This policy report is coauthored by Danny Kanso, Senior Tax & Budget Policy Analyst & Alex Camardelle, Senior Economic Mobility Policy Analyst

![]()

Key Takeaways

- Georgia collects no corporate income tax revenue from the vast majority of businesses.

- Due to the state’s lack of transparency when it comes to evaluating major subsidy programs, it is unclear how many of the jobs created are paying a meaningful living wage and are permanently retained in Georgia.

- Business tax breaks disproportionately favor large corporations over small businesses, which are responsible for a majority of Georgia’s new jobs.

- The state of Georgia estimates it will forgo $10 billion in revenue in FY 2022 due to state tax breaks.

Introduction

Each year, Georgia offers billions in tax breaks that significantly reduce the amount of taxes paid by large corporations and select industries granted preferential tax treatment by state elected officials. Because Georgia also maintains a relatively weak and antiquated corporate income tax structure, the state’s generous tax credit programs allow for large corporations to entirely eliminate their tax liability. In some cases, the combination of special tax breaks and the state’s tax laws can also allow corporations to profit at the expense of Georgia taxpayers.

For the most part, the billions of dollars granted by the state in annual business tax breaks go unaudited, and very little data is publicly available to assess the efficacy of Georgia’s largest tax credit and subsidy programs. However, in the few instances of recent, comprehensive evaluations of Georgia’s tax credit programs, evidence has demonstrated that large corporations benefit from unnecessarily favorable tax treatment at the expense of Georgia families. In fact, in the case of the Film Tax Credit—Georgia’s largest industry-specific tax break—the state Department of Audits found in January 2020 that the state’s economic development agency “significantly overstated” the number of jobs supported by the film tax credit while failing to recognize that hundreds of millions of dollars in tax credits are being approved each year for compensation paid to nonresident workers.[1]

In addition to eroding the corporate income tax base and harming the state budget, in many cases, the state’s tax credit programs represent the transfer of Georgia taxpayer dollars to large out-of-state corporations and top income earners. Granting funds to corporations in this manner leaves less funding for schools, job training and health care programs that have consistently proven to generate better long-term job creation and economic performance than tax credits or subsidies.

| Georgia’s Top Corporate Tax Subsidies Projected to Cost State $1.8 Billion in FY 2022 | ||||||

| FY 2022 Tax Expenditures | Description | Corporate Income Tax (millions) | Individual Income Tax (millions) | Insurance Premium Tax (millions) | Total Cost for FY 2022 (millions) | Year Enacted |

| Film Tax Credit | Up to a 30 percent, dollar-for-dollar tax credit for eligible productions that spend over $500,000. This credit is fully transferable — meaning it can be sold to any taxpayer — and can be applied to offset taxes owed for up to five years | $389 | $679 | – | $1,068 | 2005 (modified in 2015, 2017, 2020) |

| Georgia Job Tax Credit | Statewide tax credit with eligibility criteria based on geographic region, local poverty level and industry type. | $153 | $27 | $7 | $186 | 1989 and 1993 |

| Research Tax Credit | Tax credit for up to 10 percent of research expenses by corporations across a select group of industries that matches a tax credit offered at the federal level | $152 | $7 | – | $160 | 1997 |

| Quality Jobs Tax Credit | Tax credit for eligible corporations that create jobs with 30+ hours per week and pay at least 110 percent of the average county wage | $78 | $1 | – | $79 | 2009 |

| Employer’s Credit for Approved Employee Retraining | Reimburses corporations for the cost of retraining employees | $33 | $18 | – | $51 | 1994 |

| Exclusion of global intangible low-taxed income (GILTI) | Allows corporations to exclude certain foreign earned income from state income taxes | $182 | – | – | $182 | 2018 |

| Manufacturer’s Investment Tax Credit | Tax credit for up to 5 percent of the investment | $22 | $4 | $1 | $25 | 1994 |

| Total | $1,009 | $736 | $7 | $1,752 | ||

Source: Department of Audits and Accounts, Georgia Tax Expenditure Report for FY 2022

Tax Credits and Subsidies Help Corporations Pay Fewer Taxes and Profit from the State

