Analysis of potential revision to House Bill 329 (LC 43 0601S)

Georgia lawmakers are considering a large income tax proposal with three sound tax policy reforms alongside one serious shortcoming. On the plus side, the current bill proposes to boost families with a new Georgia Earned Income Tax Credit (EITC), close an outdated loophole and index several broadly available exemptions to ensure they keep pace with economic growth. The downside is it replaces Georgia’s graduated income tax structure that tops out at 6 percent with a regressive flat tax of 5.4 percent. Flat-rate income taxes typically lead to higher tax bills for workers in low-wage jobs, especially people without children who don’t gain as much from various credits and exemptions. A rate cut that large also could pose headaches for budget writers over the long term.

This report details a straightforward revision to the package that can allow lawmakers to keep the good parts and fix its chief flaw without compromising supporters’ main goals. This modification will keep Georgia’s graduated income tax and cut the top rate to 5.75 percent, rather than moving to a flat 5.4 percent rate. Adopting this fix or something similar offers a solution that lowers Georgia’s income tax rate, provides a bottom-up tax cut to working families and protects the state’s long-term finances. The reasons to ditch the 5.4 percent flat tax in favor of the 5.75 percent alternative include:

- Swapping out the flat tax for a modest cut to the top rate avoids raising taxes on low-wage workers. HB 329 as it now stands will raise taxes for low-wage workers without children, while taxpayers with children will get a modest cut. Revising the bill to keep Georgia’s longstanding graduated structure in place and drop the top rate to 5.75 percent cuts taxes for all people at poverty level incomes. A childless married couple earning $12,060 a year faces an estimated tax hike of $140 a year in the House-passed version of HB 329. The 5.75 percent alternative cuts that couple’s tax bill by $32.

- Middle-class families get a better deal without the flat tax. Enacting a modest rate cut within Georgia’s current system while preserving other aspects of HB 329 provides a larger tax cut for most middle-class families than the flat tax option. A married couple with one child who make $65,000 a year gets an estimated annual tax cut of $104 under the 5.75 percent option, compared to $50 with the flat tax.

- A graduated tax approach can offer an overall savings to taxpayers without jeopardizing key services. Flattening Georgia’s income tax rate to 5.4 percent can cause future headaches for Georgia budget writers as lost revenue mounts. Annual cost estimates for HB 329 as originally introduced ranged from about $20 million to $154 million in lost revenue according to two separate estimates from reliable sources.[1] The price will grow over time since some of the new tax-cutting measures are linked to inflation. Changing HB 329 to include a top rate cut to 5.75 percent within Georgia’s current graduated structure carries an estimated cost of $65 million a year. That’s still an overall tax reduction for Georgians but less of a long-term threat to key services like education.

Alternative Option Keeps Key Tenets of Bill, Allows for Top Rate Cut

House Bill 329 as it passed from the House to the Senate includes four major changes to Georgia’s personal income tax system. This proposed revision retains three of those changes and swaps the problematic flat tax for a reduction of Georgia’s top rate. The table below contrasts HB 329, the proposed revision and current law.

Revision Keeps Three Key Assets of House Tax Package, Swaps Flat Tax for Modest Rate Cut

| Current Law | HB 329 | Proposed Revision |

| Graduated income tax structure with rates from 1% to 6% | Flat income tax rate set at 5.4% | Graduated structure with rates from 1% to 5.75% |

| No state Earned Income Tax Credit (EITC) | Nonrefundable EITC set at 10% of federal credit | Nonrefundable EITC set at 10% of federal credit |

| Itemizers allowed to deduct state income taxes on state return (double deduction) | Eliminates double-deduction loophole | Eliminates double-deduction loophole |

| Broadly available exemptions* not indexed to inflation | Exemptions indexed to inflation | Exemptions indexed to inflation |

Source: Georgia Code Title 48 and House Bill 329; *Broadly available deductions include the standard deduction, personal exemption and dependent exemption

