This piece was co-authored by Ashley Young and Daniel Kanso, PhD

![]()

Introduction

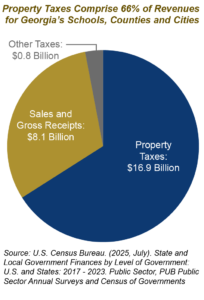

Property taxes are the primary source of revenue for Georgia’s local governments, including school districts, raising about two-thirds (66%) of $25.8 billion in total tax revenue in 2023.[1] State lawmakers are considering whether to radically change the way Georgia’s local governments and schools raise revenue by eliminating or significantly reducing property taxes on owner-occupied residential homes, which are known as homesteaded properties. These measures largely propose substituting property taxes for sales taxes.[2]

Property taxes are the primary source of revenue for Georgia’s local governments, including school districts, raising about two-thirds (66%) of $25.8 billion in total tax revenue in 2023.[1] State lawmakers are considering whether to radically change the way Georgia’s local governments and schools raise revenue by eliminating or significantly reducing property taxes on owner-occupied residential homes, which are known as homesteaded properties. These measures largely propose substituting property taxes for sales taxes.[2]

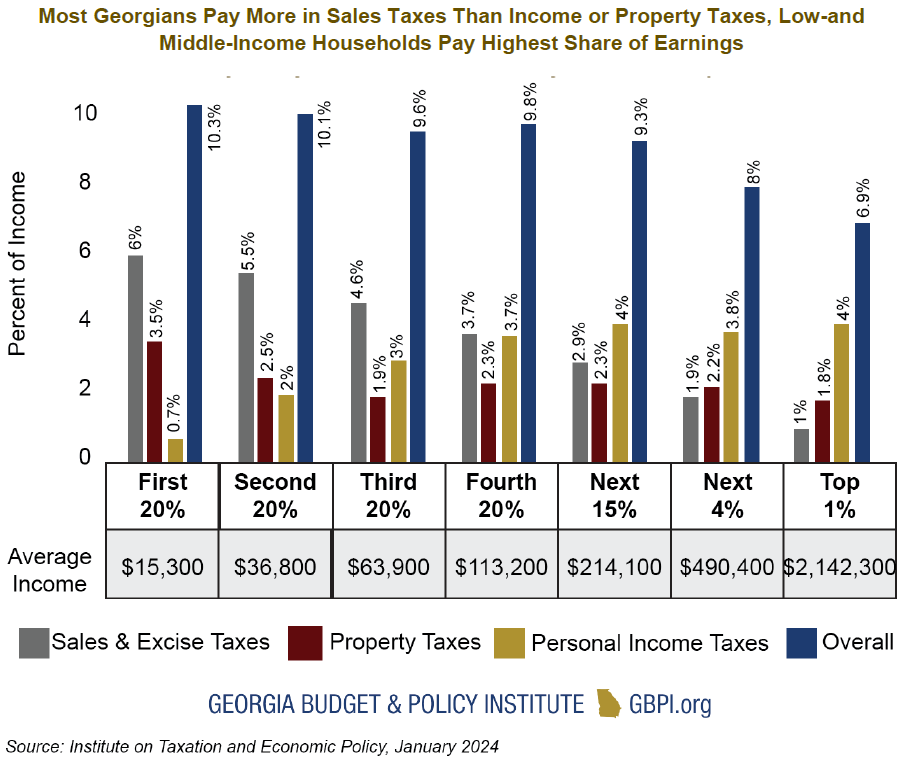

On average, sales taxes already consume a larger share of earnings than property taxes for approximately 95% of households across Georgia.[3] Replacing property taxes with sales taxes is likely to raise the cost of living and would do little to address broader affordability concerns for most Georgians.

Leading estimates show Georgia’s local governments, including school districts, cities and counties, generate between $6.6 billion to $8.7 billion in revenue from homesteaded residential properties, which include about 65% of homes statewide.[4] Property taxes are stable, simple and economically efficient ways of raising needed revenues for schools and local governments. Residential property taxes also recognize that homeowners receive significant benefits from public services and should be taxed fairly to help fund those services at the local level.

Property Taxes Enable Schools, Counties and Cities to Balance Budgets

Entirely offsetting revenues lost from residential homesteaded property taxes would likely require doubling local sales tax revenues, which raised about $8.1 billion or 31% of local taxes statewide in 2023.[5] Currently, sales taxes average 7.42% statewide, split between a 4% state sales tax and combined local sales tax rates of up to 5%.[6] Regressive taxes push working and middle-income Georgians to pay a higher share of what they make in taxes. Although both property taxes and sales taxes are regressive, shifting from property taxes to sales taxes would likely cause low-to middle-income Georgians to pay an even higher share of what they earn in taxes.

