Higher education is a pathway to greater financial security and prosperity. The pandemic-induced recession illustrates how Georgians without degrees are most vulnerable during economic downturns, with unemployment rates for individuals with a high school education only—37 percent of adult Georgians—consistently double that of those with a college degree.[1],[2] Many jobs lost during recessions do not return, and almost all new jobs created during economic recoveries require some level of postsecondary education.[3]

But students seeking a bachelor’s or associate degree or other postsecondary credentials often face financial roadblocks, including high costs that lead them into student debt. Growing student debt indicates the shift of risk and responsibility for paying for higher education to individuals from the public, yet the burden of excessive student debt spreads from individuals out to the economy.

Seeing higher education as a private investment rather than a shared responsibility intensifies financial risk in an economy where postsecondary education is increasingly critical to achieving economic security. Debt burden varies widely by race, ethnicity and family wealth, and borrowers experience different challenges repaying debt based on their loan amounts and jobs they can get. Concerningly, borrowing rates and loan amounts are very high among Black students, whose college enrollment has grown quickly while state funding for colleges has declined and tuition increased. Debt is too risky for some low-income students who choose not to borrow and face difficult tradeoffs that can hurt their chances of going to college, getting a degree and achieving financial security. Student loans allow for-profit colleges, which disproportionately enroll Black women, to charge high prices for credentials that often fail to provide an adequate return in the workforce. Those hardest hit are the students who borrow and do not graduate, and graduation rates are lower for students from low-income families and Black students who face multiple and cumulative financial, institutional and academic barriers to success.

State leaders can create stronger communities and a more prosperous state by funding colleges and universities adequately so they can provide a high-quality education while keeping student costs low. Schools can work harder to support students and remove roadblocks to graduation. Federal and state governments, schools, businesses and students themselves all have a part to play. Postsecondary education should be a shared responsibility, with shared gains for families, communities and the state.

Excessive Student Debt Hurts Economy and Individual Financial Security

Student loans enable many Georgians to go to college, but the consequences of excessive debt can also hurt students’ financial security and slow overall economic growth. For example, student debt is linked to lower homeownership rates among young adults, and housing is a vital sector of the economy and personal wealth.[4] Debt is also linked to declines in small business formation, the engine of economic growth, as small businesses rely most on personal financing.[5]

Many student borrowers struggle to pay back their loans, and loan default can worsen existing cycles of financial insecurity. Nationally, 27 percent of borrowers will default on a federal student loan within 12 years of starting college.[6] Borrowers in repayment can experience wage garnishment, withholding from income tax refunds and ineligibility for state and federal programs like HOPE or the recent Paycheck Protection Program. Federal and state debt relief options like Public Service Loan Forgiveness have systemic problems that mean few borrowers receive the relief they expect.[7] Poor credit scores from loan default can also make it difficult to get approval for apartment rentals or cause higher interest rates for other forms of consumer debt. Student loans cannot be discharged through normal bankruptcy proceedings, so the vast majority of people filing for bankruptcy do not seek debt relief (though a portion of the less than 1 percent of people who go through special proceedings achieved some relief).[8]

Students’ College Cost Burden Increases as Public Investment Declines

Students borrow to pay for college when the price of college attendance outstrips available financial resources. Most college students who graduate finish their degrees with debt: 57 percent of Georgia college graduates carry debt, and of those who do, the average debt burden is $28,824.[9]

In contrast to public K-12 education, individuals and families bear a significant share of the costs of public postsecondary education. Since college students are older, many do not receive financial or material support from parents or family. This means college attendance is a unique period when students are expected to pay for education and support themselves at the same time, before they have the credentials and earnings required to do so.