Revised Approach Can Cut Rate While Avoiding Pitfalls of Flat Tax

The key to understanding HB 329 is to know that flattening Georgia’s structure and cutting the top rate to 5.4 percent are not intrinsically linked. Cutting the tax rate is one distinct policy choice and creating a flat tax is another. The wisdom of cutting the top rate is debatable, but pitfalls of a flat tax are well-known. The flat-rate approach typically leads to higher income tax bills for low-wage workers, especially childless adults who receive fewer benefits from various credits and exemptions.[2]

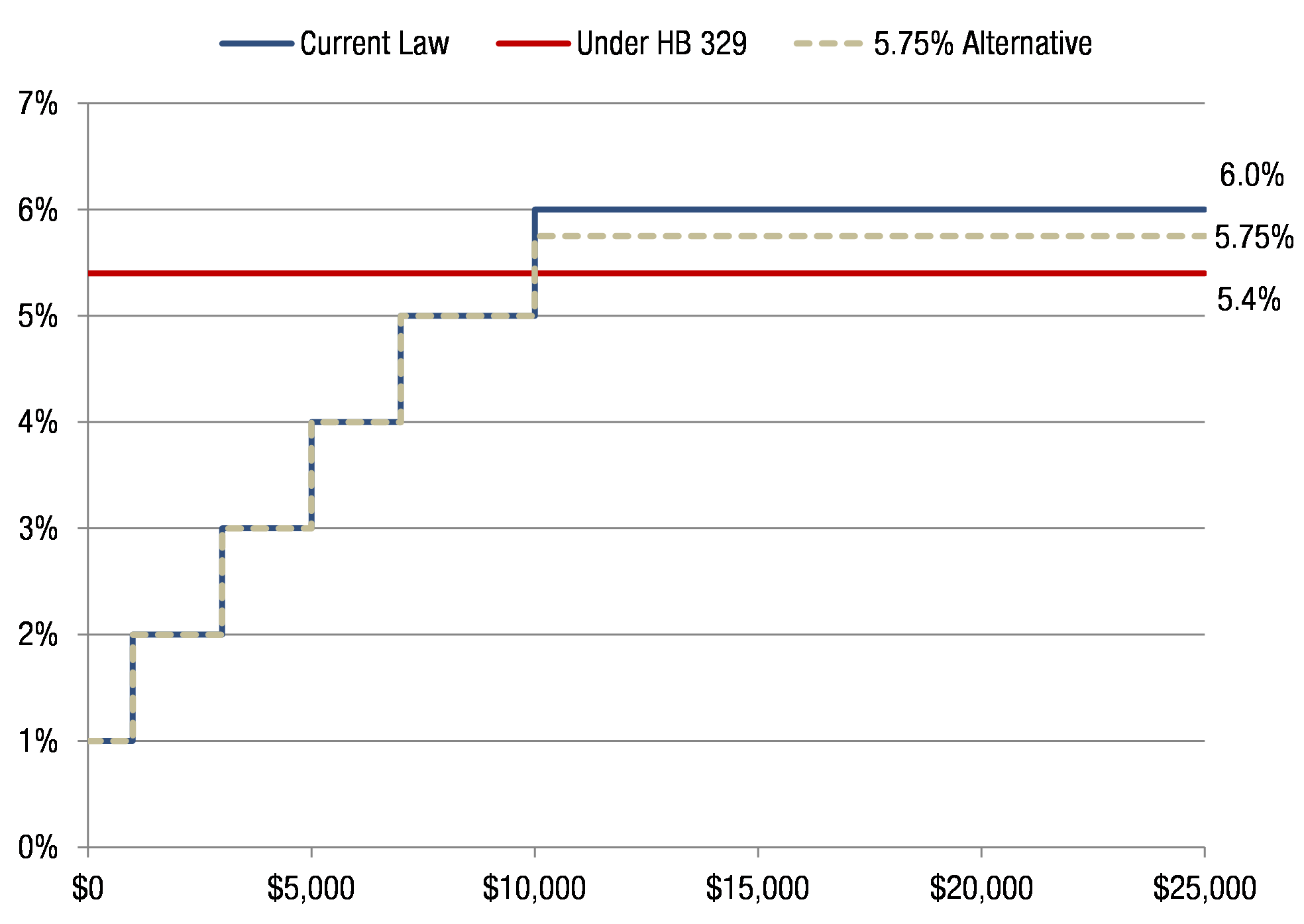

How Tax Rates Vary Under Plans

Marginal Georgia tax rates by income, married filing jointly, current law vs. alternatives

