This report offers the first comprehensive look at how the Tax Cuts and Jobs Act of 2017 (TCJA), in combination with Georgia’s enacted response, will impact the state budget and families at every level of income from 2020–2025. In partnership with Step Up Savannah and the Institute on Taxation and Economic Policy (ITEP), a case study of the City of Savannah is also included alongside GBPI’s statewide analysis to provide an in-depth look at how these major tax policy changes are affecting communities across the state.

Executive Summary

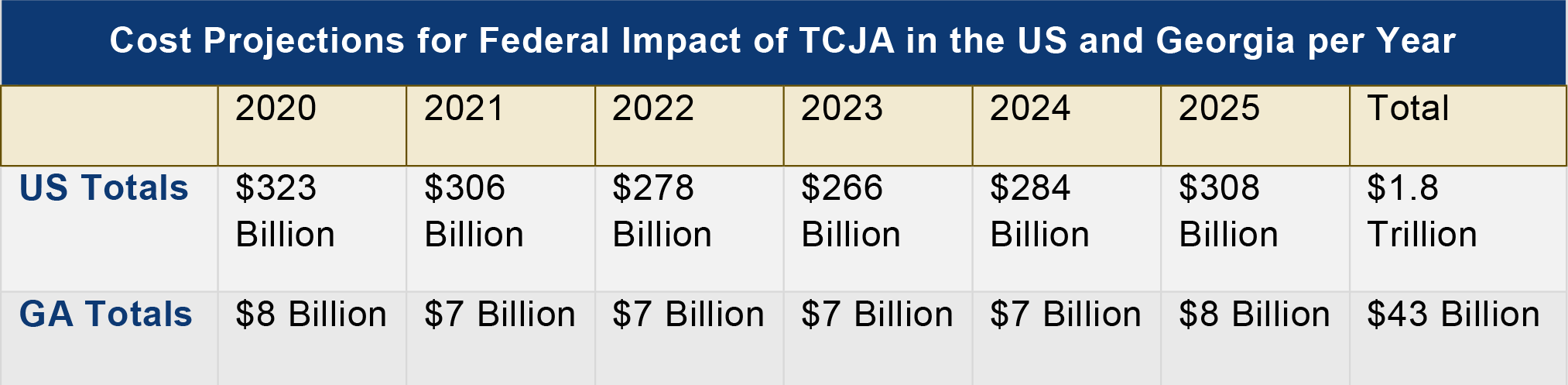

The Tax Cuts and Jobs Act (TCJA) fundamentally changes how millions of Georgians and state-based businesses will calculate their income taxes from 2020–2025, reducing federal revenue collections from Georgians by more than $43 billion and reshaping the structure of the state’s main source of revenue.

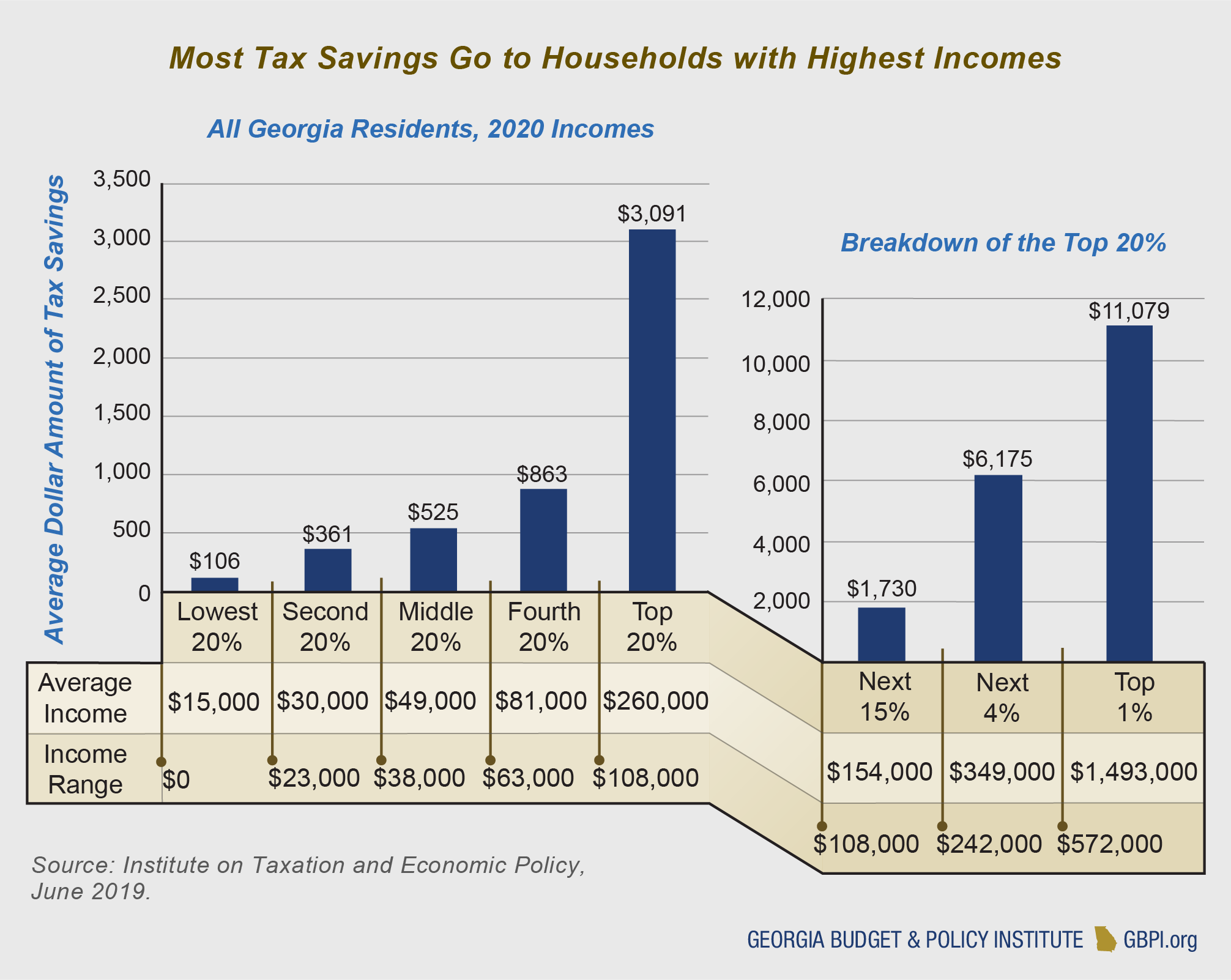

While TJCA reduces federal personal income taxes for 88 percent of residents, the vast majority of tax cuts benefit upper-income households. In 2020, about 75 percent of Georgia’s total tax savings will go to households earning more than $108,000 annually. The Georgians who gain the least are the 1.9 million families and individuals with incomes less than $38,000 per year. These 40 percent of households will collectively receive less than 6 percent of the total tax savings distributed across the state.

|

Major Provisions of the Tax Cuts and Jobs Act:

|

Georgia’s State Tax Changes to TCJA (HB 918; Expires 2025):

|

Although the state of Georgia taxes income at much lower rates than the federal government, the decisions filers make on their federal tax returns partly determines the amount of state taxes they owe. State filers are required to follow the same selection used on their federal income tax returns of whether to claim a flat standard deduction (set independently by the state) or to individually itemize deductions. Georgia is the only state with these filing requirements that allows taxpayers to deduct state and local income taxes with an itemized deduction, also known as the double deduction.

Each year, the General Assembly advances legislation to align the state’s tax code to match the filing guidelines for about 95 percent of federal itemized income tax deductions.[1] TCJA adds new limits to some of the most widely claimed and costly itemized deductions and doubles the federal standard deduction. Notably, TCJA caps the value of the federal deduction for state and local taxes (SALT) at $10,000, which resulted in applying the same limit to Georgia’s double deduction. The legislation also removes the “Pease Limitation,” which previously capped the value of certain itemized deductions for high earners.

Prior to TCJA’s approval, approximately 69 percent of individuals and families elected to take the standard deduction. As a result of the new federal law, an overwhelming 86 percent of Georgia filers will determine their taxable income using the standard deduction.[2] By simply updating the income tax provisions sourced from federal law—which caused more people to claim the standard deduction, makes major changes to the value of itemized deductions and increases overall state corporate tax payments—the state of Georgia would have generated more than $1.1 billion in additional annual income tax revenues.

Instead of accepting a significant increase in state revenues, the General Assembly passed legislation in 2018 to double the state’s standard deduction and lower the top tax rate applied to personal and corporate income from 6 to 5.75 percent through 2025. Former Gov. Nathan Deal also reacted to TCJA’s changes to state income tax collections by increasing Georgia’s revenue estimate by $167 million midway through the 2018 legislative session. This increase allowed the General Assembly to fully fund the state’s public education system.[3] The amount necessary to close the funding gap for public education is roughly equivalent to the $130 million in net state revenues generated by the Legislature’s enacted response to TCJA.