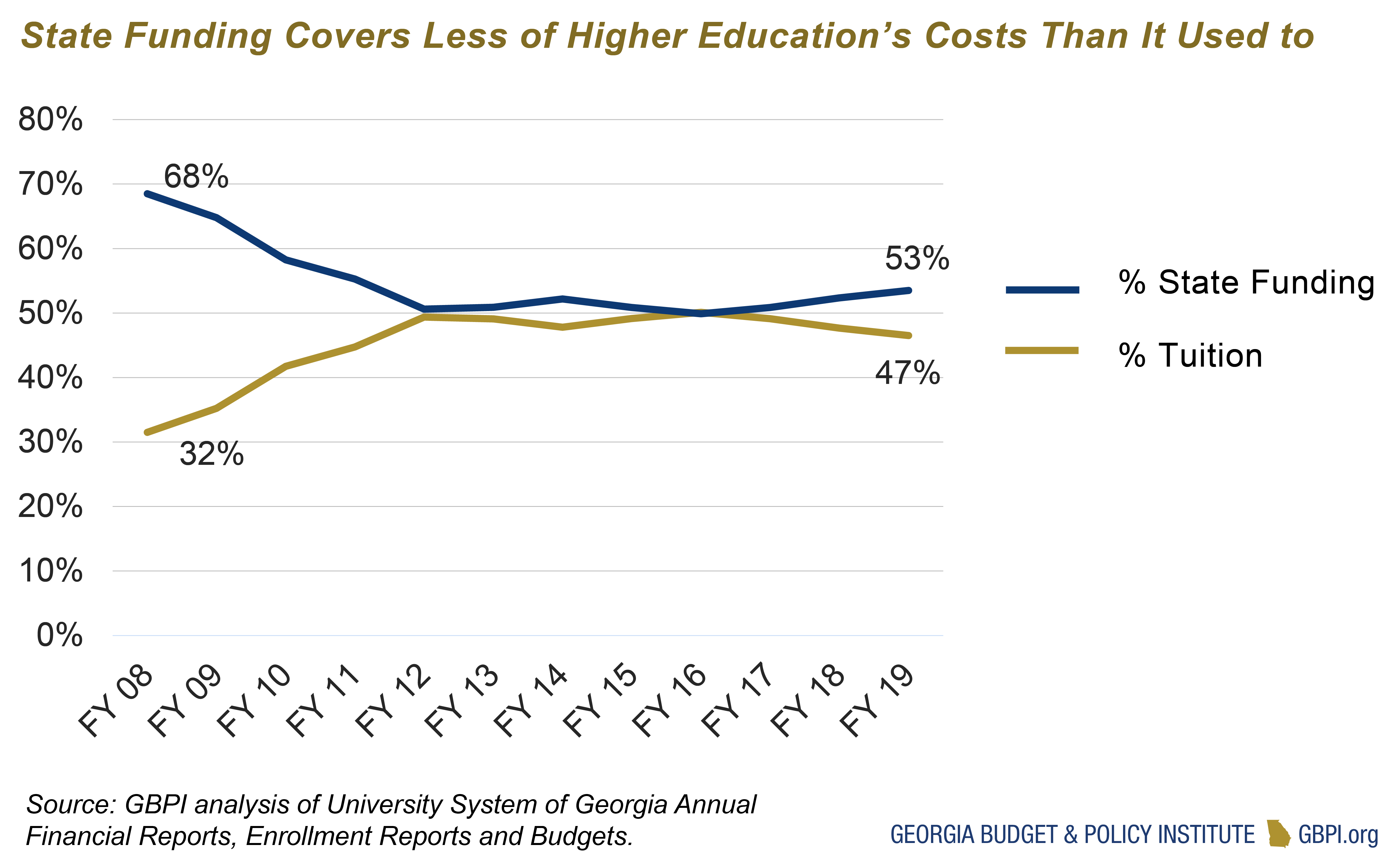

The cost of higher education is a shared responsibility among the state and federal government and families. But both the state and federal share of higher education costs have declined over time, while the cost burden on individuals and families increases.

When the state developed the current funding formula for higher education in the 1980s, three-quarters of the cost was funded by the state and one-quarter came from tuition. Over time, state funding decreased, and the student contribution doubled to today’s even split.[10]

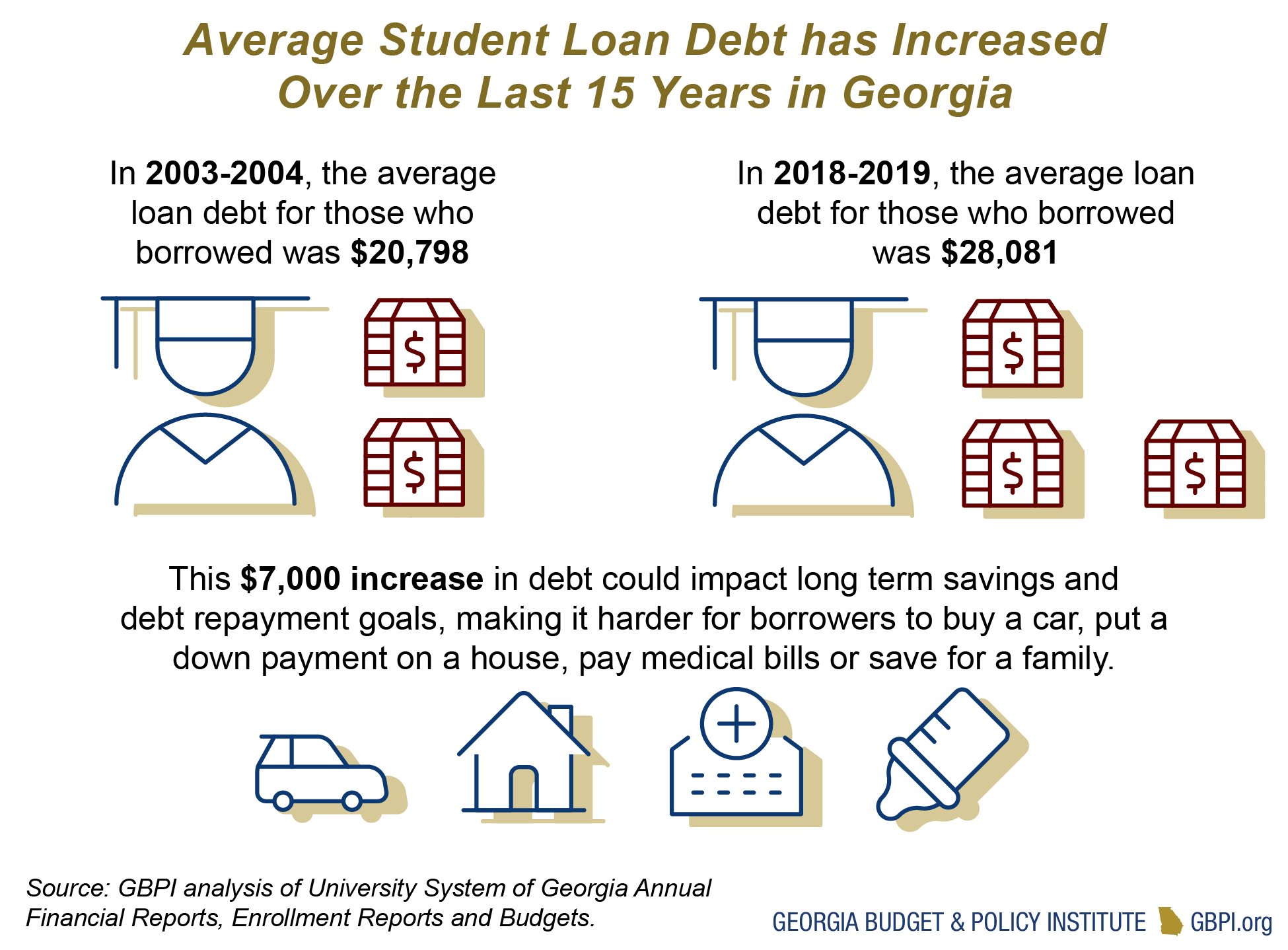

Federal Pell Grants also declined in the share of higher education costs they cover. As recently as 2001-2002, the maximum Pell grant covered an average of 42 percent of the cost of attendance. In 2019-20, the maximum Pell Grant of $6,095 now covers 28 percent of the average cost of attendance at public four-year colleges and 12 percent at non-profit private colleges.[11] Wages for jobs students can get are low compared to housing and other costs. In 2001, a student could work a full-time, minimum-wage summer job and earn enough to pay for two semesters of tuition and fees at Kennesaw State University—assuming all earnings were going to pay for college. Today, the same earnings would cover one semester of tuition only.[12] It therefore comes as no surprise that average student loan debt for those who borrow has increased by about $7,000 over the past 15 years in Georgia.[13]

![]()

Family Income and Wealth Disparities Affect Borrowing

With both federal and state support declining, individuals and families must rely on their own income and savings to pay for college. Both are distributed unequally in Georgia today. Median family income varies widely in the 22 colleges and universities in the University System of Georgia, from under $18,000 to over $120,000.[14] (Data unavailable for technical colleges or private colleges and universities.) Many students struggle to make basic ends meet, let alone pay for college.