To fund services, programs and other functions of state government, Georgia primarily relies on a mix of income taxes (53 percent of state General Funds, or $13.6 billion), assessed on both people and corporations, and sales taxes (26 percent, or $6.7 billion). Although the state maintains a flat corporate income tax of 5.75 percent, many corporations are able to take advantage of a wide range of subsidies, tax credits and loopholes built into state law that allow businesses to reduce the amount of taxes owed to the state. Furthermore, a mechanism in the state tax code referred to as “transferability” allows corporations that owe nothing in state taxes to sell credits issued by the state to other businesses or individuals, who are then able to pay their own taxes at a reduced cost despite having no involvement in the economic activity for which the tax credit used was initially awarded.[2]

In part because of structural weaknesses in Georgia’s corporate income tax and weak laws governing how taxable corporate income is calculated, the state collects no corporate income tax revenue from the vast majority of businesses. In the 2019 tax year, out of a total of 230,838 corporate income tax returns filed, 94 percent or over 217,000 corporations reported taxable income of $0 or less to the state, while only 605 corporations reported earning annual income over $1 million.[3] Corporate income taxes are also extremely sensitive to economic declines. Between fiscal years 2020 and 2021, annual state corporate income tax collections are expected to fall from over $1.2 billion to $789 million, escalating Georgia’s imperative to ensure top-earning corporations are paying their fair share to help balance the state budget.[4]

In part because of structural weaknesses in Georgia’s corporate income tax and weak laws governing how taxable corporate income is calculated, the state collects no corporate income tax revenue from the vast majority of businesses. In the 2019 tax year, out of a total of 230,838 corporate income tax returns filed, 94 percent or over 217,000 corporations reported taxable income of $0 or less to the state, while only 605 corporations reported earning annual income over $1 million.[3] Corporate income taxes are also extremely sensitive to economic declines. Between fiscal years 2020 and 2021, annual state corporate income tax collections are expected to fall from over $1.2 billion to $789 million, escalating Georgia’s imperative to ensure top-earning corporations are paying their fair share to help balance the state budget.[4]

With Few Safeguards, Cost of Georgia Film Tax Credit Soars

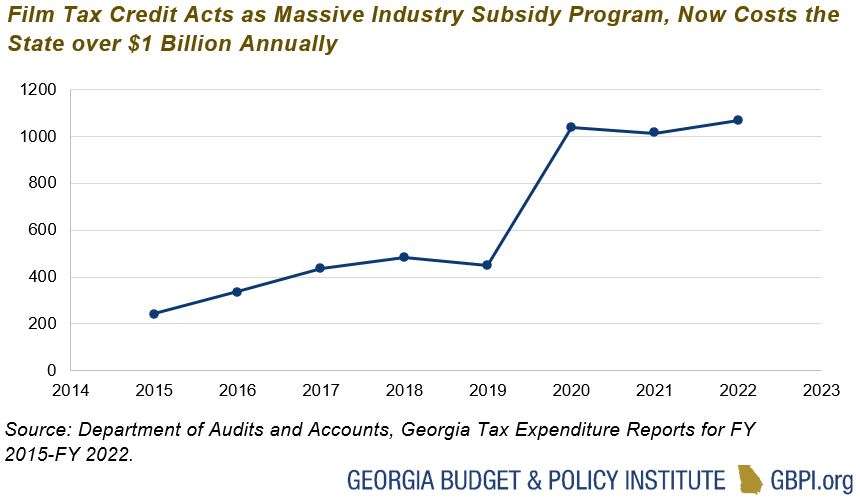

The state’s Film Tax Credit is Georgia’s largest special-interest tax credit and one of the most lucrative tax subsidy programs in the United States. The state allows corporations to receive up to a 30 percent, dollar-for-dollar tax credit for expenses from qualifying vendors to film and other entertainment industry productions completed in Georgia. Because approximately 88 percent of companies participating in the program are based outside of Georgia and owe less in taxes than they receive in credits, the generous tax subsidy allows many corporations to profit from state taxpayers.[5]

As a result of transferability and deferred-use provisions that allow the credits to be sold on the open market and used for up to five years after they are earned, the state estimates that only $389 million of over $1 billion in film tax credits issued in 2022, or 36 percent, will go to offsetting corporate income taxes. Of this share, only a small fraction will actually go to offsetting taxes by companies directly involved in earning film credits. A previous state audit suggests that film companies earning the credits use as little as 1 percent of the credits to offset their own taxes and that the vast majority are sold second-hand.[6]