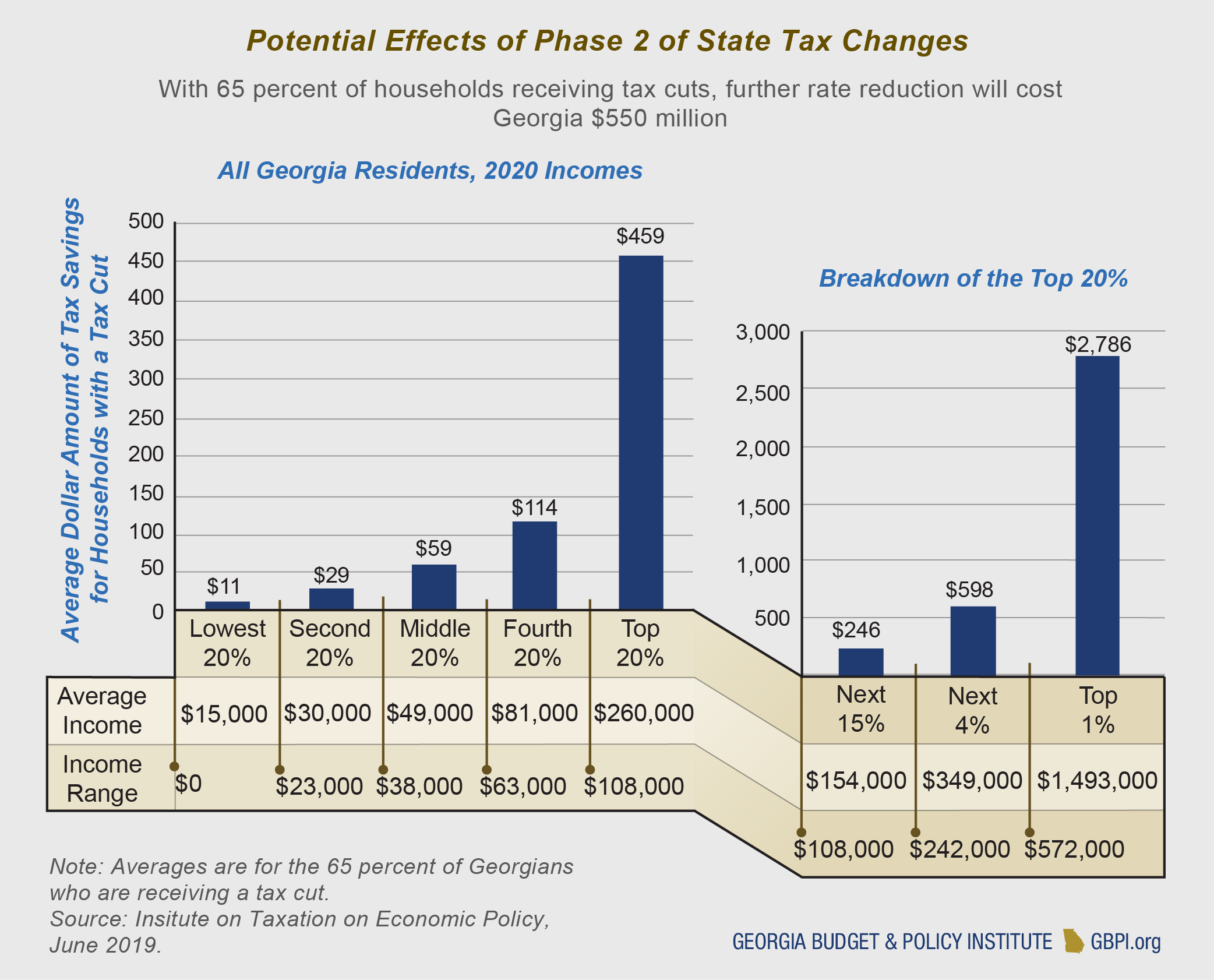

In contrast to the federal TCJA changes, Georgia’s tax changes reduced state taxes for 55 percent of residents with modest benefits distributed relatively equally across income levels. However, the enacted legislation also includes a provision for a potential second rate reduction, which requires the passage of a joint resolution by the General Assembly to further lower the top income tax rate from 5.75 to 5.5 percent through 2025.[4] If lawmakers adopt the additional rate cut, the middle 20 percent of Georgia households would experience an average income tax cut of just $42, while the state would lose $550 million in revenue in 2020.

TCJA’s tax cuts are made possible by the fact that the federal government’s deficit spending is at its highest-ever level outside of the Great Recession.[5] Unlike the federal government, the state of Georgia is required, by its constitution, to balance its budget each year. If a further income tax rate cut of 0.25 percent is adopted by the Legislature next year, the reduction in revenues would be equivalent to cutting about 2 percent of the entire state budget, which would likely require future spending cuts or off-setting tax increases to allow the General Assembly to meet its constitutional obligation of passing a balanced budget.

Overview of How the Tax Cuts and Jobs Act Affects State and Federal Income Taxes

Overview of How the Tax Cuts and Jobs Act Affects State and Federal Income Taxes

When Georgia’s income tax was first adopted in 1929, it was set at one-third of the federal rate.[6] In the years since, the growth of federal income tax revenues has far outpaced state collections. Today, Georgia’s state taxes are among the lowest in the nation, ranking 48th in general revenues per person.[7] Although the state’s response to TCJA makes changes to the formula Georgians use to calculate the amount they owe in income taxes, the vast majority of the overhaul’s effects will be felt through changes to the federal tax code.

In fiscal year 2020, the state of Georgia projects that it will raise $12.8 billion from the individual income tax (49 percent of general fund revenue collections) and $1.3 billion from the corporate income tax (5 percent). In comparison, in the last year reported (2018), the federal government collected approximately $79 billion from Georgians in gross personal income and employment taxes and nearly $9 billion in corporate income taxes.[8] Although the federal government collects more than six times the amount of revenue from these same sources, income taxes remain the primary funding source for the state.

Georgia’s tax code is structured to feature many of the same deductions and exemptions that exist at the federal level. These provisions, along with the state’s relatively low standard deduction, made Georgia taxpayers especially vulnerable to TCJA’s changes to federal law.

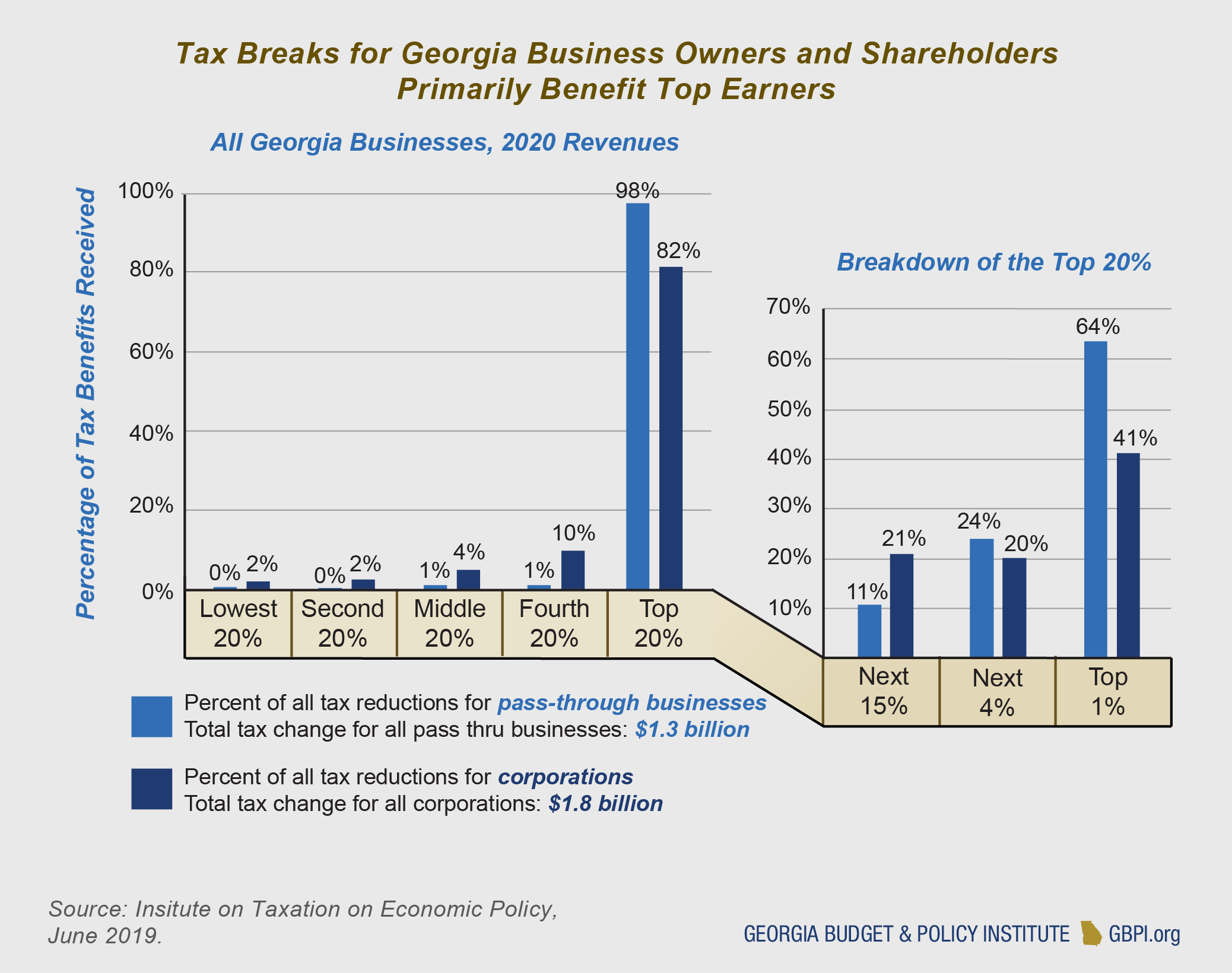

About 39 percent of the tax savings going to state residents are business tax cuts, which come in two parts. The first is $1.3 billion in tax savings in 2020 for “pass-through” companies, which do not independently pay taxes but instead pass through any profits or losses to their owners who include them on their personal income tax returns.