Undocumented Students Ineligible for Federal Loans and Aid

Undocumented students are ineligible for federal financial aid, including federal loans, state student loans and state aid like HOPE. They are also ineligible for in-state tuition. These students must rely on private scholarships and loans and pay out of pocket for higher in-state tuition. In Georgia, about 14,000 undocumented students ages 18-24 are enrolled in school, and 30,000 are not enrolled, according to estimates from the Migration Policy Institute. Without access to loans, grants and in-state tuition, college is too expensive for many undocumented students.

Wealth disparities are also wide. In Georgia, white households’ average net worth is six times higher ($123,830) than Black households ($20,630).[15] The racial wealth gap both contributes to and is exacerbated by student debt. Policies and practices that excluded African-Americans from wealth-building, like redlining, discriminatory lending and housing discrimination, prevented Black households from building wealth and stripped existing wealth from them.[16] With fewer family resources to pay for college, Black students are more likely to turn to loans to finance higher education, and they borrow more on average.[17] Student debt subtracts from Black wealth in young adulthood, continuing a cycle of lower wealth and assets among Black households. Ironically, the pathway to opportunity that higher education represents for so many can contribute to financial insecurity and wealth disparities between white and Black Georgians, when paired with excessive student debt.[18],[19] In addition to discrimination, many Black Georgians experience so-called “predatory inclusion,” where higher education is accessible only on risky or exploitative terms that might limit its benefits.[20]

Many Students Who Choose Not to Borrow Still Cannot Afford College

It is important to note that some students with financial need will choose not to borrow. Though these students might avoid debt, the tradeoffs they make can decrease their chances to enroll in, excel in and finish college. Strategies students use to avoid debt include attending lower-priced (and lower-resourced) two-year colleges, delaying or pausing school enrollment to work and save money, enrolling part-time and working part or full-time.

Asian and Latinx students, immigrant families and independent students without parental financial support are less likely to borrow, even when they have significant financial need. Factors related to non-borrowing include the complexity of applying for federal loans, differing cultural perceptions or prohibitions on holding debt and negative experiences or inexperience with financial services, institutions, credit and debt.[21]

Student Debt More Likely For Black Students and Women

Georgia’s college students have become increasingly racially and ethnically diverse. In the university system, Black, Latinx and Asian students enroll in college in greater numbers every year, far outpacing population growth, while white student enrollment has declined. In the last 20 years, Black student enrollment was double that of Black population growth and Latinx student enrollment more than four times overall growth.[22]

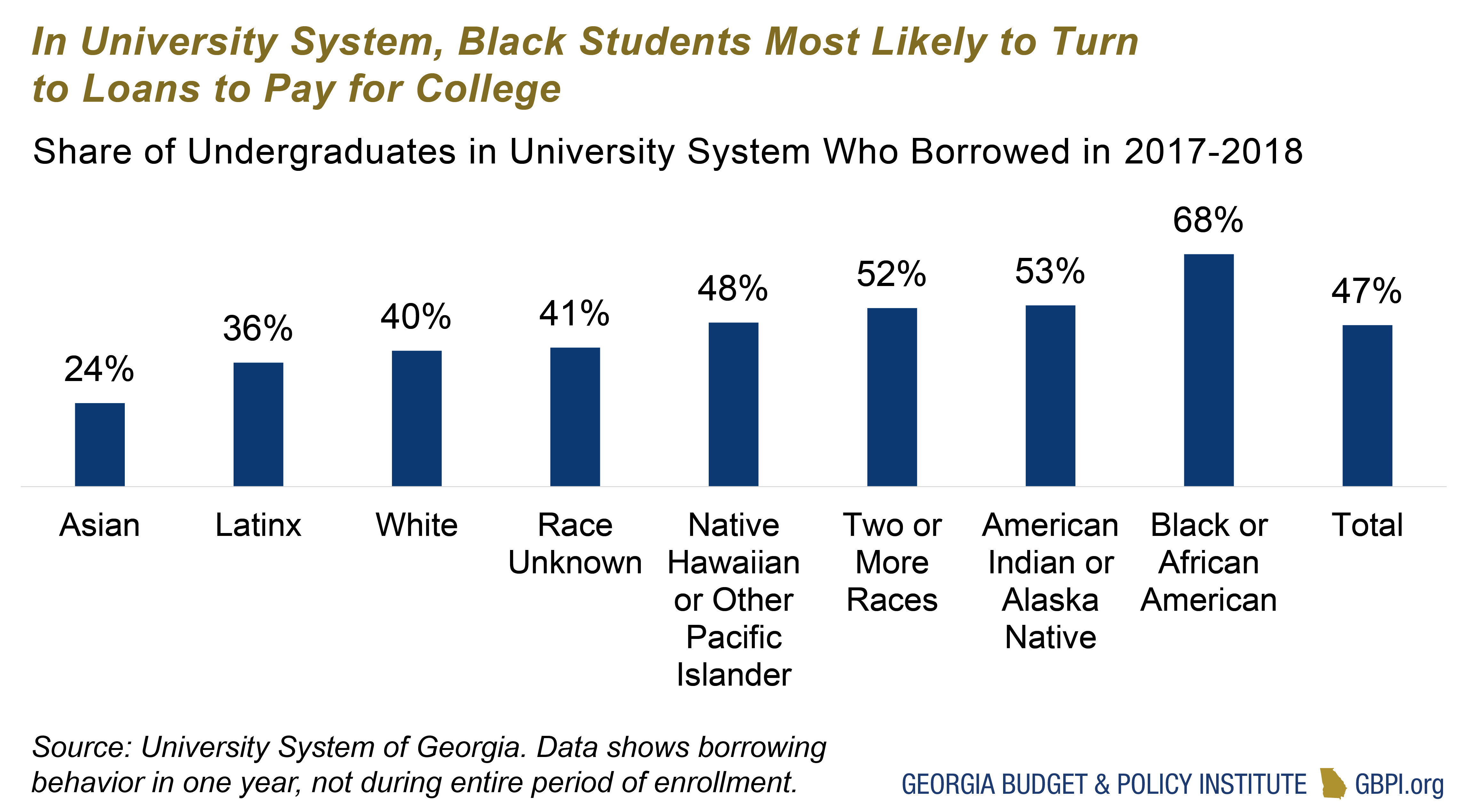

Overall, 57 percent of college graduates carry student debt in Georgia.[23] Most student loans are provided by the federal government, with a small share coming from the state, colleges themselves and private lenders. Each year about half of undergraduate students in the university system will take out student loans to finance the cost of their education. Borrowing rates are lowest among Asian students and highest among Black or African-American students.[24]