Further demonstrating the flawed design of the state’s film tax credit, a recent state audit revealed that, of all the industry expenses used by corporations to claim film tax credits, non-resident labor was the largest category of expenditures, accounting for 37 percent of credits issued. This is just one obvious example of how the state is subsidizing the cost of employing out-of-state workers rather than benefitting Georgians. Currently, the film tax credit has no sunset, meaning there is no date set for the law authorizing it to expire, and there are no limits or caps on the amount of credits that can be earned.[7]

Jobs Tax Credits

Job creation is often touted as the primary reason for subsidy programs, and Georgia offers breaks exclusively for this purpose. Georgia’s first Job Tax Credit (JTC) was enacted by the General Assembly in 1989, at which time the primary purpose of the program was to increase employment in Georgia’s most distressed counties.[8] These JTCs may potentially offset up to 100 percent of a corporation’s tax liability.

The amount of JTC available to a company creating jobs in Georgia is determined by the area where the company is looking to expand or locate. Georgia counties receive a designation based on economic-related conditions annually. Higher credits are available in counties with greater economic challenges, which tend to fall in areas of the state outside of Metro Atlanta. The Georgia Department of Community Affairs issues a four-tier designation based on the following factors:

- Highest unemployment rate

- Lowest per capita income

- Highest percentage of residents whose incomes are below the poverty level

In Tier One (the most distressed) and Tier Two counties, the total credit amount may offset up to 100 percent of a company’s state income tax liability for a taxable year. In Tier Three and Tier Four counties, the total credit amount may offset up to 50 percent of a company’s liability for a taxable year.[9]

Companies are also able to qualify for other job creation credits, such as the Quality Jobs Tax Credit (QJTC), which can be applied to 100 percent of Georgia’s corporate income tax liability. The QJTC requires employers to establish a minimum number of jobs that pay at least 10 percent above the average wage in the county where the jobs are created. It is important to note that jobs that qualify for the QJTC are ineligible for the JTC, so a company cannot create jobs that take advantage of both credits simultaneously.[10]

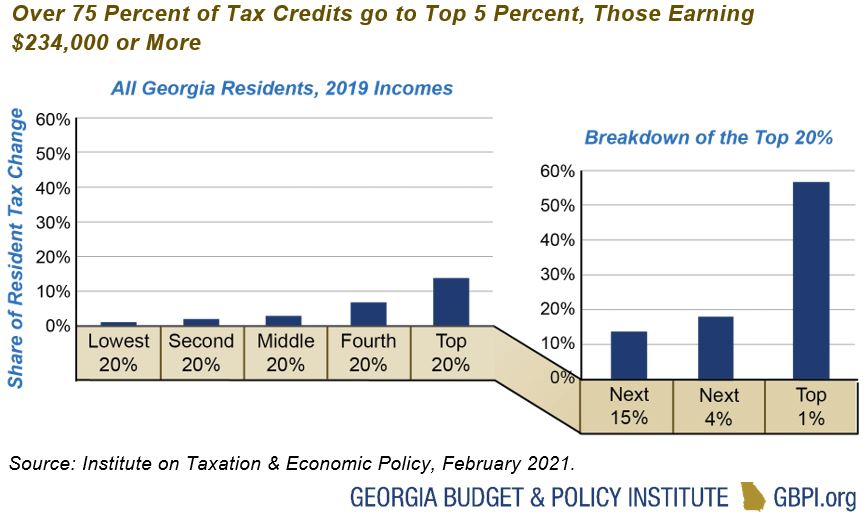

GBPI’s distributional analysis demonstrates that approximately 81 percent of $476 million in tax savings from the state’s JTC, QJTC, Employer’s Credit for Approved Retraining and Research Tax Credits go to benefit businesses and taxpayers based out-of-state. Of the 19 percent, or $92 million per year that goes to Georgia residents, 75 percent of credits benefit tax filers earning over $234,000 annually—the top 5 percent.

Because little information is publicly reported, it is difficult to make firm conclusions or conduct appropriate research on the effect that job creation tax credits have on economic mobility. For instance, due to the state’s lack of transparency when it comes to evaluating major job creation tax credit programs, it is unclear how many of the jobs created are paying a meaningful living wage. It is also unclear how many of the jobs are permanently retained in these communities.