Lawmakers can avoid the flat tax downside while still reducing Georgia’s top rate in a responsible manner. The key is keeping Georgia’s graduated income tax structure in place rather than moving to a single, lower flat rate. Couples filing jointly still stand to pay 1 percent on their first $1,000 of taxable income, 2 percent on their second $2,000 of taxable income and so on, as they do under today’s system. In the preferred approach, taxpayers pay 5.75 percent once the top rate kicks in at $7,000 of taxable income for a single taxpayer and $10,000 for a married couple. The chart contrasts the effect of the flat tax plan and cutting the top rate within Georgia’s existing system.

Modest Rate Cut a Better Deal for Taxpayers than Flat Tax

The version of HB 329 that passed the House March 1, 2017 raises taxes for low-wage childless workers, while most taxpayers with children stand to get a modest cut. This is caused by moving to a flat tax and enacting an EITC at the same time. The former raises taxes for all low-wage workers and the latter offsets that increase just for families raising dependent children. A childless single worker living at the poverty line gets an estimated annual tax hike of $126 in the House-backed plan, to cite one example. In contrast, a single parent living at the poverty line with two children gets an estimated annual tax cut of $311.

Tweaking the tax plan to cut the top rate to 5.75 percent rather than flattening it at 5.4 percent eliminates this uneven treatment of Georgians in low-wage jobs. The table below details how taxpayers at the federal poverty line fare in two different version of the bill. With a 5.4 percent flat tax, HB 329 reduces income taxes for poor families with children but raises them for childless adults. In contrast, a revised version of the package that keeps the graduated structure and drops the top rate to 5.75 percent cuts taxes for all people living at poverty level.

A married couple without children faces an estimated tax increase of $140 a year due to the House-passed version of HB 329. The 5.75 percent alternative cuts that couple’s taxes by an estimated $32 a year. That happens because the couple gains a small benefit from both the rate cut and the new EITC, without losing money from higher rates on smaller amounts of income captured by a flat tax.

Swapping 5.4% Flat Tax for 5.75% Top Rate Delivers Low-Wage Workers a Better Deal

| Family Type | Poverty Line | State Income Taxes Owed | Change from Current Law | |||

| Current Law | HB 329 with flat 5.4% | HB 329 with graduated 5.75% | Flat 5.4% | Graduated 5.75% | ||

| Single, no children | $12,060 | $226 | $352 | $204 | $126 | $(22) |

| Single, one child | $16,240 | $242 | $98 | $0 | $(144) | $(242) |

| Single, two children | $20,420 | $311 | $0 | $0 | $(311) | $(311) |

| Married, no children | $16,240 | $134 | $273 | $102 | $140 | $(32) |

| Married, one child | $20,420 | $191 | $42 | $0 | $(149) | $(191) |

| Married, two children | $24,600 | $250 | $0 | $0 | $(250) | $(250) |

Source: GBPI calculations using Georgia Code Title 48, Department of Revenue tax tables, House Bill 329 and IRS tables for Earned Income Credit. Calculations assume taxpayers take standard deduction rather than itemize.

Middle-class families also benefit from substituting a modest rate cut for a flat tax. The table below details how the two proposals might affect the wallets of workers whose annual wages sit at the midpoint of Georgia’s wage scale, or about $32,500 per full-time worker.[3] Five of the six taxpayer-types at this middle-income level stand to gain a larger tax cut from the graduated 5.75 percent alternative. So a married couple with two children that makes $65,000 a year receives an estimated annual tax cut of $97 under the 5.75 percent alternative, compared to a $32 cut under the 5.4 percent flat tax. A single parent of one child gains a $145 cut from the 5.75 percent option versus a $4 hike under the 5.4 percent flat tax.