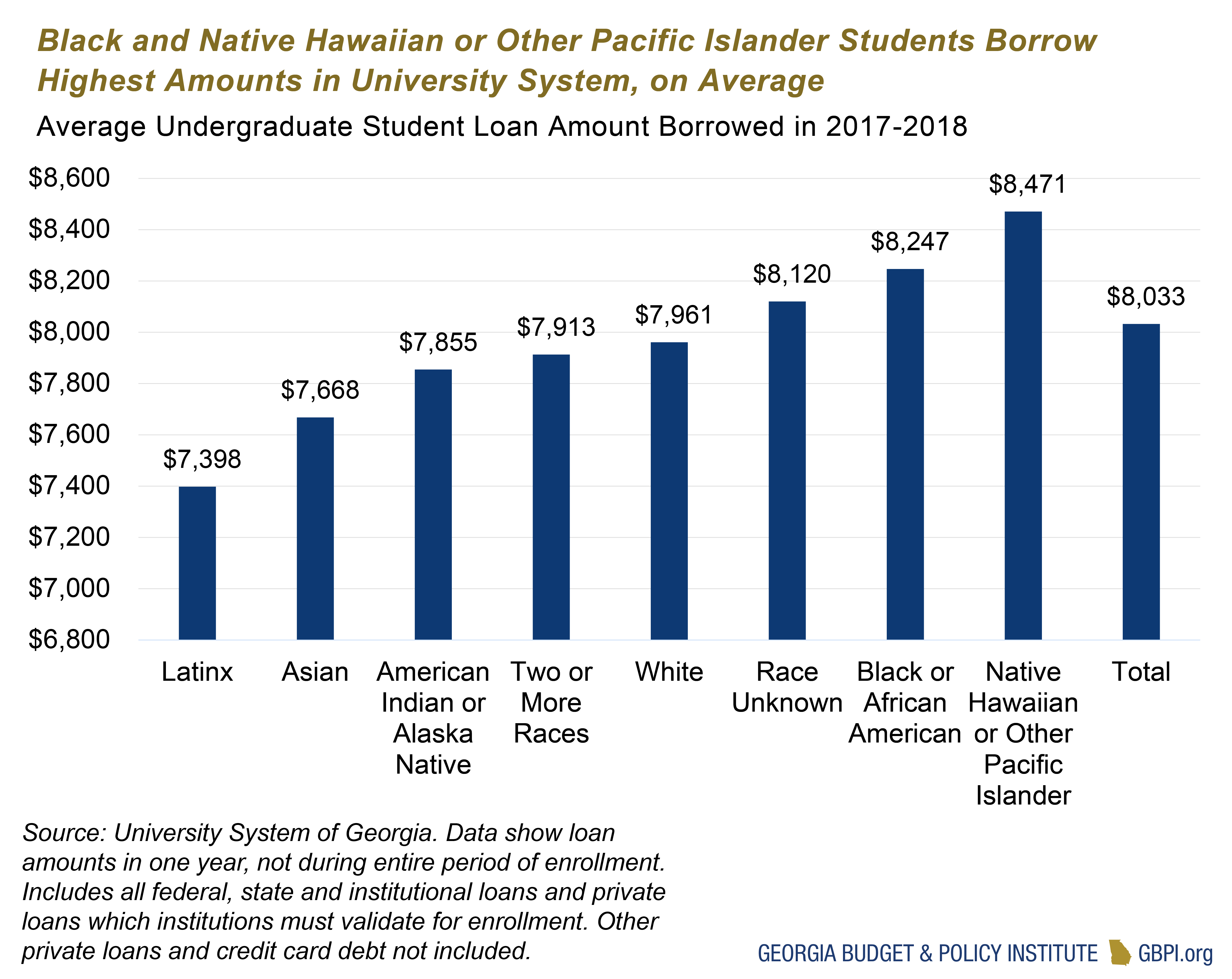

Among students who borrow, average amounts vary by about $1,000 per year. Latinx and Asian students borrow the least on average (about $7,500) and Black and Native Hawaiian or Other Pacific Islander students borrow the most (about $8,500).[25] Most loan providers, including the federal government, the largest provider of student loans, limit borrowing to certain amounts.

Lower Incomes for Women Mean Higher Student Debt Burdens

Women are the majority of college students in Georgia, making up 59 percent of enrollment in public colleges, 63 percent of non-profit private colleges and 72 percent of for-profit colleges.[26] In the university system, women are more likely to borrow than men (52 percent vs 46 percent), though they borrow slightly smaller amounts.[27]

Though they are more likely to graduate, women can expect to enter an economy where they are paid less on average. That means they may spend more time paying back student debt, or loan payments may represent a heavier financial burden. Median earnings for Georgia women with some college or an associate degree is similar to median earnings for men with less than a high school diploma ($30,197 versus $29,218). And median earnings for women with graduate degrees are still less than median earnings for men with bachelor’s degrees ($61,467 vs. $67,400).[28]

For Black and Latinx women in Georgia, the gender earnings gap is even larger. White women with bachelor’s degrees have a median income of $45,000, compared to $42,000 for Black women, $40,000 for Asian women and $35,000 for Latinx women with the same education level.[29]

In the university system, the average first-semester loan taken out by women represents about 9 percent of median income for female bachelor’s degree holders in Georgia. For male graduates, the average loan amount is about 6 percent of median income.

The combination of higher enrollments, greater likelihood of borrowing, lower incomes and slower repayments leads to estimates that women hold nearly two-thirds of the more than $1.3 trillion of student debt in the U.S.[30]

Keke Harley worked her way up a large restaurant chain after high school, raising her daughter and eventually managing hundreds of employees. But during the Great Recession, she had to lay off many employees. Even with her experience, she knew that if she lost her job, she would be vulnerable in the job market without a college degree. Seeking more stability, Harley enrolled in Savannah State University after having been out of college for 16 years. She took classes full-time and worked 25 to 40 hours a week. Harley received the Zell Miller Scholarship and Pell Grant, but still needed help paying for living expenses, so she took out federal loans. Without loans, she says she would have gone part-time and would probably still be in school today.

