georgia Budget & Policy Institute. https://gbpi.org/breaking-the-bank-eliminating-the-state-income-tax-harms-most-georgians-and-increases-the-cost-of-living/?_gl=1*xqing0*_up*MQ..*_ga*MTg4NTYyMDQzNy4xNzY0NjA4NDky*_ga_ZWZC5HZ1YJ*czE3NjQ2MDg0OTIkbzEkZzEkdDE3NjQ2MDg1MDkkajQzJGwwJGgw#_edn15