Most Middle-Class Georgians Stand to Gain More from 5.75% Alternative

| Family Type | Median Annual Wage* | State Income Taxes Owed | Change from Current Law | |||

| Current Law | HB 329 with flat 5.4% | HB 329 with graduated 5.75% | Flat 5.4% | Graduated 5.75% | ||

| Single, no children | $32,500 | $1,460 | $1,485 | $1,409 | $25 | $(51) |

| Single, one child | $32,500 | $1,210 | $1,214 | $1,065 | $4 | $(145) |

| Single, two children | $32,500 | $1,030 | $905 | $745 | $(125) | $(285) |

| Married, no children | $65,000 | $3,016 | $2,948 | $2,967 | $(68) | $(49) |

| Married, one child | $65,000 | $2,836 | $2,786 | $2,732 | $(50) | $(104) |

| Married, two children | $65,000 | $2,656 | $2,624 | $2,560 | $(32) | $(97) |

Source: GBPI calculations based on Georgia Code Title 48, Department of Revenue income tax tables, House Bill 329 and IRS tables for Earned Income Credit; *Median annual wage for married couples assume both adults work full-time at the state’s 2015 median wage of $32,460/year (Economic Policy Institute). Calculations assume taxpayers take standard deduction rather than itemize.

Revised Tax Plan Offers Overall Savings to Taxpayers, Minimizes Revenue Risk

The reduction of Georgia’s income tax rate to 5.4 percent in the House tax restructuring plan is a deep enough cut that it may cause future headaches for Georgia budget writers as lost revenue mounts. Again, the annual cost of HB 329 as it passed the House could range from about $20 million to $154 million in lost revenue. Indexing the standard deduction and personal and dependent exemptions to inflation, an element added after the original cost estimates, also increases the long-term price of the package. The inflation factor could add another $34 million a year to HB 329’s cost, which brings the ceiling of the House-passed version of the bill up to an estimated $188 million a year in lost revenue.[4] Changing HB 329 to include a rate cut of 5.75 percent within Georgia’s current graduated structure instead carries an estimated cost of $65 million a year. So Georgia taxpayers can still gain an overall reduction in income taxes but face less risk of future funding challenges for vital services like education.

Conclusion: Modest Fix Holds Potential for Broadly Supported Win on Tax Reform

The HB 329 legislation might be the most significant tax reform package to pass Georgia’s legislature in years. Lawmakers can pursue a straightforward option to keep the positive parts of the bill as it stands, fix the remaining flaw and still hold true to supporters’ main goals. Removing the 5.4 percent flat tax in favor of reducing the top rate of Georgia’s traditional graduated system to 5.75 percent, while keeping the three other components of the package, can deliver middle class families a tax cut without saddling low-wage workers with a tax hike. Adopting this fix or a close equivalent offers a better solution that lowers Georgia’s tax rate, provides a bottom-up tax cut to working families and protects the state’s long-term revenues.

Endnotes

[1] The state’s official fiscal note estimates the price of HB 329 at about $19.5 million a year once fully phased-in starting in the 2019 budget year. An alternative estimate from the nonpartisan Institute on Taxation and Economic Policy in Washington, D.C. estimates the annual cost at $154 million a year.

[2] “Fairness Matters: A Chart Book on Who Pays State and Local Taxes,” Institute on Taxation and Economic Policy. 2017.

[3] Georgia’s median wage in 2015 was $16.23 an hour which equates to $32,460 a year at full-time hours. Underlying hourly number comes from analysis of the Current Population Survey by the nonpartisan Economic Policy Institute.

[4] Institute on Taxation and Economic Policy. Custom analysis provided to GBPI by email on March 3, 2017.

Cover photo by Wonderlane under CC BY 2.0