After graduating with a bachelor’s degree in accounting, Harley got a job but faced roadblocks moving up into positions that matched her skills and experience. She said, “I’m going to have to have more education as an African-American woman to get in the door.” She decided to return to school for a Master’s in Business Administration and a Master’s in Public Administration. Today, Harley works as an accountant for a local non-profit hospital in Savannah. With her bachelor’s and two master’s degrees, she has accumulated $70,000 in student debt.

Race, Income and College Price Influence Borrowing Patterns

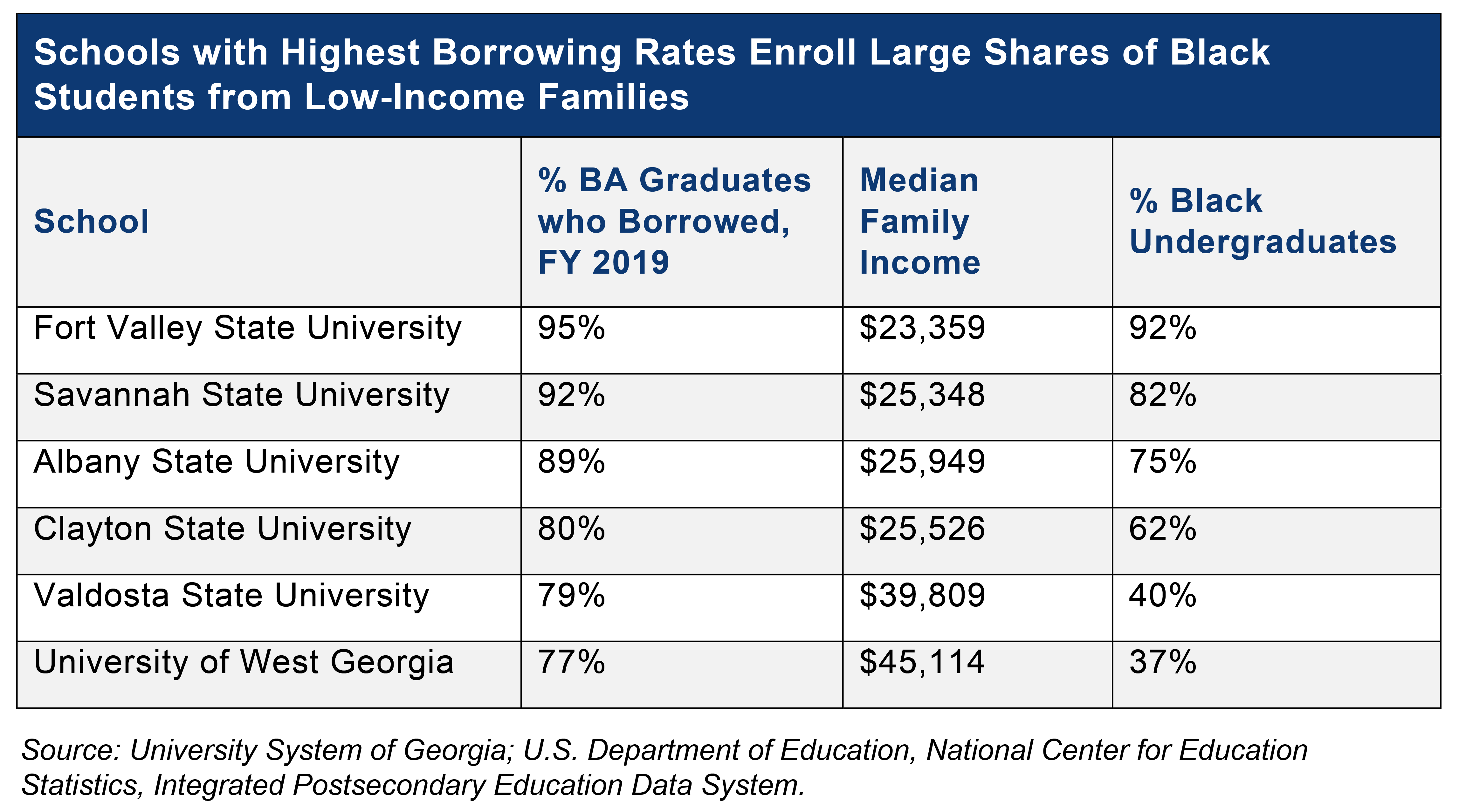

Race and differences in income and wealth affect differences in borrowing rates across the university system. Though about half of students overall will borrow in a given year, in some schools, almost all students will borrow to finance their education. [31] Consistent with demographic patterns that the students likeliest to turn to loans to pay for college are Black students, the three schools with the highest borrowing rates in the university system are Historically Black Colleges and Universities. Other schools with high borrowing rates have larger shares of Black students than the university system as a whole (28 percent). (Note: Due to data limitations, the following section focuses on borrowing behavior within the university system only.)