Under Georgia’s current property tax system, homeowners are eligible for homestead exemptions, which allow Georgians who own and occupy their primary residence to exempt a share of their home’s value from property taxes. Although Georgia eliminated its state property tax in 2015, a homestead exemption of $2,000 in assessed value is available statewide. This is complemented by local homestead exemptions that range in value and eligibility criteria. Additional statewide exemptions are available for some Georgians, including low-income seniors, disabled veterans and surviving spouses of disabled veterans, officers and firefighters.[7] In 1999, lawmakers also created the Homeowner Tax Relief Grant, which has since been used to deliver one-time homestead exemptions of up to $18,000 for county, city and school property taxes through state appropriations. In the Amended Fiscal Year (AFY) 2026 budget, lawmakers allocated $850 million for this program, which is estimated to reduce homesteaded property taxes by an average of $500.[8]

About 56% ($11.1 billion) of $19.9 billion raised from statewide property taxes funded schools in 2024, while the remainder funded local services provided by cities and counties.[9] This $11.1 billion in property tax collections accounted for 72% of all local revenues raised by school districts.[10] Unlike volatile sales taxes, which are likely to fluctuate with economic conditions, property taxes are a more stable source of funding for schools.[11]

Overall, one-third (34%) of $32.3 billion in total K-12 education funding (2024) is raised through property taxes, a figure that is in line with best practices.[12] Of this $11.1 billion total, about $6.7 billion is raised statewide for schools from residential property taxes, with most of that revenue coming from homesteaded properties.[13] The remaining $4.4 billion in school property taxes is raised from other categories of property, including commercial, industrial, agricultural and utilities.

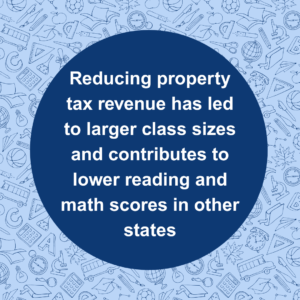

Eliminating homesteaded property taxes would significantly impact K-12 public school funding. Historically, measures reducing property tax revenues in other states led to larger class sizes and higher student-to-teacher ratios, which can negatively affect instructional quality and student success.[14] Studies show revenue losses from property tax cuts contribute to declining student outcomes, specifically in reading and math scores.[15] Reduced property tax revenues can also can cause cuts in staffing and resources for support services such as counselors, social workers, librarians and nurses.[16]

Eliminating homesteaded property taxes would significantly impact K-12 public school funding. Historically, measures reducing property tax revenues in other states led to larger class sizes and higher student-to-teacher ratios, which can negatively affect instructional quality and student success.[14] Studies show revenue losses from property tax cuts contribute to declining student outcomes, specifically in reading and math scores.[15] Reduced property tax revenues can also can cause cuts in staffing and resources for support services such as counselors, social workers, librarians and nurses.[16]

Overall, Georgians paid $5,391 in per-person taxes in 2023, including $3,056 in state taxes and $2,335 in local taxes.[17] Although Georgia’s per person state taxes ranked 7th lowest nationally, local taxes ranked in the middle of the pack at 26th out of 50.[18] In part, this is a product of state policy decisions that have pushed localities to carry a higher share of spending for services to prioritize keeping state taxes low. Rather than mandating that local governments drastically rebalance their budgets to provide outsized tax cuts to some taxpayers and large tax increases to others, Georgia lawmakers should consider a more balanced approach that requires additional resources from the state. Unlike local governments, the state has a broad array of potential revenue sources available to help fund equitable tax cuts for most Georgians in addition to strengthening public schools.

Major Cost Shifts from State to School Districts Contribute to Increased Reliance on Property Taxes

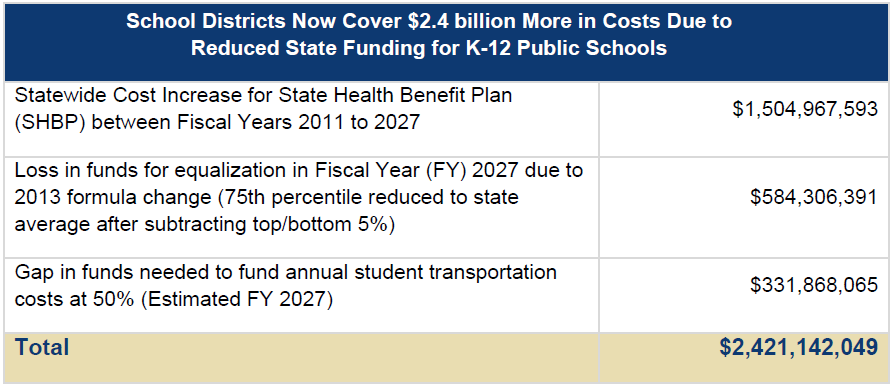

Recent state budget cuts reducing funding for public education are one of the primary forces adding pressure to residential property taxes in Georgia. As the state of Georgia has substantially reduced its funding commitments for schools through health care costs, the equalization formula and student transportation, school districts have stepped up to fill the gap, which amounts to an estimated $2.4 billion in Fiscal Year (FY) 2027. In 2014, the state funded 51% of K-12 education costs.[19] By 2024, the state’s investment declined to 40% of total costs.[20] During this period, local school districts increased their share of total education spending from 41% to 48%, while a smaller increase in federal funding helped to make up the remainder of the gap left by the state.

