Sign up to receive a physical copy of the Georgia Budget Primer here.

View more sections of the 2027 budget primer here.

![]()

Georgia’s Recent History Sets Stage for Next Chapter

Georgia’s $38.5 billion budget for FY 2027 is Gov. Kemp’s final state budget as governor. After adjusting for changes in population and inflation over the past eight years, the FY 2027 budget represents a slightly lower level of per person spending ($3,351) than the state appropriated in FY 2020 ($3,374).

Shortly after Gov. Kemp took office in 2019, he led the General Assembly to cut over 1,000 vacant state jobs in the FY 2020 state budget. The following year, in anticipation of a sudden economic recession caused by the COVID-19 pandemic, Georgia cut $2.2 billion from the FY 2021 state budget.

Over the next five years (FY 2022-2026), Georgia felt the effects of conservative state revenue estimates and massive levels of federal spending intended to avoid an economic downturn. The combined effects of these policies helped to overfill Georgia’s state reserve accounts. These reserve accounts have since been tapped repeatedly to fund billions in one-time tax rebates, capital projects and other state investments.

Between FY 2024 and FY 2026, Georgia spent more than $4.6 billion in surplus funds on infrastructure and capital projects, reducing inflation-adjusted debt service payments by 35% per person. Over the past five fiscal years, the state also issued more than $6 billion in one-time tax rebates through the state income tax and local property taxes.

Kemp’s eight years as Georgia’s governor are characterized by this spending pattern, along with growth in higher education funding that led to the creation of a need-based scholarship, reduced fees and enhanced funding for HOPE scholarships and grants. However, the fastest growing area of spending over the past eight years is health, which has seen a 12%-inflation adjusted spike in per-person costs despite the state largely ignoring that Georgia maintains the nation’s second highest rate of uninsured residents and glaring deficits in services.

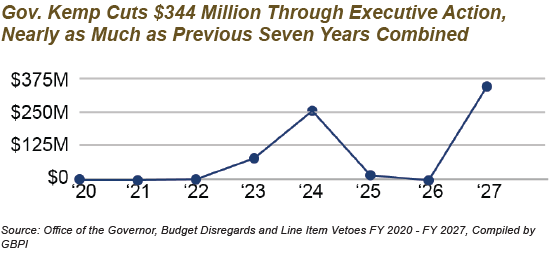

Gov. Kemp Unilaterally Cuts $344 Million in FY 2027 Spending, Nearly as Much as Previous Seven Years Combined

In signing the FY 2027 budget, Gov. Kemp issued a combined 157 budget disregards and line-item vetoes to cut more than $344 million in spending. Budget disregards act similarly to line-item vetoes and allow the governor to withhold funding for certain areas of the budget approved by the General Assembly. Unlike line-item vetoes, they are considered non-binding, meaning that the funds remain part of the budget but are not released to agencies for spending. When the General Assembly reconvenes to write the Amended Fiscal Year (AFY) 2027 budget, lawmakers can reconsider whether to approve these expenditures.

In total, Gov. Kemp disregarded more than $329.4 million and vetoed $14.8 million for FY 2027. This compares to $342.3 million in combined budget disregards and $16.3 million in line-item vetoes issued over the previous seven years.

Most of the changes made this year removed funding for public education ($87.5 million), health care ($81.8 million) and human services ($15.8 million).

Gov. Kemp made clear that these spending cuts are intended to partially offset the cost of more than $1.2 billion in income tax cuts approved this year. On average, households will see $196 in savings next year from these cuts, while countless Georgians are harmed by budget cuts to essential services ranging from student transportation to domestic violence and sexual assault centers.

Who is Georgia’s Budget For?

Georgia’s budget for FY 2027 directly affects the quality of life for all 11.5 million Georgians across the state. The $38.5 billion state budget for FY 2027 amounts to $3,351 in per-person spending. Accounting for inflation, this is a decrease of $23 per person since Gov. Kemp’s first full year budget in FY 2020.

The majority of the budget is allocated to core investments in the state’s economic future, including education, health care and transportation.

The Georgia state budget:

- Provides health care coverage and services through Medicaid and PeachCare for over 1.8 million Georgians with low incomes who are seniors, disabled, children or parents ($5.5 billion in FY 2027)

- Educates 1.7 million K-12 students while employing over 141,000 teachers and administrators in our 2,300 K-12 public schools ($14.2 billion in FY 2027)

- Educates 503,600 students enrolled in Georgia public colleges, universities and technical colleges, while employing 64,000 faculty and staff across 47 institutions ($5.8 billion in FY 2027)

- Employs 78,335 full-time state workers (FY 2025) across government agencies such as health care, education and child services, up slightly from 78,199 full-time employees in 2020. ($4.3 billion for FY 2025)

- Helps feed about 700,000 Georgia households by contributing to the SNAP administration costs. The federal government pays for the SNAP benefits itself. (Georgia is contributing $53.2 million in FY 2027)