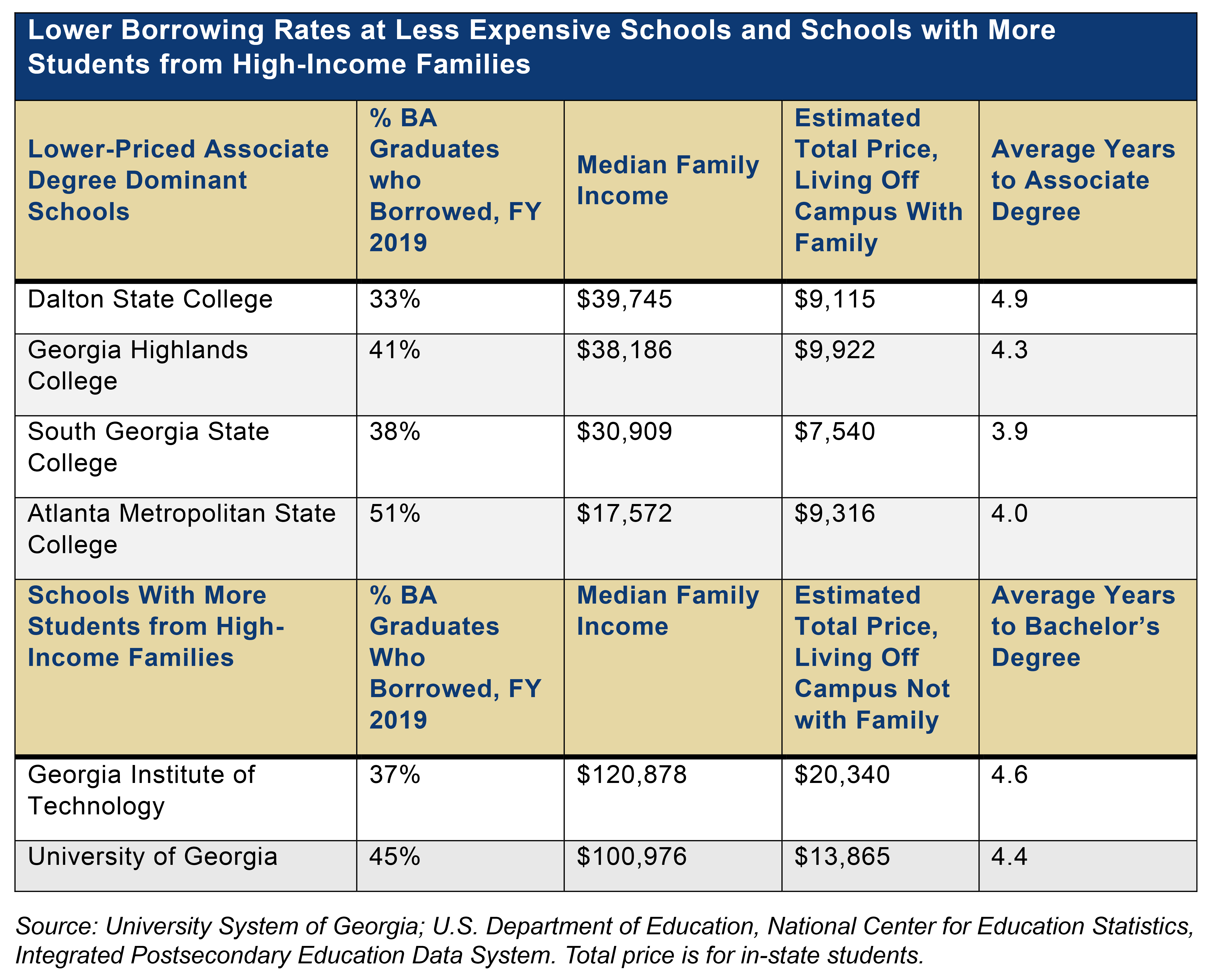

Schools with the lowest borrowing rates fall into two categories: lower-priced, associate-degree-dominant colleges and selective schools that enroll a larger share of students from high-income families. Two of the schools with the lowest borrowing rates serve significant percentages of Hispanic/Latinx students who tend to be less likely to borrow, even with financial need. Latinx students represent 31 percent of Dalton State College enrollment and 16 percent of Georgia Highlands College compared to 10 percent of total university system enrollment.[32] Schools with lower borrowing rates also tend to have more students who attend part-time to save money, and therefore take longer to graduate.

Schools with above-average loan amounts include the Georgia Institute of Technology and colleges that serve predominantly Black and low-income students. Georgia Tech enrolls a large number of out-of-state students, who have a higher cost of attendance and higher loan amounts. However, the same loan can pose very different risks, depending on family income, wealth and a labor market with uneven barriers and opportunities based on race, gender and school. For example, the average cumulative loan amount at both Georgia Tech and Clayton State University is about $29,000. This represents about a quarter of the typical family’s annual income at Georgia Tech and more than the typical family’s annual income at Clayton State.

Lower-priced state colleges have the lowest average loan amounts. State colleges offer associate degrees and bachelor’s degrees in select disciplines. Forty percent of students in state colleges attend part-time, and 22 percent are from rural counties.[33],[34]

Know More. Borrow Less.

The University System of Georgia launched its “Know More. Borrow Less” campaign in 2019 to provide students clearer information about borrowing. Components include so-called “debt notifications,” which give the amount a student owes, the expected monthly payments and projections of future costs should they borrow more; a standardized financial aid award letter that provides a recommended loan amount instead of a maximum loan amount and chatbots to respond to student and parent questions. For more, see usg.edu/know_more_borrow_less.

For-Profit College Students at Much Higher Risk of Loan Default

One of excessive student loan debt’s worst outcomes is loan default. Default can hurt credit scores, eligibility for scholarships and other programs and make it harder to achieve financial security. Nationally, 27 percent of borrowers will default on a federal student loan within 12 years of starting college. Among students entering college in 2014, 20 percent of Latinx students and 37.5 percent of Black students defaulted within the next 12 years, compared to 12 percent of white students.[35]

Black students are more likely to enroll in for-profit colleges, which are much more expensive than public colleges and universities, especially for certain occupational certificates and two-year degrees.[36] Seventy-two percent of students enrolled in for-profit colleges in Georgia are women, and 44 percent are Black women.[37]

Loan default rates among students who start at for-profit colleges are almost four times higher than for students starting at private non-profit and public colleges. Nationally, default rates are similar for students who begin school at public and non-profit private colleges (12 to 13 percent within 12 years). Though overall only 5 percent of students who complete a bachelor’s degree default on their student loans, 26 percent of graduates who attended a for-profit defaulted on a student loan. Forty-four percent of certificate-holders who attended a for-profit college defaulted on their loans.[38]

Loan default rates among students who start at for-profit colleges is almost four times higher than for students starting at private non-profit and public colleges.

College Graduation and Fair Labor Market Key to Successful Repayment

Graduation plays a significant role in the ability to repay student loans. Only 5 percent of students who complete a bachelor’s degree default on their student loans, compared to 24 percent of students who did not finish a degree and are no longer in school. Default rates are even higher for those who attended for-profit colleges but did not complete; most of these students will default. In fact, the borrowers most likely to default on student loans are those with the smallest debts, as students who drop out tend to have smaller total loan amounts. Thirty-five percent of student loan defaults are for amounts smaller than $5,000, and 66 percent of all defaults are for amounts less than $10,000.[39]

Still, graduation rates differ by race and ethnicity. Black students enroll in college in high numbers, but about half of first-time, full-time freshmen in the university system will graduate with a bachelor’s degree within six years, compared to 67 percent of white students.[40] Though Black students do not all experience college the same way, many face a combination of challenges that create barriers to graduation. Black students are more likely than students of other races and ethnicities to attend colleges with fewer resources and experience financial roadblocks.[41] A lack of encouraging and welcoming interactions with faculty, staff and other students can also affect a sense of belonging and commitment critical to persistence and graduation.

Five percent of students who complete their bachelor’s will default on their loans. But only 62 percent of students in the university system will graduate within six years.