Moreover, many of the counties that are designated as the most distressed also overlap with counties in Georgia’s more rural Black Belt region, a swath of Middle and Southwest Georgia where slavery was once concentrated and where many Black Georgians live today.[11] Consequently, transparency in Georgia’s tax subsidy programs is a racial equity imperative. Rural communities of color need assurance that corporations that are benefitting from $0 in corporate income tax liability are creating high-quality employment opportunities. Otherwise, corporations benefitting from subsidies in these areas are blocking opportunities for economic growth that could benefit both families and businesses.

Other Tax Subsidies and Credits

Several other major tax breaks are primarily used by qualifying corporations to reduce the amount of corporate income taxes owed to the state without job creation requirements. The State of Georgia allows corporations to exempt foreign-earned income from corporate taxes through its global intangible low-taxed income (GILTI) provision, which was adopted in 2018 in conformity with a federal tax package. Almost all the benefits of this $182 million provision (FY 2022) go to large, multinational corporate shareholders outside the state of Georgia. Regardless of whether or not the tax break is designed to create jobs, proponents argue that tax breaks are necessary to attract businesses and that the costs of those breaks are partially or wholly offset by the additional tax revenue derived from the increased economic activity.

Several other major tax breaks are primarily used by qualifying corporations to reduce the amount of corporate income taxes owed to the state without job creation requirements. The State of Georgia allows corporations to exempt foreign-earned income from corporate taxes through its global intangible low-taxed income (GILTI) provision, which was adopted in 2018 in conformity with a federal tax package. Almost all the benefits of this $182 million provision (FY 2022) go to large, multinational corporate shareholders outside the state of Georgia. Regardless of whether or not the tax break is designed to create jobs, proponents argue that tax breaks are necessary to attract businesses and that the costs of those breaks are partially or wholly offset by the additional tax revenue derived from the increased economic activity.

In contrast, most tax experts oppose income tax breaks for corporations. At best, corporate income tax breaks are an inefficient and often ineffective way to attract new companies, bolster job growth or encourage research and development. At their worst, business tax breaks redirect revenues that could be used to fund critical state programs in education or health care to instead boost the profits of large out-of-state corporations and well-connected special interests.[12]

While some tax breaks do not serve Georgians as well as they should, others are designed to keep the state’s tax system from unduly harming either low-income Georgians or people struggling to stay in the middle class. Groceries purchased using an EBT card (provided by the Supplemental Nutrition Assistance Program, or SNAP) are exempted from Georgia’s sales tax for that reason. Georgia seniors are not asked to pay income taxes on their Social Security benefits. Georgians with low incomes receive tax credits to help them afford the rising costs of child care and other necessities. These types of policies should certainly be monitored to ensure efficiency, but generally, they are essential tools lawmakers should maintain and, in some cases, expand.

Tax Subsidies Favor Big Business

In addition to bypassing Georgia’s more rural communities, subsidies also tend to bypass small businesses that serve as essential job creators in the state. Small businesses (those with fewer than 500 employees) are a defining feature of Georgia’s economy. According to the latest small business profile from the United States Small Business Administration (SBA), 43 percent of all Georgia workers are employed by small businesses.[13]

In a detailed national study examining more than 4,000 deals in 14 states, researchers found that large corporations were awarded 70 percent of tax break deals and 90 percent of the subsidy dollars—even from programs that are made available to small businesses. Small businesses, which are responsible for so many of Georgia’s new jobs, are being severely shortchanged.[14]

Recommendations

Establish a formal review of business tax subsidies: Unlike other state investments such as education or health care, tax subsidy programs are rarely reviewed to ensure effectiveness in Georgia. Georgia was recently ranked as “trailing behind” other states on evaluating these breaks.[15] Creating a system to regularly evaluate all tax credits and subsidies would give lawmakers a tool to determine which tax credits and exemptions are working and which are not. The state could then cut or expand them based on an informed assessment of the return on investment, as opposed to only anecdotal evidence and information generated by lobbyists and the corporations seeking tax breaks.