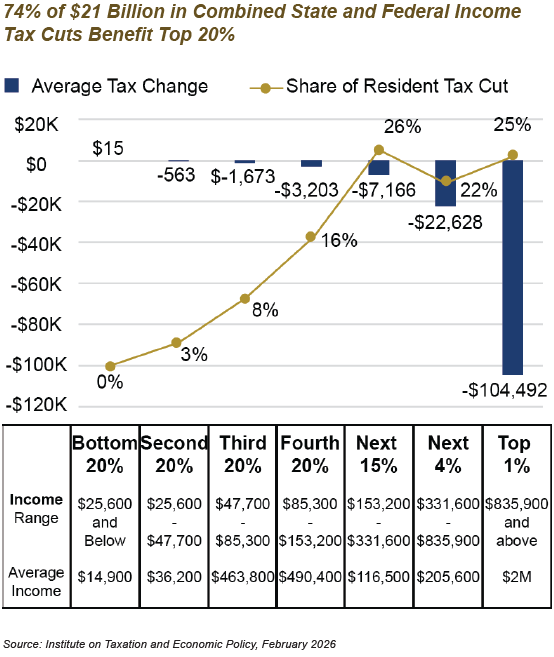

Since 2017, 74% of $21 Billion in Combined State and Federal Income Tax Cuts go to Benefit Top 20%

Between 2017 and 2025, Georgia lawmakers approved $6.5 billion in personal and corporate income tax reductions. On top of this, the federal government has reduced taxes by $14.5 billion through the Tax Cuts and Jobs Act (TCJA) of 2017 and H.R. 1 of 2025. Out of $21 billion in combined recent state and federal tax cuts, the 20% of households who earn the most (over $153,000 per year) have gained $15.5 billion or 74% of the benefits. In comparison the first 60% of Georgians who earn low-to-middle incomes have gained 11% of the benefits ($2.3 billion).

State Prepares for Costly Nine-Year Income Tax Cut Plan

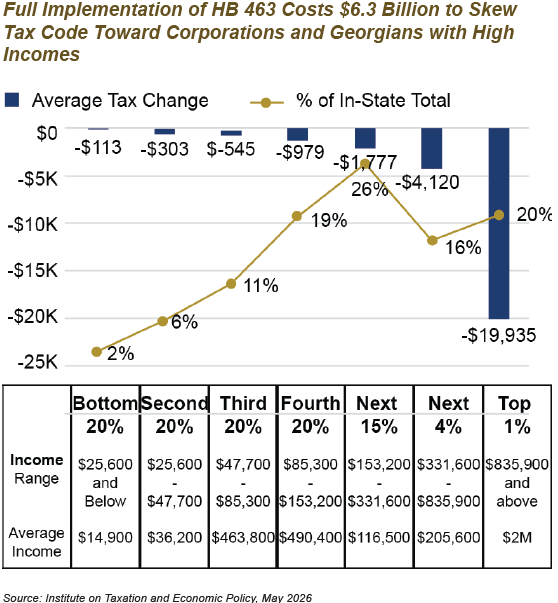

In the 2026 legislative session, lawmakers passed HB 463, enacting a nine-year plan that could eliminate one-third of Georgia’s entire income tax. In its first full year of implementation, at a cost of $1.2 billion, this legislation delivers a larger share of cuts to those in the top 1% and out-of-state corporate interests than to the first 60% of Georgia households combined.

The legislation cuts Georgia’s income tax rate to 4.99%, retroactively beginning January 1, 2026. The legislation also increases the state’s standard deduction to $15,000 for individuals and $30,000 for married couples from $12,000 and $24,000, respectively. Additionally, it increases the state’s dependent exemption by $1,000 and its retirement exclusion by $5,000 per person. For three years, between 2026 and 2028, the legislation exempts up to $1,750 in tipped or overtime income from taxes. The cap on Georgia’s Revenue Shortfall Reserve is also increased from 15% to 20% of the prior year’s revenue collections and the threshold for funds to be spent down is raised from 4% to 8%. HB 463 also authorizes the General Assembly to use surplus funds in excess of this 20% threshold for tax cuts. Over the next eight years, between 2027 and 2034, the legislation calls for Georgia to annually reduce its income tax rate by 0.125 percentage points until it reaches 3.99%, to increase its standard deduction by $375 per person (up to $18,000/$36,000) and to increase its dependent exemption by $125 (up to $6,000).

If the legislation is fully implemented over the next eight years, it would cost the state a massive $6.3 billion, with no set plan to recoup or offset the additional $5.1 billion in revenue required for this measure to be fully enacted. These costs would go towards providing an average of $19,935 in annual tax cuts to those in the top 1%, compared to an average annual tax cut of less than $10 per month for the one million households with the lowest incomes.

As enacted, these reductions will take place automatically if the state meets three triggers, including (1) raising higher net revenues in the prior year than during each of the preceding three fiscal years, (2) the governor issuing a revenue estimate for the next fiscal year that is at least 3% above the revenue estimate for the current fiscal year and (3) maintaining sufficient funding in the Revenue Shortfall Reserve (RSR) to cover the projected decrease in revenue from pending tax changes. However, due to the immediate deficit-causing impact of the legislation, it is unlikely that future decreases to the income tax rate, standard deduction or dependent exemption would be implemented without further legislative action and corresponding spending or revenue changes. Adhering to these safeguards could help to avoid a budget crisis that could be created by making deep cuts to Georgia’s primary source of revenue.