The second part of the business tax cuts is $1.8 billion in corporate tax cuts in 2020. This includes a permanent reduction in the federal corporate income tax rate from 35 percent to 21 percent and other changes. Based on the latest research on the effects of corporate taxes, the Institute on Taxation and Economic Policy (ITEP) assumes that most corporate tax cuts ultimately go to shareholders (including foreign investors) and a small portion goes to workers. High income taxpayers, who own most corporate stocks, receive the greatest benefits

While the federal corporate income tax changes do not have the same type of effect on state tax policy as those to the personal income tax, they are important to recognize because of the meaningful amount of revenue the federal government will forgo in cutting taxes for Georgians with the highest incomes. The General Assembly is set to consider a joint resolution in 2020 that would drop the top tax rates for both personal and corporate income from 5.75 to 5.5 percent.

Personal Income Tax Changes Favor Top Earners

In addition to reducing personal income tax rates through 2025, TCJA made significant changes to the formula used to calculate the amount of taxes owed by each household. Filers are still required to choose between accepting a flat standard deduction or taking advantage of a broader set of itemized deductions to determine the amount of their income that is taxed. However, the standard deduction and several of the most valuable itemized deductions underwent major revisions through TCJA.

Major Changes to the Personal Income Tax |

||

| Federal Income Tax Provision | Description | State Tax Changes, Phase 1 |

| Personal income tax rates brackets | Broadens income tax brackets and reduces federal tax rates. Does not restructure lowest income tax bracket, reduces rates for all other brackets[i] | Reduces the top state personal income tax rate from 6 to 5.75 percent ($456 million in 2020) |

| Pass-through business deduction | Allows the owners of qualifying pass-through businesses to deduct up to 20 percent from their business’ income tax liability | Not included in state tax changes |

| Standard deduction | Increases standard deduction from $6,500 to $12,200 for individuals (for the 2019 tax year), from $9,550 to $18,350 for heads of household and from $13,000 to $24,400 for married couples. Also changes the formula used to calculate the rate of inflation, slowing the standard deduction’s rate of growth | Through 2025, the state standard deduction increases from $3,000 to $4,600 for single filers and from $3,000 to $6,000 for married filers. Georgia does not index its state standard deduction to keep pace with inflation ($515 million in 2020) |

| Child Tax Credit | Increases the child tax credit from up to $1,000 to up to $2,000 per qualifying child (up to $1,400 of which is refundable, meaning that families can still receive the credit as a tax refund if it exceeds what they owe in taxes) | Not included in state tax changes |

| Personal exemption | Eliminates the federal personal exemption, which previously allowed each taxpayer (including any dependents) to claim a deduction of $4,150. Removing this exemption offset a large share of the gains that many lower-income taxpayers would otherwise receive | Georgia’s leaders maintained the state’s existing personal and dependent exemptions, which are set at $2,700 for single filers, $7,400 for married couples and $3,000 per dependent (additional state deductions are also available for taxpayers over 65 and legally blind individuals) |

| Pease Limitations on itemized deductions | Repeals limits that previously reduced the value of itemized deductions for upper-income taxpayers. This provision reduced the value of itemized deductions by 3 percent of every dollar of taxable income over certain thresholds, capping the total reduction at 80 percent of the value of itemized deductions claimed. In 2017, the threshold was $261,500 for individuals and $313,800 for married couples | Included in state tax changes |

| Deduction for State and Local Taxes (SALT) |

Caps the itemized deduction for state and local taxes (SALT) at $10,000 | Included in state tax changes, which had an outsized effect on state revenues because of Georgia’s unique status in offering this state-level tax break |

| Deduction for mortgage interest |

Limits the itemized deduction for mortgage interest to $750,000 of mortgage debt | Included in state tax changes |

| Other deductions | Eliminates several itemized deductions, including casualty and theft loss deduction, moving expense deduction and deduction for home equity loan interest | Included in state tax changes |

| 529 Accounts | Allows for tax-free contributions of up to $10,000 for 529 account savings plans designed to cover college expenses, which were also expanded under the law to include K-12 tuition | Included in state tax changes and adopted through additional legislation (HB 266) |

Overall, 77 percent of TCJA’s $7.9 billion impact will be delivered to Georgians in 2020 through the personal income tax with changes that directly impact individuals, families and pass-through business owners.

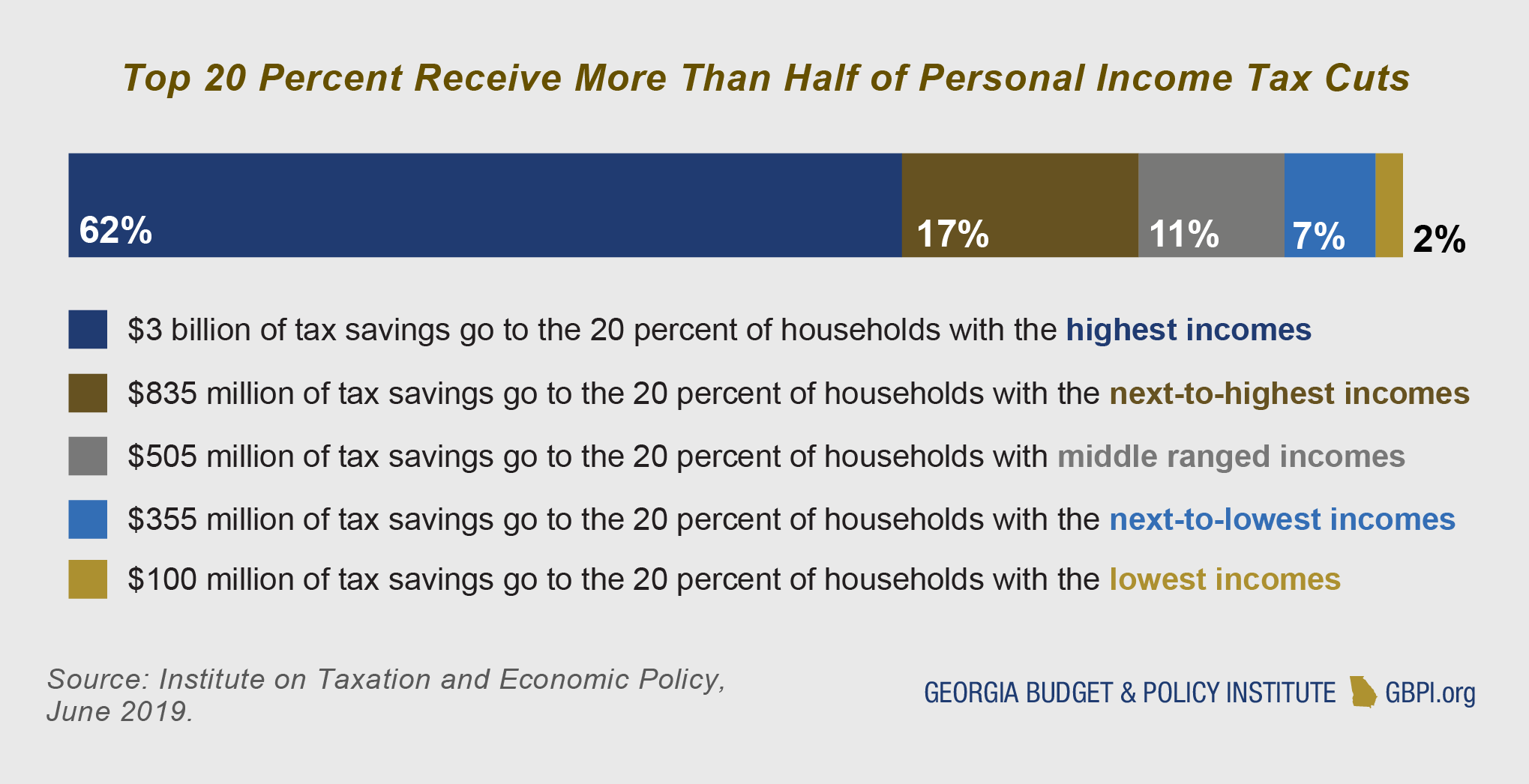

Of $4.8 billion in tax cuts for individuals and families, more than half of these savings ($2.4 billion) will go to the nearly 20 percent of individuals and families—916,000 households—earning between $108,000 to $572,000 per year. This group does not include the top 1 percent of households who will collect the largest average tax cuts of $11,000, which will total $540 million next year. The savings shared by these 49,000 filers may represent only a fraction of TCJA’s total impact, but it still far exceeds the $455 million that will be divided between the 1.9 million Georgia taxpayers with the lowest incomes.

TCJA Directly Reshapes Georgia’s State Income Tax

TCJA Directly Reshapes Georgia’s State Income Tax

Georgia is one of a handful of states that requires taxpayers to follow the same selections used to file federal taxes when submitting their state returns. This includes a taxpayer’s filing status (head of household, married filing jointly, etc.) and choice of whether to accept the standard deduction or itemize deductions. One of the prominent features of TCJA was to double the federal standard deduction. Unfortunately, most of the tax-reducing effects of this change were offset by the elimination of the federal personal exemption, which previously offered a deduction valued at $4,150 to all taxpayers and each of their dependents regardless of their decision to itemize or claim the standard deduction.

Prior to the implementation of TCJA, approximately 31 percent of the state’s residents itemized.[10] Those who did had an average income of $173,000, while residents using the standard deduction earned an average of $42,000. Partly because TCJA limited several of the most popular tax breaks, a large group of taxpayers shifted from itemizing to using the standard deduction. In 2020, 86 percent of Georgians are expected to file their state and federal taxes using the standard deduction, with an average income of $57,000.[11] Among the estimated 14 percent of filers who will itemize in future tax years, household earnings will average $240,000.

Prior to the implementation of TCJA, approximately 31 percent of the state’s residents itemized.[10] Those who did had an average income of $173,000, while residents using the standard deduction earned an average of $42,000. Partly because TCJA limited several of the most popular tax breaks, a large group of taxpayers shifted from itemizing to using the standard deduction. In 2020, 86 percent of Georgians are expected to file their state and federal taxes using the standard deduction, with an average income of $57,000.[11] Among the estimated 14 percent of filers who will itemize in future tax years, household earnings will average $240,000.