Tax break reports should include the following features:[16]

| Feature | Includes |

| Accessibility | Regular publication

Incorporated into the budget process Available on the Internet |

| Scope | All tax expenditures, including those with lower costs or those benefitting few taxpayers

Explicit and implicit tax expenditures Tax expenditures enacted by the state that affect local government |

| Detail | The cost of the tax expenditure, using current data

The cost in future years, to allow for comparison with other proposed expenditures A description of the tax expenditure The relevant legal citation and year of enactment Details on the taxpayers who benefit from the tax expenditure Separate reporting for the state and local revenue losses, where applicable |

| Analysis | Classification of tax expenditures using the same categories as direct spending

The stated purpose of each tax expenditure Evaluation of the extent to which that purpose has been accomplished Examination of outputs, such as jobs created, distributed to populations disaggregated by race/ethnicity and gender Analysis of the distribution of benefits by income level and size of business |

Eliminate Transferable Tax Credits: Transferable tax credits can be sold when the entity that earns them owes nothing in state taxes to any business or person that owes state income tax in Georgia. The state offers several tax credits that are transferable; however, the Film Tax Credit is by far the largest, and each year singularly accounts for $679 million (FY 2021) in revenue lost to the state through credits sold second-hand. The state should eliminate the practice of allowing the transfer of tax credits to stop corporations with no tax liability from effectively profiting off state taxpayers through indirect subsidies.

Add Sunset Dates to All Tax Credits: Along with enacting a standardized process of evaluation for tax credits, lawmakers should add a sunset date to all tax expenditures in Georgia’s tax code to ensure that tax breaks do not go unaudited or renewed indefinitely without legislative review. The vast majority of state tax credits have no sunset date. GBPI recommends adding sunset dates of no more than five years from the date of enactment for all industry-specific tax credits, as well as those designed to incentivize job creation.

Strengthen the State Corporate Income Tax by Eliminating Low-Return Credits, Subsidies and Loopholes: As more information becomes available on specific tax credits and breaks, the state should eliminate tax breaks that only serve to reduce corporate income tax collections and benefit wealthy, out-of-state special interests. GBPI’s analysis of available data, in conjunction with the Institute on Taxation and Economic Policy, demonstrates that out-of-state shareholders and those in the top five percent of income earners are the largest beneficiaries of the seven largest tax credits offered by the state, which will cost Georgians approximately $1.8 billion in lost revenue in FY 2022.

Methodology

These analyses of Georgia’s tax expenditures and the impact of reducing job tax credits were developed in partnership with the Institute on Taxation and Economic Policy (ITEP), using the approach, procedures and definitions laid out below, and considering job tax credits’ effects on 5 million unique Georgia tax filers.

Definition of Income

There are two broad ways in which a distributional analysis can sort taxpayers by income level. One approach, used by legislative fiscal analysts in most states, uses income definitions based on “Adjusted Gross Income.” In this approach, the starting point is the income that is subject to income taxes in a given state. The other approach, used by ITEP, is to use a more universal income definition, including both income that is subject to tax and income that is exempt.

For components of income that are subject to income taxes, ITEP relies on information from the Internal Revenue Service’s “Statistics of Income” publication, which provides detailed state-specific information on components of income at different income levels. For components of income that are either fully or partially tax-exempt, ITEP uses data from the Congressional Budget Office and the Current Population Survey to estimate income levels in each state. The generally non-taxable income items for which ITEP makes state-by-state estimates (which are included in our measure of “total income”) include: Social Security benefits, Worker’s Compensation benefits, unemployment compensation, VA benefits, child support, financial assistance, public assistance and supplemental security income.

It is widely understood that taxpayers at all income levels tend to underreport certain income categories, especially capital gains, pass-through business income, rental income and farm income. For this reason, ITEP’s model estimates the amount of unreported income of each type in each state. These estimates are based on data from a series of Internal Revenue Service research reports that measure the income “tax gap”—the difference between the amounts of various types of income that are reported for tax purposes each year and the (larger) amounts that are earned. The tax gap is primarily the result of underreporting by taxpayers. This unreported income is included in our “total income” estimates for each state.

This comprehensive approach to measuring income is more informative than the “Adjusted Gross Income” approach for two critical reasons. Different states can use very different income tax rules, so “Adjusted Gross Income” is a concept that can have different meaning depending on the state. Moreover, large amounts of income are excluded from Adjusted Gross Income entirely, even though these income sources represent a meaningful element in a taxpayer’s “ability to pay.” If the goal is to express the impact of a tax change in relation to a taxpayer’s ability to pay it, the only accurate way of doing so is to express these tax changes as a share of total income, rather than Adjusted Gross Income.