Graduation rates differ by income as well. More than 70 percent of students with family income higher than $75,000 will graduate within six years, compared to 46 percent of students from families with income less than $35,000.[42] In technical colleges, which tend to enroll a larger share of financially independent students and more students from low-income families, only 1 in 3 students who start a technical certificate, diploma or degree will finish a credential within 150 percent of the normal time for completion (e.g., within three years for an associate degree).

The labor market that graduates enter also matters for successful loan repayment. Bachelor’s degree holders default at a low rate, but Black college graduates are more than five times as likely to default on student loans than white graduates (21 percent and 4 percent, respectively). In fact, Black graduates are more likely to default than white college dropouts. Part of the reason is Black students are more likely to enroll in for-profit colleges, which tend to be much more expensive than public colleges. Black students make up 60 percent of for-profit college students in Georgia, where average net price is $23,121 for four-year colleges and $19,701 for two-year colleges, compared to $11,500 for public four-year colleges and $3,710 for public two-year colleges.[43] Students who attend for-profit colleges are also less likely to be able to get a job and have lower earnings compared to their peers who attended non-profit and public colleges.[44] Higher cost and debt, and lower employment rates and earnings mean bachelor’s degree holders who attended for-profit colleges at any point default at more than six times the rate of students who never attended a for-profit college.[45],[46] National data show debt divides grow even larger after graduation, as some students pursue graduate school or face racial discrimination in the job market.[47]

Conclusion

Student loan debt enables many students to go to college, but the consequences of excessive debt can also hurt students’ financial security and contribute to social and economic inequalities.

Excessive debt and loan default can set people back—a cruel irony given that higher education’s promise for so many is financial security for their families and the building of intergenerational wealth. The growing cost and necessity of higher education mean more low-wealth Black families are borrowing to attend college. But they are also less likely to complete college and more likely to default, hindering their ability to build wealth and pass it on to their children. In contrast, higher-wealth families have a financial cushion for hard times, access to well-funded school systems and access to capital for larger investments like education or housing.

Financing higher education with debt has become increasingly common as public state and federal resources fail to keep up with student enrollment and employer demand for college graduates. Current federal policy conversations to reduce debt include increasing need-based Pell Grants, raising awareness of repayment options, simplifying income-driven repayment and canceling portions of student debt.

State financial aid policy can also reduce the need for students to borrow. This means increasing funding for need-based state grants and scholarships, and funding colleges and universities adequately to shift the higher education cost burden away from individual students.

Colleges and universities can also ensure policies and practices are in place, so campuses are designed to support students through their education to graduation. That means prioritizing services like academic advising and mental health support, reducing administrative barriers, creating welcoming and inclusive environments and providing students with accurate information and guidance when making borrowing decisions.

Businesses who want more employees with postsecondary credentials to fill positions can do their part by offering paid internships for college students, contributing to need-based scholarships, ensuring diverse hiring pools and fair hiring practices and supporting policies for college affordability at the state and federal levels.

During and after this recession and recovery, postsecondary education will be more important than ever for individuals and the state’s prosperity. Before the pandemic, it was predicted that more jobs in Georgia would require some form of college education than Georgians with those credentials.[48] Evidence suggests the recession will lead to permanent job loss for some positions that do not require a college credential.[49] Policymakers must share in managing the risk of debt-financed education so that it does not harm individuals, slow the economy and worsen social and economic inequalities.

Endnotes

[1] GBPI analysis Bureau of Labor Statistics Current Population Survey data on unemployment rate by educational attainment.

[2] U.S. Census Bureau, 2019 American Community Survey 1-Year Estimates Table S1501. 33 percent of adults 25 and over have a bachelor’s degree or higher; an additional 8 percent have an associate degree.

[3] Carnevale, A., Jayasundera, T., & Gulish, A. (2016). America’s divided recovery: College haves and have-nots. Georgetown University Center on Education and the Workforce. https://cew.georgetown.edu/cew-reports/americas-divided-recovery/ See new evidence in Ding, L., & Saenz Molina, J. (2020). “Forced automation” by COVID-19? Early trends from Current Population Survey data. Federal Reserve Bank of Philadelphia. https://www.philadelphiafed.org/-/media/community-development/publications/discussion-papers/discussion-paper_automation.pdf

[4] Mezza, A., Ringo, D., & Sommer, K. (2019 Feb). Can student loan debt explain low homeownership rates for young adults? Consumer & Community Context. Federal Reserve Board Division of Research and Statistics. https://www.federalreserve.gov/publications/2019-january-consumer-community-context.htm

[5] Ambrose, B.W., Cordell, L., & Ma, Shuwei. (2015 July). The impact of student loan debt on small business formation. Federal Reserve Bank of Philadelphia.

[6] Scott-Clayton, J. (2018 Jan). The looming student loan default crisis is worse than we thought. Economic Studies at Brookings. https://www.brookings.edu/research/the-looming-student-loan-default-crisis-is-worse-than-we-thought/

[7] Green, E.L. & Cowley, S. (2019, Nov 28). Broken promises and debt pile up as loan forgiveness goes astray. The New York Times. https://www.nytimes.com/2019/11/28/us/politics/student-loan-forgiveness.html

[8] Iuliano, J. (2011 July 24). An empirical assessment of student loan discharges and the undue hardship standard. 86 American Bankruptcy Law Journal 495. https://ssrn.com/abstract=1894445

[9] The Institute for College Access and Success. Student debt and the class of 2018. https://ticas.org/interactive-map/

[10] GBPI analysis of data from University System of Georgia annual financial reports, enrollment reports and amended fiscal year budgets.

[11] Data from College Board. (2019). Trends in student aid 2019. https://research.collegeboard.org/pdf/trends-student-aid-2019-full-report.pdf

[12] In 2001, working 480 hours at the federal minimum wage of $5.15 per hour resulted in $2,472. Assuming all earnings go to college tuition, this could cover two semesters of tuition and fees at Kennesaw State University, which was $2,428. In 2019, working 480 hours at the federal minimum wage of $7.25 per hour results in $3,480. Tuition for one semester at Kennesaw is $2,781, plus fees totaling $1,003.

[13] The Institute for College Access and Success. Student debt and the class of 2018. https://ticas.org/interactive-map/

[14] University System of Georgia data.