Of approximately $1 billion in offset tax cuts in 2020, the state estimates that more than $515 million will be absorbed by increasing the standard deduction.[12] Even with the General Assembly’s decision to double the state standard deduction, it remains far lower than its federal counterpart, which TCJA sets at $12,200 for individuals and $24,400 for married couples in 2019. Rather than significantly reducing taxes, the state’s legislative tax changes primarily acted to prevent a majority of Georgians from experiencing a tax increase as a result of TCJA’s changes.

Estimates show that aligning the state’s tax code with the new federal limits on deductions and tax breaks alone would have generated up to $1.1 billion annually in new income tax revenue.[13] Ultimately, however, in addition to mirroring most of the federal changes through 2025, Georgia’s leaders advanced a legislative package that doubled the state’s standard deduction, lowered the top income tax rate from 6 to 5.75 percent and established a trigger to potentially further reduce the rate to 5.5 percent in 2020.

Under the state’s 2018 legislative package, Georgia’s leaders maintained the state’s personal and dependent exemptions, while doubling the state’s standard deduction to $4,600 for individuals and $6,000 for married couples. All state filers remain eligible for a $3,000 exemption per dependent and a personal exemption of $2,700 for single taxpayers or $7,400 for married couples.

Georgia allows taxpayers to claim an itemized deduction for state and local taxes (SALT) on their state income tax returns. Before a $10,000 cap was placed on the federal SALT deduction, which was also applied to the state’s tax code, the tax break cost more than $500 million annually. Prior to adopting this change, the SALT deduction, which is more widely known as the double deduction because of how it functions at the state level, was Georgia’s most frequently claimed itemized tax break.[14] Georgia continues to offer a more limited version of the double deduction, which will cause the state to forgo approximately $120 million in 2020 tax collections.[15]

At first glance, the enacted provisions of Georgia’s TCJA response are producing generally positive results. Although a larger percentage (88 percent) of taxpayers will receive at least some savings from the federal changes, a majority of households (55 percent) will also experience a tax cut as a result of the state’s tax changes. Under the changes made to Georgia’s tax code, individuals and families across most income groups will receive a roughly equal share of the tax benefits.

Still, those who fall among the 950,000 taxpayers earning less than $23,000 will only receive a 12 percent share of the state tax cut. This group, which represents approximately 20 percent of the state’s filers, will experience less than 2 percent of TCJA’s direct benefits.

On the other hand, the top 20 percent of earners will see 26 percent of the total benefits of Georgia’s state tax changes. All other filers, representing about 60 percent of households, will receive a roughly equal share of the state-level tax cuts.

On the other hand, the top 20 percent of earners will see 26 percent of the total benefits of Georgia’s state tax changes. All other filers, representing about 60 percent of households, will receive a roughly equal share of the state-level tax cuts.

A provision to further cut the income tax was also included in Georgia’s TCJA response legislation. Lawmakers will have the option to reduce the top income tax rate from 5.75 to 5.5 percent by passing a joint resolution during the 2020 legislative session.

Implementing this cut would cost the state approximately $550 million in 2020. Although a 0.25 percent tax rate reduction pales in comparison to $43 billion in federal tax cuts that are set to occur through 2025, the cost of this pending tax break represents about 2 percent of Georgia’s $27.5 billion budget. For perspective, the $3,000 pay raise for Georgia’s public school teachers and staff will cost approximately $530 million in fiscal year 2020. Gov. Kemp has also called for an additional $2,000 pay raise for educators, which, if implemented, is likely to cost at least $350 million per year.

Nearly 40 percent of TCJA’s benefits for Georgia in 2020 are provisions for corporations (which are subject to the federal corporate income tax) and pass-through entities (which are not).

Corporations accounted for 47,000 of the state’s tax returns filed and owed a total of $9 billion in federal taxes in 2018.[16] As explained in the methodology section, the benefits of corporate tax cuts initially go to shareholders who own stocks in American corporations. The Institute on Taxation and Economic Policy (ITEP) follows the approach of Congress’s official revenue estimator, the Joint Committee on Taxation (JCT), which estimates that a small share of the benefits from corporate tax cuts will also eventually benefit workers.

Georgians will benefit from $1.8 billion in federal corporate income tax cuts in 2020 including a reduction in the corporate tax rate from 35 percent to 21 percent and other changes. The other category of businesses benefiting from TCJA are pass-throughs that do not directly pay taxes but rather pass through any profits or losses to their owners, who claim that income on their personal tax returns.

About 98 percent of $1.3 billion in tax cuts targeted toward pass-through businesses will go to filers with incomes that rank among the top 20 percent of earners. The tax cuts for these businesses offer the most disproportionate benefits to upper-income filers of any TCJA provision. Moreover, no other change authorized by TCJA will distribute a greater total amount to taxpayers earning more than $572,000 annually. In total, qualifying pass-through businesses with incomes in the top 1 percent of earners will receive more than $824 million in tax cuts next year.

About 98 percent of $1.3 billion in tax cuts targeted toward pass-through businesses will go to filers with incomes that rank among the top 20 percent of earners. The tax cuts for these businesses offer the most disproportionate benefits to upper-income filers of any TCJA provision. Moreover, no other change authorized by TCJA will distribute a greater total amount to taxpayers earning more than $572,000 annually. In total, qualifying pass-through businesses with incomes in the top 1 percent of earners will receive more than $824 million in tax cuts next year.

Georgians to Save $1.8 Billion in Federal Corporate Taxes in 2020

TCJA made sweeping changes to the corporate tax, permanently setting a flat 21 percent federal income tax rate for corporations, reduced from 35 percent. The $1.8 billion share of TCJA’s corporate tax cuts next year is equivalent to nearly 150 percent of the total amount of corporate income tax that the state of Georgia expects to collect in 2020. The federal tax law also applied several other major changes to the corporate income tax, including:

- Eliminating the corporate alternative minimum tax

- Expanding depreciation deductions

- Eliminating and scaling back some itemized deductions

- Instituting new international tax rules for multinational corporations

While the savings realized through the corporate tax are more evenly distributed than those delivered to pass-through businesses through the personal income tax, most of the impact from TCJA changes will be felt by the state’s highest income filers. With 26 Fortune 1000 companies headquartered in metro Atlanta, large industries are a core element of Georgia’s economy. Some of these locally based corporations have long been known to avoid federal income taxes.[17] Nevertheless, the corporate tax code changes will have significant effects for Georgians.

While the savings realized through the corporate tax are more evenly distributed than those delivered to pass-through businesses through the personal income tax, most of the impact from TCJA changes will be felt by the state’s highest income filers. With 26 Fortune 1000 companies headquartered in metro Atlanta, large industries are a core element of Georgia’s economy. Some of these locally based corporations have long been known to avoid federal income taxes.[17] Nevertheless, the corporate tax code changes will have significant effects for Georgians.

Corporate Tax Changes Lift State Revenue

Although TCJA’s tax changes are likely to only further erode corporate tax collections at the federal level, Georgia’s corporate income tax revenues increased more than 25 percent during the 2019 fiscal year. While this trend has important consequences, corporate income tax revenues represent less than 5 percent of the state’s budget, a total of $1.3 billion for fiscal year 2020. This revenue source is roughly equivalent to the total collected by the Georgia Lottery, which funds the HOPE Scholarship for higher education and the state’s Pre-K program.

At least part of the uptick in state corporate tax revenues could be temporary benefits initiated by TCJA’s implementation. For example, in addition to reducing the corporate income tax rate, the legislation also included provisions related to multinational corporations, major revisions to business deductions and other changes that could explain the recent volatility in state corporate income tax collections.

It is also worth noting that the state of Georgia operates on a fiscal year that begins on July 1, while corporate tax returns are due to the Department of Revenue by the 15th of March for calendar year corporations or, for fiscal year corporations, on or before the 15th day of the third month following the end of their fiscal year.[18] Because of the significant gap between when the state reports revenue collections and tax filing deadlines, more time is needed to fully understand the impact of TCJA on state corporate income tax revenues.