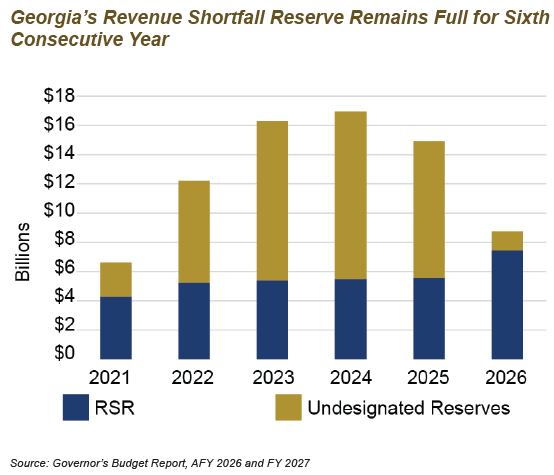

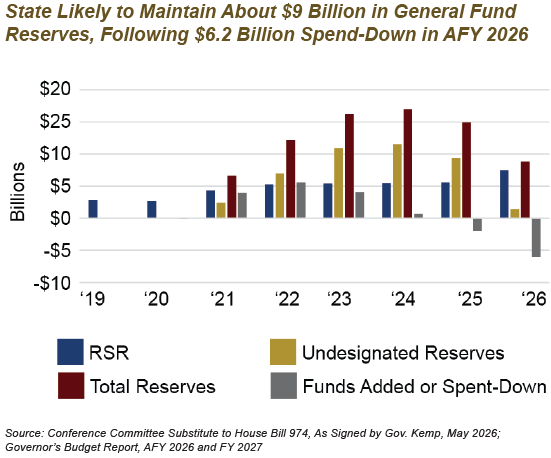

State Savings Account Remains Full After Historic Reserve Spend-Down

The Revenue Shortfall Reserve (RSR), Georgia’s rainy-day fund, provides stability during economic downturns. This fund is like a savings account to pay expenses and maintain services when revenues decline unexpectedly. Maintaining adequate reserves helps Georgia keep its prized AAA bond rating, allowing the state to borrow on the most favorable terms and save in interest payments.

Money is not appropriated into the RSR; the balance grows at the end of each fiscal year automatically if there is surplus state revenue. However, the RSR is limited to a maximum of 20% of prior year revenue, which was increased this year from 15% under HB 463. The minimum balance required to be kept in the RSR is 8% of the prior year’s revenues and the governor is allowed to release any amount over that for appropriation in the state budget. When the RSR is full, remaining surplus funds are referred to as “undesignated reserves” and can be freely spent for any legal purpose.

Since the end of FY 2021, Georgia’s RSR has remained at its maximum level. At the close of FY 2025, Georgia’s RSR stood at $5.6 billion. It is projected to increase its balance to $7.4 billion at the end of the 2026 fiscal year after the General Assembly raised the maximum threshold to 20% of prior year revenues.

In the amended budget for 2026, the state spent down $6.2 billion in undesignated reserves, drawing from its other General Fund reserve account that stood at $9.3 billion at the start of the fiscal year. Because the RSR threshold is simultaneously increasing, Georgia’s undesignated reserve balance is likely to decrease to $1 to 2 billion going into FY 2027.

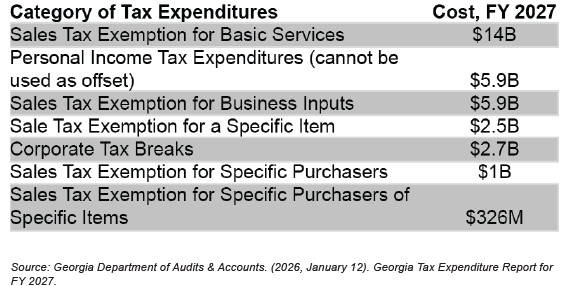

Georgia to Offer $33.4 Billion in Tax Breaks for FY 2027

Georgia offers an array of tax credits, deductions and other tax breaks, also known as tax expenditures. These tax breaks will cost the state approximately $33.4 billion in FY 2027. Some measures provide key protections for families, such as the sales tax exemption on groceries. Alternatively, a range of tax breaks deliver outsized gains to select groups or industries, often with questionable benefit to the state.

Among the $33.4 billion in tax expenditures, sales tax exemptions comprise 87% of the total or $23.8 billion. The remainder includes $5.9 billion in personal income tax credits, $2.7 billion in corporate tax breaks and just under $1 billion from other revenue sources.

Subsidies for film production, data centers, insurance companies and other tax-advantaged industries will cost Georgia about $3.2 billion in lost revenues in FY 2027. However, other Georgia tax expenditures result in lower prices for consumers through lower sales taxes. Sales tax exemptions for health care and prescription drugs, schools, groceries, business inputs and construction amount to more than $16 billion in FY 2027.