Corporate Tax Cuts

When estimating the impact of corporate tax changes, ITEP uses revenue estimates from the Joint Committee on Taxation (JCT) for guidance on a provision’s overall impact and then calculates the distribution of benefits or costs among taxpayers. ITEP follows JCT’s approach in assuming that in the short run, a corporate tax cut will benefit the owners of corporate stocks alone, but in the long run (usually assumed to be ten years after enactment) a quarter of the benefits will flow to workers.

ITEP differs from JCT in that ITEP has updated their approach to account for new research that finds 35 percent of American corporate stocks are owned by foreign investors, a larger fraction than were previously assumed. This means that whatever portion of benefits flows to owners of corporate stocks (100 percent in the short-run, three-fourths in the long-run), one can assume that 35 percent of that amount flows to foreign investors.

This approach to corporate tax changes is applied to provisions that entirely affect C corporations (companies that pay the corporate tax), such as the reduction in the corporate income tax rate. For provisions that affect both C corporations and pass-through businesses, this approach is applied to the portion of the provision’s tax cut or tax hike that would fall on C corporations.

End Notes

[1] Georgia Department of Audits and Accounts Performance Audit Division, “Impact of the Georgia Film Tax Credit,” January 2020, p. 23.

[2] Goodman, J. (2012). Tax breaks for sale: transferrable tax credits explained. Pew Trusts. https://www.pewtrusts.org/en/research-and-analysis/blogs/stateline/2012/12/14/tax-breaks-for-sale-transferable-tax-credits-explained

[3] Georgia Department of Revenue. Fiscal year 2019 statistical report. https://dor.georgia.gov/document/document/2019-statistical-report/download

[4] Governor’s Office of Planning and Budget. (2021, January). The governor’s budget report for AFY 2021 and FY 2022. https://opb.georgia.gov/document/governors-budget-reports/afy-2021-and-fy-2022-governors-budget-report/download

[5] Georgia Department of Audits and Accounts, Performance Audit Division. (2020, January). Impact of the Georgia Film Tax Credit: Credit’s impact on economy, jobs is less than reported. Performance Audit Report No. 18-03B, p. 28. http://open.georgia.gov/openga/report/downloadFile?rid=23536

[6] Georgia Department of Audits and Accounts, Performance Audit Division. (2020, January). Administration of the Georgia Film Tax Credit, Generous tax credit and insufficient controls incentivize misuse. Performance Audit Report [page 10]

[7] Georgia Department of Economic Development, “Incentives and Applications,” https://www.georgia.org/industries/film-entertainment/georgia-film-tv-production/production-incentives

[8] Sjoquist, D., & Wheeler, S. (2013). The structure and history of Georgia’s job tax credit program. Fiscal Research Center, Georgia State University. https://cslf.gsu.edu/files/2014/06/structure_and_history_of_georgias_job_tax_credit_program_the.pdf

[9] Georgia Department of Revenue. (2020). Tax credit summary in rules and regulations. Georgia Secretary of State. http://rules.sos.state.ga.us/gac/110-9-1?urlRedirected=yes&data=admin&lookingfor=110-9-1

[10] Ibid

[11] GBPI. (2021). 2021 Georgia budget primer. https://gbpi.org/georgiabudgetprimer/ pp. 30-31.

[12] Bartik, T. J. (2018). Who benefits from economic development incentives? How incentive effects on local incomes and the income distribution vary with different assumptions about incentive policy and the local economy. Upjohn Institute. https://research.upjohn.org/up_technicalreports/34/

[13] United States Small Business Administration. (2018). Small business profile for Georgia. (2018). https://www.sba.gov/sites/default/files/advocacy/2018-Small-Business-Profiles-GA.pdf

[14] LeRoy, G., Fryberger, C., Tarcyznska, K., Cafcas, T., Bird, E., & Mattera, P. (2015). Shortchanging small business: How big businesses dominate state economic development incentives. Good Jobs First. https://www.goodjobsfirst.org/sites/default/files/docs/pdf/shortchanging.pdf

[15] Goodman, J., & Chapman, J. (2017). How states are improving tax incentives for jobs and growth: A national assessment of evaluation practices. Pew Trusts. https://www.pewtrusts.org/en/research-and-analysis/reports/2017/05/how-states-are-improving-tax-incentives-for-jobs-and-growth

[16] Adapted from Levitis, J., Johnson, N., & Koulish, J. (2009). Promoting state budget accountability through tax expenditure reporting. Center on Budget and Policy Priorities. https://www.cbpp.org/sites/default/files/atoms/files/4-9-09sfp.pdf