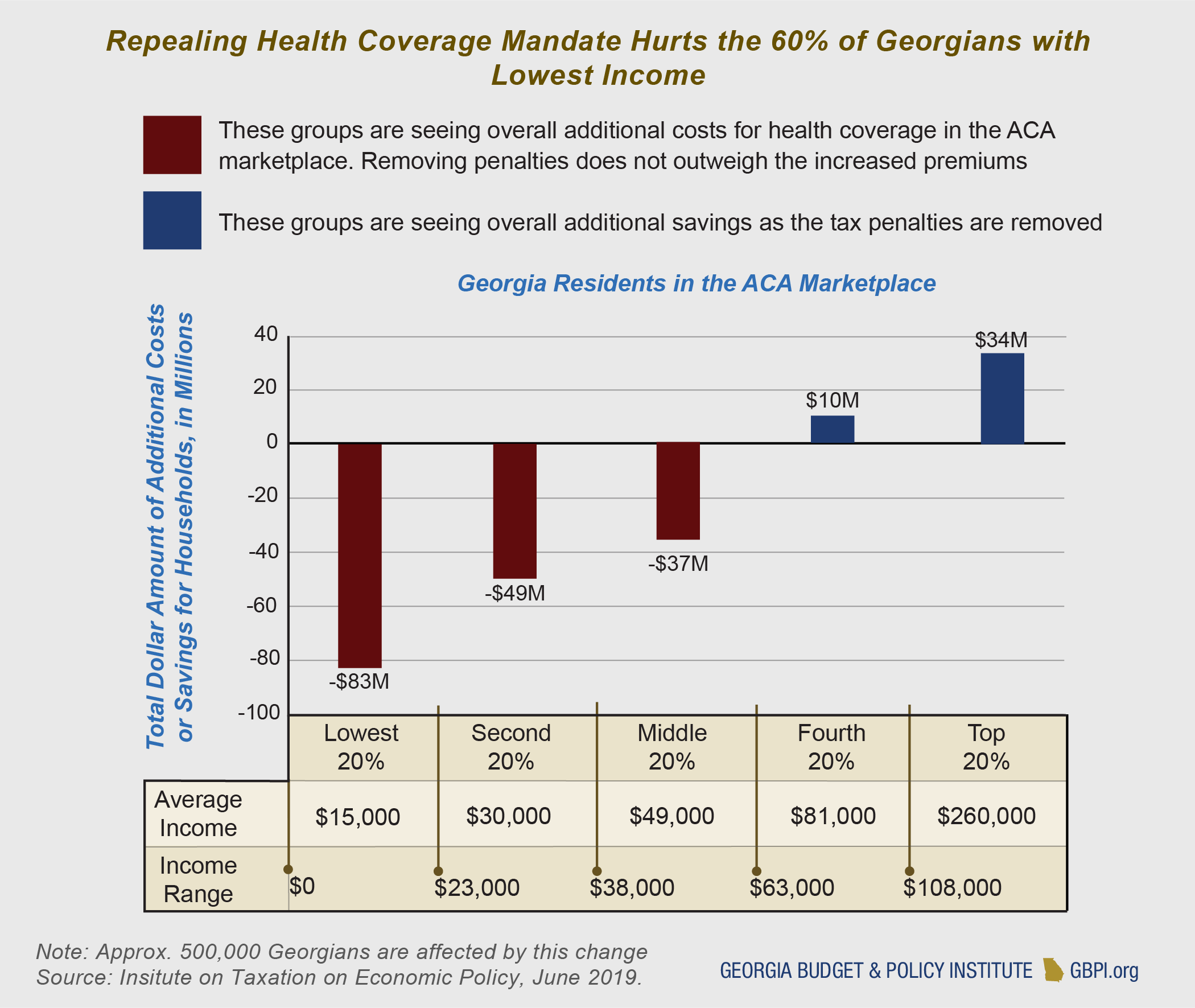

Repeal of Coverage Requirement Will Increase Health Care Costs for Georgians

The TCJA permanently zeroed out the income-based tax penalty assessed to individuals who fail to maintain health coverage. The maximum personal income tax penalty applied under the individual mandate was previously set at $2,085 per family or 2.5 percent of income, whichever amount was greater. Created by the Affordable Care Act, the individual mandate was intended to encourage younger, healthier people to purchase insurance to help create a stable marketplace.

Currently, 27 percent of young adults (19–34) in Georgia are uninsured, the second highest rate in the nation.[19] With more than 458,000 residents insured through the individual marketplace, Georgia has the fifth largest volume of enrollees of any state.[20] The Institute on Taxation and Economic Policy (ITEP) estimates that repealing the health coverage requirement will raise costs for customers of Georgia’s insurance marketplace by about 10 percent in 2020. The brunt of these increases will fall on those whose earnings are below the state’s middle 20 percent of incomes.

Changes to Estate and Gift Tax Rules Further Lift Top Earners

Changes to Estate and Gift Tax Rules Further Lift Top Earners

Beyond personal and corporate income taxes, TCJA also makes major changes to the estate and gift tax exemption. Prior to the TCJA’s enactment, single filers were eligible for exemptions of up to $5.6 million from the estate and gift tax and married filers were allowed up to $11.2 million. Through 2025, TCJA doubles the value of the estate and gift tax exemption, up to $11.2 million for individuals and $22.4 million for a married couple. The law also allows a surviving spouse to transfer the unused portion of a deceased spouse’s eligible estate tax exemption. These changes are likely to benefit only the wealthiest households, reducing estate taxes by $127 million in 2020. In 2018, the federal estate and trust income tax generated approximately $570 million in revenues, while the state of Georgia fully eliminated its estate tax in 2014.[21]

Analysis and Recommendations

In Georgia, the most significant consequence of the Tax Cuts and Jobs Act is that $43 billion in tax savings will be distributed through the federal tax code from 2020–2025, predominately benefitting the highest income households, businesses and estates.

In 2020, the majority of $7.9 billion in total benefits will go to the state’s top-income earners. Although it is true that about 88 percent of Georgia taxpayers will receive some direct benefits from TCJA, families with incomes that rank them among the first 40 percent of households will receive less than 6 percent of the federal legislation’s total statewide impact. In terms of the state’s tax changes, Georgia still has an opportunity to leverage its unique tax code to maximize the benefits directed to working families. For most households that fall outside of the upper-middle-class, the federal tax cuts will do relatively little to change their annual earnings.

In terms of the TCJA’s economic effects, a 2019 preliminary analysis of the legislation’s impact by the Congressional Research Service concluded, “On the whole, the growth effects tend to show a relatively small (if any) first-year effect on the economy.”[22] From 2017 to 2018, national real wages grew at 2 percent, and real gross domestic product (GDP) grew by 2.5 percent (revised). In the first two quarters of 2019, GDP grew by 3.1 percent and 2.1 percent, respectively.[23]

Although Georgia’s economy is in its ninth consecutive year of economic expansion and has sustained strong growth in recent years, state revenue growth is projected to register at 3.2 percent in fiscal year 2020, the lowest level since the Great Recession.[24] Nationally, concerns about the economy were also elevated in July 2019, when the Federal Reserve acted to reduce interest rates for the first time since 2008, citing “global developments for the economic outlook” and “soft” growth in business investment. This rate change influences what banks and financial institutions charge for short-term borrowing.[25]

Pending Rate Cut Offers Little Benefit to Most Georgians, Threatens to Further Weaken Income Tax Revenues

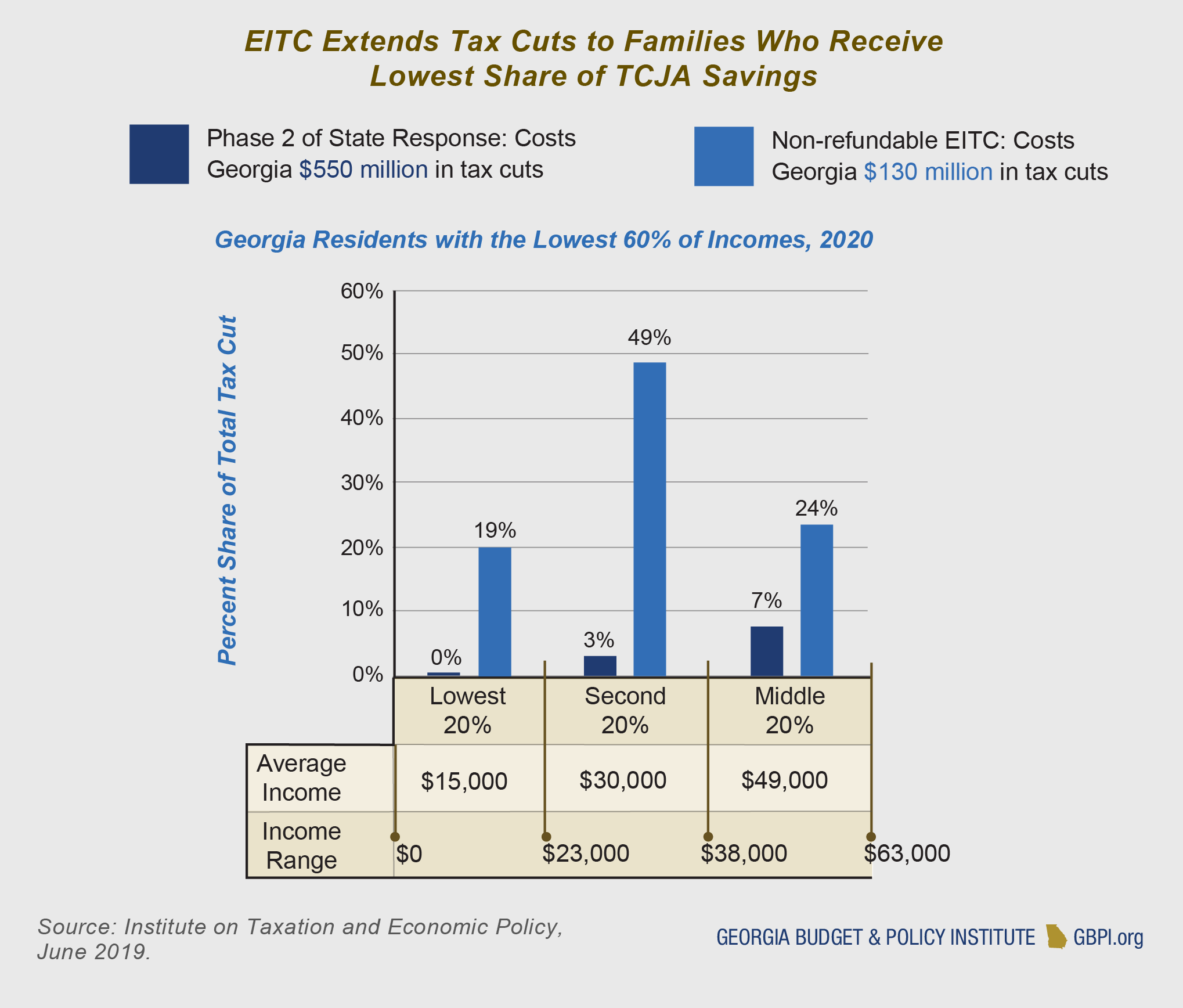

Reducing the top income tax rate from 5.75 to 5.5 percent would have an insignificant impact on the amount of income taxes that the vast majority of Georgians pay. The state would be best served by preserving the strength of its largest and most dependable source of revenue. It is also important to note that personal income tax collections, which make up 48 percent of general fund revenues, underperformed over the last fiscal year and fell short of the state’s 2019 revenue estimate by $127 million.[26] Although the first phase of the state tax changes did not significantly affect tax collections because it was offset by TCJA’s revenue-raising provisions, the fact that income tax payments fell short of the state’s revenue estimate in the last fiscal year further signals that Georgia’s budget writers are not prepared to forgo an additional $550 million in revenue in 2020.