[15] Prosperity Now Scorecard. https://scorecard.prosperitynow.org/data-by-location#state/ga

[16] Rothstein, R. (2018). The color of law: A forgotten history of how our government segregated America. Liveright Publishing Corporation. For a case study, see Rothstein, R. (2014, Oct 15). The making of Ferguson. Economic Policy Institute. https://www.epi.org/publication/making-ferguson

[17] University System of Georgia data.

[18] Houle, J.N., & Addo, F. (2018). Racial disparities in student loan debt and the reproduction of the fragile black middle class. CDE Working Paper No. 2018-2. Center for Demography and Ecology, University of Wisconsin Madison. https://cde.wisc.edu/wp-content/uploads/sites/839/2018/12/cde-working-paper-2018-02.pdf

[20] Seamster, L., & Charron-Chenier, R. (2017). Predatory inclusion and education debt: Rethinking the racial wealth gap. Social Currents 4(3), 199-207. https://www.researchgate.net/publication/315114639_Predatory_Inclusion_and_Education_Debt_Rethinking_the_Racial_Wealth_Gap

[21] Cunningham, A.F., & Santiago, D.A. (2008). Student aversion to borrowing: Who borrow and who doesn’t. Institute for Higher Education Policy and Excelencia in Education. http://www.ihep.org/sites/default/files/uploads/docs/pubs/studentaversiontoborrowing.pdf. See also Boatman, A., Evans, B., & Soliz, A. (2016). Understanding Loan Aversion in Education: Evidence from High School Seniors, Community College Students, and Adults (CEPA Working Paper No.16-15). Retrieved from Stanford Center for Education Policy Analysis: http://cepa.stanford.edu/wp16-15

[22] GBPI analysis of University System of Georgia enrollment data, 1998-2018 and Census population data, 2000-2018.

[23] The Institute for College Access and Success. Student debt and the class of 2018. https://ticas.org/interactive-map/

[24] University System of Georgia data.

[25] University System of Georgia data.

[26] GBPI analysis of U.S. Department of Education, National Center for Education Statistics, Integrated Postsecondary Education Data System (IPEDS), 2019.

[27] Jones, T. R. (June 2020). Post-secondary financial aid foundational report: 2013-14 to 2018-19. Georgia Policy Labs, Child & Family Policy Lab. https://gpl.gsu.edu/publications/post-secondary-financial-aid/

[28] U.S. Census Bureau, 2019 American Community Survey 1-Year Estimates, Table B20004.

[29] GBPI analysis of 2017 IPUMS USA data, University of Minnesota, www.ipums.org

[30] American Association of University Women. (2017). Deeper in debt: Women and student loans. https://www.aauw.org/app/uploads/2020/03/DeeperinDebt-nsa.pdf

[31] University System of Georgia data.

[32] Board of Regents, University System of Georgia, Semester Enrollment Report, Fall 2019. https://www.usg.edu/research/assets/research/documents/enrollment_reports/SER_Fall_19_Final.pdf

[33] University System of Georgia Fall 2018 enrollment report, https://www.usg.edu/research/enrollment_reports/

[34] GBPI analysis of University System of Georgia data, Resident Enrollment by Institution and County of Origin. https://www.usg.edu/research/enrollment_reports/. GBPI uses the U.S. Census Bureau’s definition of “rural” to classify counties.

[35] Scott-Clayton, J. (2018 Jan). The looming student loan default crisis is worse than we thought. Brookings. https://www.brookings.edu/research/the-looming-student-loan-default-crisis-is-worse-than-we-thought/

[36] GBPI analysis of IPEDS data. Average institutional net price of a public technical colleges if $3,710 compared to about $20,000 for two-year for-profit and non-profit private colleges. Average institutional net price for for-profit private colleges offering four-year degrees or above is more than $23,000 compared to $11,500 for public colleges and $22,000 for non-profit private colleges.

[37] GBPI analysis of U.S. Department of Education, National Center for Education Statistics, Integrated Postsecondary Education Data System (IPEDS), 2019.

[38] Scott-Clayton, J. (2018 Jan). The looming student loan default crisis is worse than we thought. Economic Studies at Brookings. https://www.brookings.edu/research/the-looming-student-loan-default-crisis-is-worse-than-we-thought/

[39] Wedderburn, R., & Biddle Andres, K. (2020). Majoring in debt: Why student loan debt is growing the racial wealth gap. Asset Funders Network. https://assetfunders.org/wp-content/uploads/AFN-Majoring-in-Debt-10.12.20.pdf

[40] University System of Georgia data

[41] GBPI analysis of University System of Georgia enrollment data. Two-thirds of Black students in the university system attend a comprehensive university, state university or state college.

[42] University System of Georgia. Graduation rates for students with unknown income is 84 percent.

[43] GBPI analysis of U.S. Department of Education, National Center for Education Statistics, Integrated Postsecondary Education Data System (IPEDS), 2019.

[44] Armona, L., Chakrabarti, R. & Loveheim, M.F. (2018). How does for-profit college attendance affect student loans, defaults and labor market outcomes? National Bureau of Economic Research Working Paper 25042. https://www.nber.org/system/files/working_papers/w25042/w25042.pdf See also Cellini, S.R. (2018). Gainfully employed? New evidence on the earnings, employment, and debt of for-profit certificate students. The Brown Center Chalkboard. https://www.brookings.edu/blog/brown-center-chalkboard/2018/02/09/gainfully-employed-new-evidence-on-the-earnings-employment-and-debt-of-for-profit-certificate-students

[45] GBPI analysis of U.S. Department of Education, National Center for Education Statistics, Integrated Postsecondary Education Data System (IPEDS), 2019.

[46] Scott-Clayton, J. (2018 Jan). The looming student loan default crisis is worse than we thought. Economic Studies at Brookings. https://www.brookings.edu/research/the-looming-student-loan-default-crisis-is-worse-than-we-thought/

[47] Scott-Clayton, J., & Li, J. (2016 Oct). Black-white disparity in student loan debt more than triples after graduation. Economic Studies at Brookings. https://www.brookings.edu/wp-content/uploads/2016/10/es_20161020_scott-clayton_evidence_speaks.pdf

[48] Carnevale, A.P., Smith, N. & Strohl, J. (2013). Recovery: Projections of jobs and education requirements through 2020. Georgetown Center on Education and the Workforce.

[49] Ding, L. & Saenz Molina, J. (2020). ”Forced automation” by COVID-19? Early trends from Current Population Survey data. Federal Reserve Bank of Philadelphia. https://www.philadelphiafed.org/community-development/workforce-and-economic-development/forced-automation-by-covid-19