Georgia Work Credit Would Provide Balance to Georgians Who Receive Few Benefits from TCJA

To improve the tax code, leaders should look to more targeted policy options that will strengthen the economic position of those with incomes that rank among the first 60 percent of Georgians. This group of approximately 2.9 million households has been largely left behind by TCJA’s reforms. These taxpayers will receive about 12 percent of the $7.9 billion in tax cuts that will flow into the state in 2020. In fact, households with the lowest incomes are most likely to get the proportionally smallest tax cuts.[27]

Going forward, instead of diverting $550 million in state revenues to implement a tax cut that would even further disproportionately benefit top-earning households, Georgia lawmakers would be wise to invest in working families and those striving to reach the middle class with proven tools like the Earned Income Tax Credit (EITC), which is designed to help pull families out of poverty by targeting and rewarding work, while avoiding the benefits cliff that can penalize low-income beneficiaries for earning even small wage increases.

Members of the General Assembly are considering adding an EITC, also known as the Georgia Work Credit, to the state’s tax code. Based on the long-standing federal tax credit, the Georgia Work Credit could cut taxes for up to 1.1 million Georgia families—24 percent of all households—who earn up to about $56,000 annually. The Georgians who receive the smallest share of TCJA savings would benefit most from a state EITC. Across the nation, 29 states have adopted credits structured in two ways. A refundable credit would allow filers to receive the full value they qualify for—even if it exceeds their income tax liability. A non-refundable credit would provide a more targeted tax cut applied against the amount of income tax owed to the state.

If members of the General Assembly want to grow the middle class or make the tax code more equitable while maximizing the state’s limited resources, the best way to achieve these goals is by investing resources in Georgians whose incomes fall closer to the median household, rather than redirecting further resources to those who have already reached the top of the economic ladder. The state can also continue to benefit from the positive consequences initiated by TCJA by further limiting inefficient tax breaks like the double deduction on state taxes and more closely evaluating the performance of costly tax expenditures.

If members of the General Assembly want to grow the middle class or make the tax code more equitable while maximizing the state’s limited resources, the best way to achieve these goals is by investing resources in Georgians whose incomes fall closer to the median household, rather than redirecting further resources to those who have already reached the top of the economic ladder. The state can also continue to benefit from the positive consequences initiated by TCJA by further limiting inefficient tax breaks like the double deduction on state taxes and more closely evaluating the performance of costly tax expenditures.

Georgia remains one of least-taxed states in the nation. However, those who earn the least, on average, pay the greatest portion of their incomes in combined state and local taxes.[28] Under the current revenue structure, state lawmakers face continued challenges in balancing the top priorities of a growing state—with pressing needs in education, health care, rural broadband and human services—while maintaining a balanced budget, one of Georgia’s constitutional requirements.

It was a wise decision to advance a response that includes a legislative trigger to help ensure that the state’s actions do not overreach and jeopardize Georgia’s fiscal health. Going forward, any attempts to further reduce taxes should focus on the considerable number of lower-income Georgia families who did not receive major benefits from TCJA, rather than on the highest-income earners who will receive billions in annual savings through 2025.

Case Study: How TCJA is Impacting the City of Savannah

Case Study: How TCJA is Impacting the City of Savannah

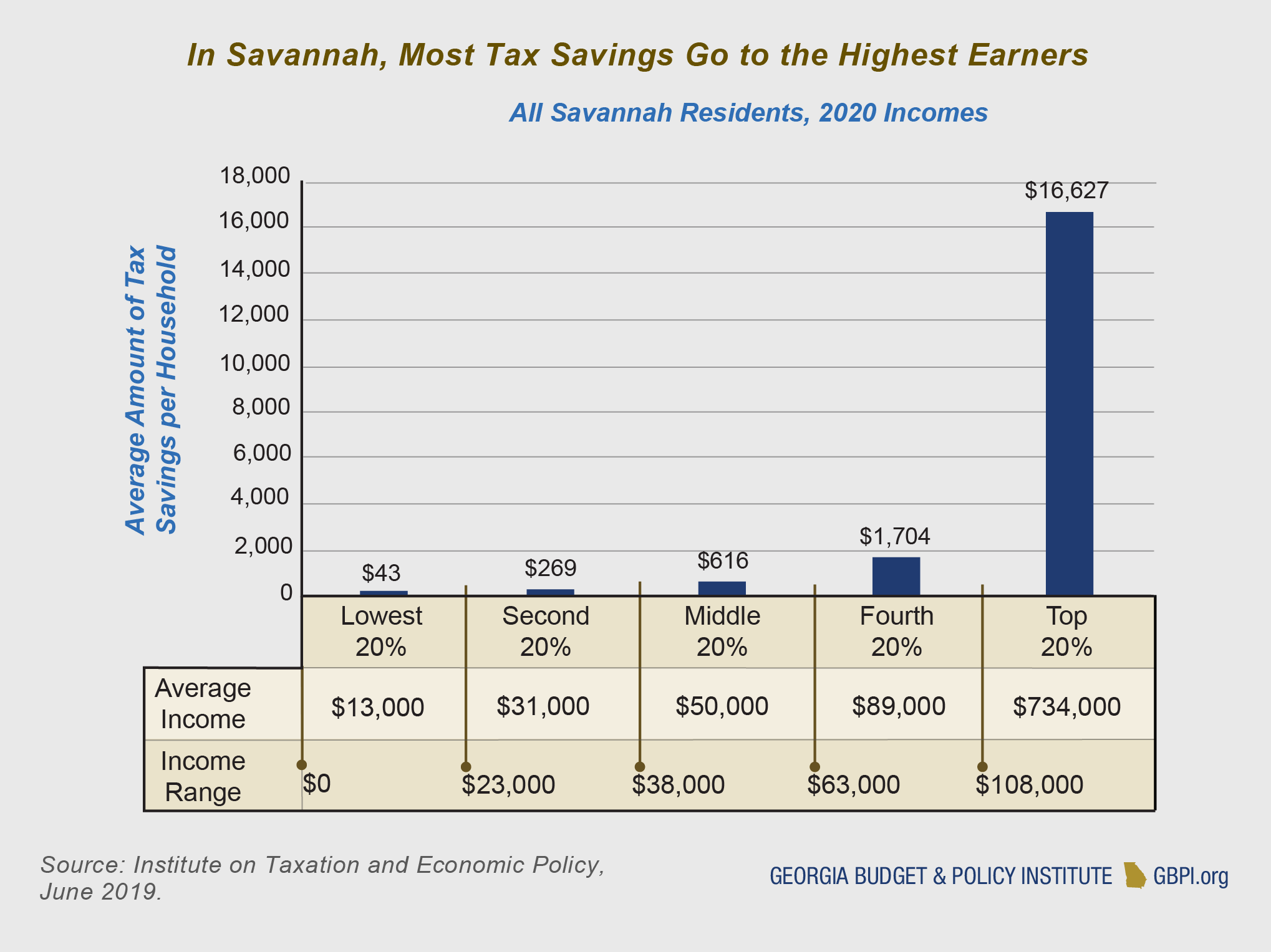

In partnership with Step Up Savannah and the Institute on Taxation and Economic Policy (ITEP), the tax changes facing more than 90,000 filers across nine zip codes throughout the City of Savannah were considered to determine how TCJA and Georgia’s state tax changes will impact residents and businesses.[29]

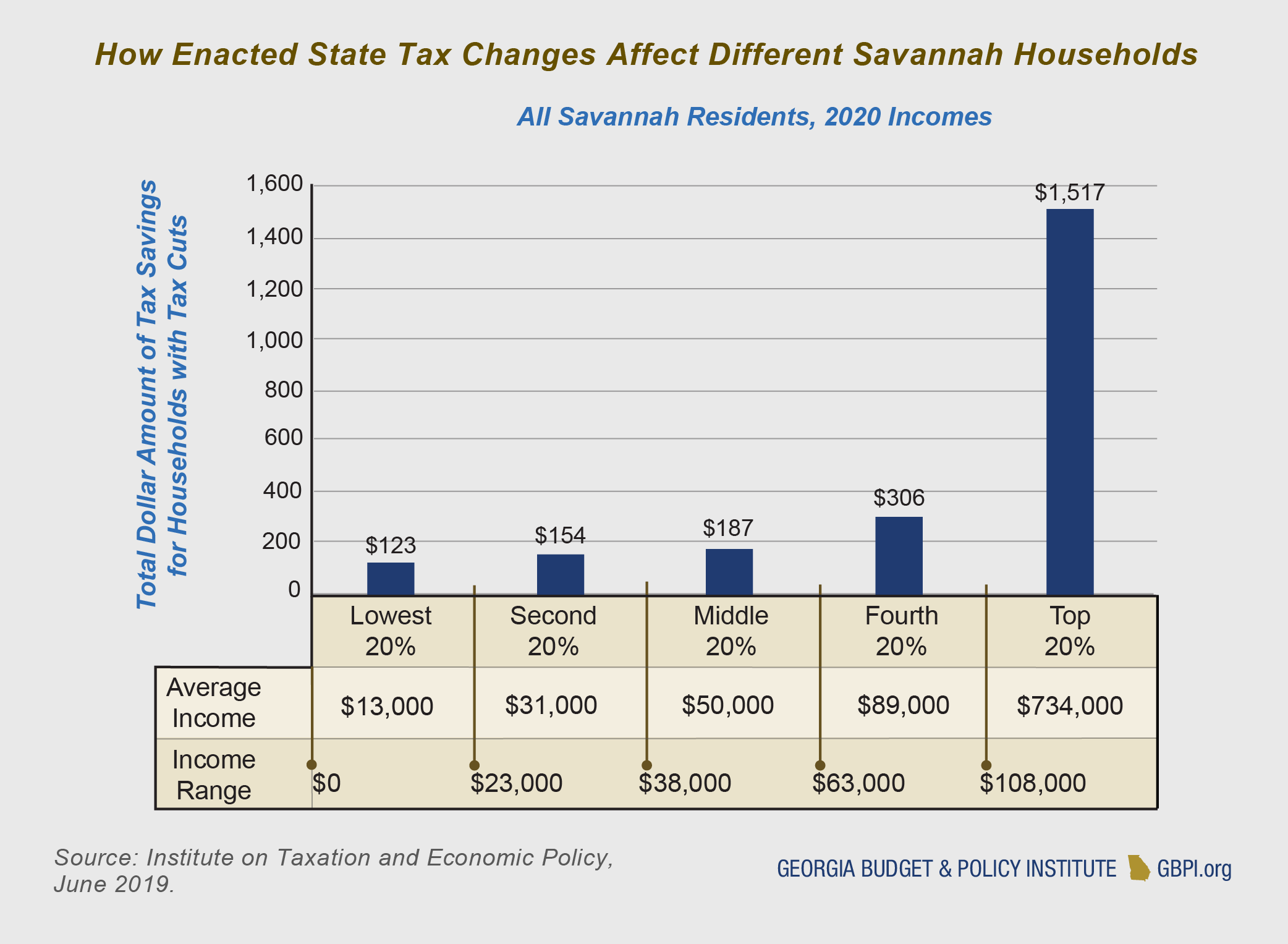

In sum, the federal tax changes will reduce taxes for Savannah residents by $342 million in 2020. These benefits disproportionately favor upper-income families, with about 85 percent of tax cuts going to residents with incomes higher than $108,000 annually, or the top 20 percent of Georgia earners. The remainder, approximately $50 million of annual tax cuts through 2025, will be distributed among the other 80 percent of Savannahians.

The enacted provisions of Georgia’s state tax changes, Phase 1, reduce taxes for 85 percent of Savannah residents. However, the vast majority (71 percent) of benefits will go to those in the top 20 percent of taxpayers.

The enacted provisions of Georgia’s state tax changes, Phase 1, reduce taxes for 85 percent of Savannah residents. However, the vast majority (71 percent) of benefits will go to those in the top 20 percent of taxpayers.

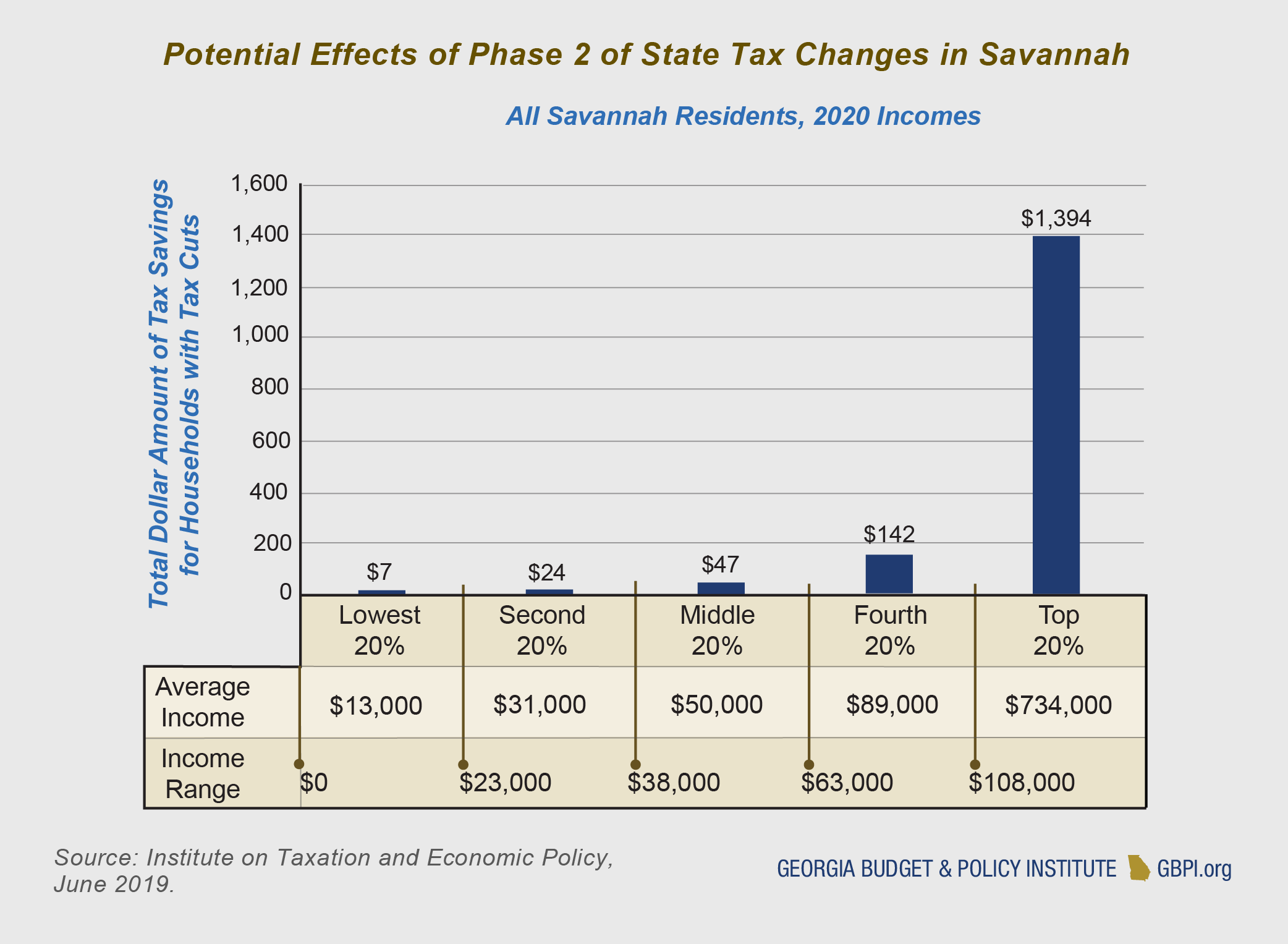

If the measure pending in the General Assembly to further reduce the income tax (Phase 2) is adopted in 2020, it would mean $27 million in new state tax cuts for Savannahians. However, more than 90 percent of these benefits would go to those who fall into the state’s top bracket of incomes.

If the measure pending in the General Assembly to further reduce the income tax (Phase 2) is adopted in 2020, it would mean $27 million in new state tax cuts for Savannahians. However, more than 90 percent of these benefits would go to those who fall into the state’s top bracket of incomes.

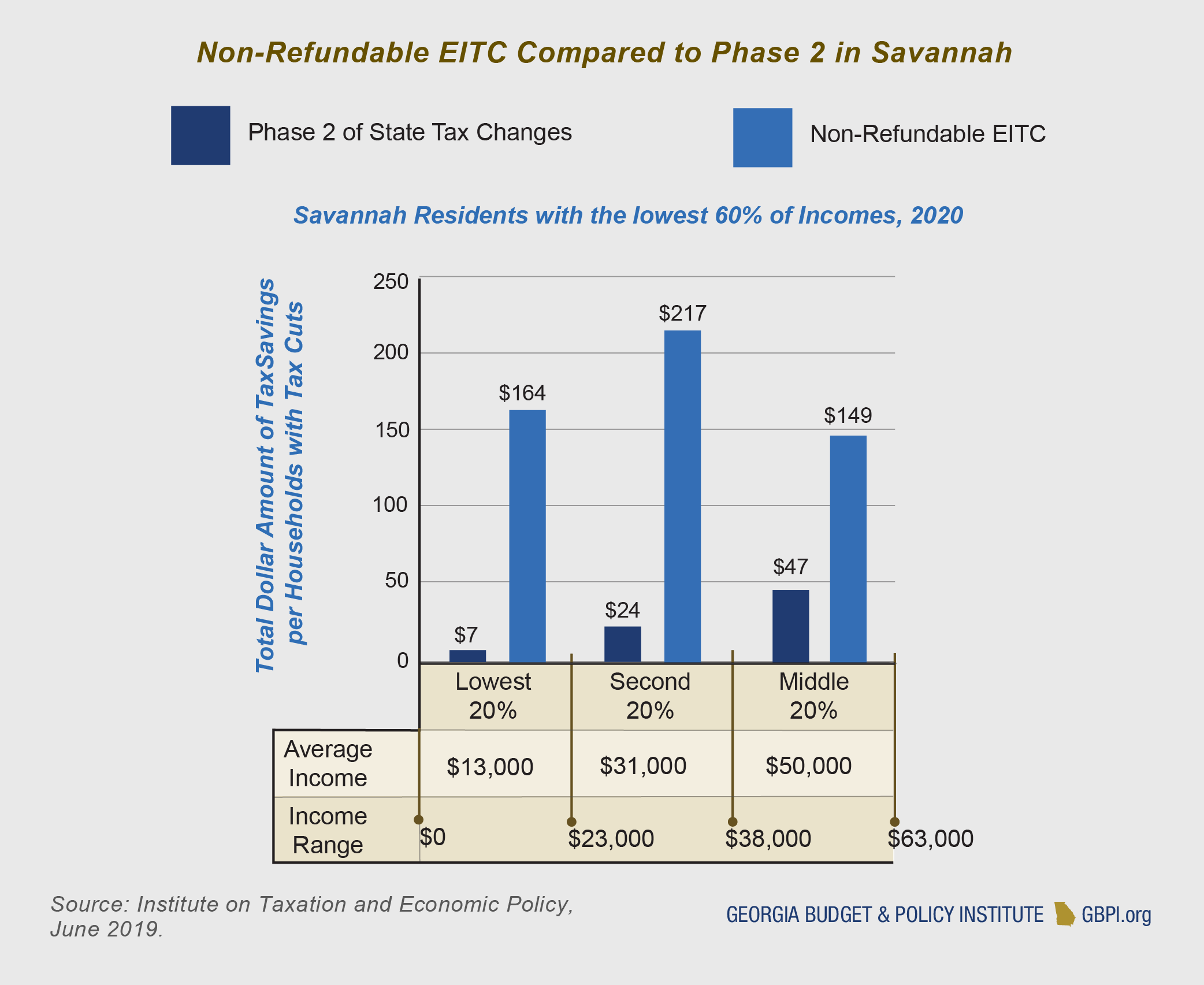

Members of the General Assembly are also considering adding an Earned Income Tax Credit (EITC) to the state’s tax code. This EITC would reward work, while avoiding the benefits cliff that can penalize low-income beneficiaries for earning even small wage increases.

Members of the General Assembly are also considering adding an Earned Income Tax Credit (EITC) to the state’s tax code. This EITC would reward work, while avoiding the benefits cliff that can penalize low-income beneficiaries for earning even small wage increases.

Methodology

Methodology

The Tax Cuts and Job Act (TCJA) makes significant changes to the federal tax code that will transform how both the state and federal government collect income taxes from individuals, families and businesses. TCJA was signed into law in December 2017 and most of its provisions expire in 2025. This report relies on data projecting the impact of TCJA from 2020–2025 prepared by the Institute on Taxation and Economic Policy (ITEP), and supplements this data using available information from the IRS, Georgia Department of Revenue, the Governor’s Office of Planning and Budget, the state auditor and Georgia State University’s Fiscal Research Center.

Effects of the Tax Cuts and Jobs Act (TCJA) in Georgia

The Institute on Taxation and Economic Policy (ITEP) partnered with GBPI to provide the data used to estimate the effects of TCJA in Georgia. ITEP’s analysis considered TCJA’s effects on 5,039,100 unique Georgia tax filers and 90,600 filers in the City of Savannah. The local analysis in Savannah considered the following zip codes: 31401, 31404, 31406, 31408, 31411, 31419, 31405, 31410 and 31415.

Definition of Income

There are two broad ways in which a distributional analysis can sort taxpayers by income level. One approach, used by legislative fiscal analysts in most states, uses income definitions based on “Adjusted Gross Income.” In this approach, the starting point is the income that is subject to income taxes in a given state. The other approach, used by ITEP, is to use a more universal income definition, including both income that is subject to tax and income that is exempt.

For components of income that are subject to income taxes, ITEP relies on information from the Internal Revenue Service’s “Statistics of Income” publication, which provides detailed state-specific information on components of income at different income levels. For components of income that are either fully or partially tax-exempt, ITEP uses data from the Congressional Budget Office and the Current Population Survey to estimate income levels in each state. The generally non-taxable income items for which ITEP makes state-by-state estimates (which are included in our measure of “total income”) include: Social Security benefits, Worker’s Compensation benefits, unemployment compensation, VA benefits, child support, financial assistance, public assistance and supplemental security income.

It is widely understood that taxpayers at all income levels tend to underreport certain income categories, especially capital gains, pass-through business income, rental income and farm income. For this reason, ITEP’s model estimates the amount of unreported income of each type in each state. These estimates are based on data from a series of Internal Revenue Service research reports that measure the income “tax gap”—the difference between the amounts of various types of income that are reported for tax purposes each year and the (larger) amounts that are earned. The tax gap is primarily the result of underreporting by taxpayers. This unreported income is included in our “total income” estimates for each state.

This comprehensive approach to measuring income is more informative than the “Adjusted Gross Income” approach for two critical reasons. Different states can use very different income tax rules, so “Adjusted Gross Income” is a concept that can have different meaning depending on the state. Moreover, large amounts of income are excluded from Adjusted Gross Income entirely, even though these income sources represent a meaningful element in a taxpayer’s “ability to pay.” If the goal is to express the impact of a tax change in relation to a taxpayer’s ability to pay it, the only accurate way of doing so is to express these tax changes as a share of total income, rather than Adjusted Gross Income.

Corporate Tax Cuts

When estimating the impact of corporate tax changes, ITEP uses revenue estimates from the Joint Committee on Taxation (JCT) for guidance on a provision’s overall impact and then calculates the distribution of benefits or costs among taxpayers. ITEP follows JCT’s approach in assuming that in the short run, a corporate tax cut will benefit the owners of corporate stocks alone, but in the long run (usually assumed to be ten years after enactment) a quarter of the benefits will flow to workers.

ITEP differs from JCT in that ITEP has updated their approach to account for new research that finds 35 percent of American corporate stocks are owned by foreign investors, a larger fraction than were previously assumed. This means that whatever portion of benefits flows to owners of corporate stocks (100 percent in the short-run, three-fourths in the long-run), one can assume that 35 percent of that amount flows to foreign investors.

This approach to corporate tax changes is applied to provisions that entirely affect C corporations (companies that pay the corporate tax), such as the reduction in the corporate income tax rate. For provisions that affect both C corporations and pass-through businesses, this approach is applied to the portion of the provision’s tax cut or tax hike that would fall on C corporations.[30]

ACA Individual Mandate

To estimate the effects of repealing the ACA’s individual mandate to obtain health insurance, ITEP begins with CBO’s estimates of the change in tax revenue that would result from this provision. ITEP estimates the effects across income groups using the distribution of penalty payments paid and premium tax credits received in each state according to the most recent IRS data.[31]

Endnotes

[1] “Analysis of State Individual Income Taxes,” Georgia Department of Audits and Accounts, December 2015.

[2] Institute on Taxation and Economic Policy, July 2019.

[3]“Deal comes up with money to fully fund Georgia K-12 schools next year,” The Atlanta Journal-Constitution, March 2018.

[4] House Bill 918 included a provision that authorizes the general assembly to reduce the state’s top income tax rate to 5.5 percent with the passage of a joint resolution that is signed by the governor on or after January 13, 2020.

[5] “Federal deficit jumps to $749B, likely to exceed $1T by September,” The Hill. July 2019.

[6] “Georgia’s Tax Expenditure Report for FY 2020,” Department of Audits and Accounts. December 2018

[7] “Georgia’s Rankings Among the States: Budget, Taxes and Other Indicators,” Georgia State University Fiscal Research Center. January 2019.

[8] Internal Revenue Service Data Book, 2018.

[9] “The New 2019 Federal Income Tax Brackets and Rates,” Forbes. December 2018.

[10] “Analysis of State Individual Income Taxes,” Georgia Department of Audits and Accounts. December 2015.

[11] “Georgia’s Taxes: A Summary of Major State and Local Government Taxes,” Georgia State University Fiscal Research Center. January 2019.

[12]. “Fiscal Note House Bill 918 (LC 34 5383-ECS,),” Department of Audits and Accounts. February 2018.

[13] Institute on Taxation and Economic Policy, June 2019.

[14] “Analysis of State Individual Income Taxes,” Georgia Department of Audits and Accounts. December 2015.

[15] Institute on Taxation and Economic Policy, February 2019.

[17] “Corporate Tax Avoidance Remains Rampant Under New Tax Law,” Institute on Taxation and Economic Policy. April 2019.

[18] “Georgia’s Taxes: A Summary of Major State and Local Government Taxes,” Georgia State University Fiscal Research Center. January 2019.

[19] ACS 5 Year Estimates 2013-2017. U.S. Census Bureau.

[20] Total Marketplace Enrollment,” Kaiser Family Foundation. July 2019.

[21] Internal Revenue Service Data Book, 2018.

[22] “The Economic Effects of the 2017 Tax Revision: Preliminary Observations,” Congressional Research Service. June 2019.

[23] “U.S. Economy Slows, Denying Trump 3% Talking Point,” The New York Times. June 2019.

[24] Governor’s Budget Report Fiscal Year 2020, Georgia Budgets in Brief 2010-2019.

[25] “FOMC statement after July interest rate cut,” MarketWatch. July 2019.

[26] “Comparative Summary of State General Fund Receipts (unaudited) For the Month Ended June 2019,” Georgia Department of Revenue. July 2019.

[27] Institute on Taxation and Economic Policy, June 2019.

[28] The poorest fifth of Georgia taxpayers pay an average 10.7 percent of their annual income in state and local taxes, the middle fifth pays 9.8 percent, while the wealthiest 1 percent pays only 7 percent. (“Who Pays? A Distributional Analysis of the Tax Systems in All 50 States,” Institute on Taxation and Economic Policy. October 2018.)

[29] Institute on Taxation and Economic Policy, June 2019; Savannah zip codes include: 31401, 31404, 31406, 31408, 31411, 31419, 31405, 31410 and 31415. The data set includes estimated tax information for over 90,000 residents.

[30] Institute on Taxation and Economic Policy, August 2019.

[31] Ibid.