After passing upwards of $2.4 billion in annual costs on to school districts, state lawmakers are seeking to further intervene by restricting how local schools raise funds to balance their budgets. These cost shifts to local districts have added upward pressure to property taxes because school districts have few other options to raise the revenues needed to educate students. Instead of mandating that local governments shift from raising revenue through property taxes to raising revenue through more regressive sales taxes, Georgia’s leaders could restore state funding for school employee health insurance costs, equalization and transportation. Increasing state funding for schools could help to reduce local reliance on residential property taxes without compromising the educational opportunities available to students.

Major Property Tax Measures Under Consideration During 2026 Legislative Session

House Resolution (HR) 1114 and House Bill (HB) 1116

HR 1114 and HB 1116 would dramatically change the way local governments and schools raise revenue by reducing residential homesteaded property taxes by 75% between 2027 and 2037.[21] This would be accomplished by reducing statewide assessments by three percentage points annually and eventually reducing property tax assessments from 40 percent of market value down to 10 percent of market value. Local governments and schools would be expected to turn to raising revenue by increasing sales taxes, likely raising taxes for working and middle-class Georgians.

Serious questions remain over how local sales taxes could raise enough revenue to eliminate residential homesteaded property taxes statewide without deep budget cuts. To make up part of the gap, the legislative package would create a Homeowner’s Tax Relief Fund by designating approximately $760 million in sales tax revenue raised from data centers to provide grants to counties, municipalities and school systems.[22]

Rather than shifting from one regressive tax in the property tax to another even more regressive tax through the sales tax, legislators could consider funding property tax relief grants by allocating state funds to unwind the recession-era cuts made to public schools. Ultimately, substituting property taxes with sales taxes would do little to address affordability concerns for most Georgians, while risking the possibility of widespread tax increases and heightened volatility from year-to-year. However, the state-funded component of the legislative package may provide an opportunity for compromise by recognizing that additional state resources are required to enable meaningful property tax relief.

Senate Resolution (SR) 811 and Senate Bill (SB) 530

SR 811 and SB 530 dedicate $2.8 billion in state and local revenues from data centers and insurance companies to finance property tax circuit breaker grants for renters and homeowners.[23] These same measures were also introduced as HB 1468 and HR 1503. Property tax circuit breakers would help to ensure that costs from property taxes and homeowners insurance, as well as rent, do not become unaffordable for working and middle-income Georgians.

The legislative package dedicates revenues from the state’s existing insurance premium tax, in addition to revenues raised from eliminating the tax break for high-tech data center equipment, along with tax breaks for insurance abatements and special deductions for life insurance companies. Based on FY 2027 estimates, this bill would dedicate $2.2 billion in state revenues (including $1.4 billion from the insurance premium tax and $760 million from data centers) in addition to $645 million in local data center revenues.[24]

The package funds two programs. First, through the Georgia Property Tax Fairness Credit program, the state would issue refundable tax credits of up to $2,500 to ensure that working and middle-income Georgians do not spend more than 5% of their income on property taxes and homeowners’ insurance or more than 33% of their income in rent. Second, at the local level, revenues from data center sales taxes would be dedicated to increasing residential homestead exemptions.

This bill is revenue-neutral and delivers property tax cuts and relief for renters without passing the buck to school systems or local governments. It is also structured to make up for revenue losses school systems have seen with $2.2 billion in new state funding. Importantly, the primary mechanism for property tax and renter relief is financed at the state level, allowing local governments needed flexibility if revenue projections for data centers and insurance companies change in the future.

Senate Bill 382

SB 382 removes the option for local governments and school districts to opt out of the statewide Georgia Local Option Property Tax Exemption that was enacted in 2024.[25] When voters approved the constitutional amendment established through HR 1022 (2024) and enabled by HB 581 (2024) and HB 92 (2025), Georgia created a floating statewide homestead exemption to restrict taxable home values (also called assessed values) from increasing above the rate of inflation from year-to-year.

However, when given the option to opt out, 68% of school districts and 30% of counties decided not to enact the measure, citing funding concerns.[26] SB 382 would unilaterally pull the rug out from under school districts and local governments that have already made clear they cannot afford the revenue losses that would accompany a cap on taxable home values. Instead of passing another unfunded mandate down to the local level, Georgia’s leaders would be wise to focus on allocating additional state resources to finance equitable property tax reductions for both owners and renters.

Appendix: K-12 Public Education Impact of Recent State Budgetary Decisions Shifting Expenses to School Districts

Property tax policy is inextricably linked to public school funding. Over the past two decades, school leaders have navigated large scale policy changes driven at the state level. As a result, schools have become more reliant on property taxes. Three areas, including increased State Health Benefit Plan (SHBP) costs, reduced equalization grants and shouldering a higher share of student transportation costs have contributed to a $2.4 billion increase in education costs paid by school districts annually. These policy changes have resulted in less funding over time from the state to school districts, causing negative impacts on day-to-day operations for Georgia’s public schools.

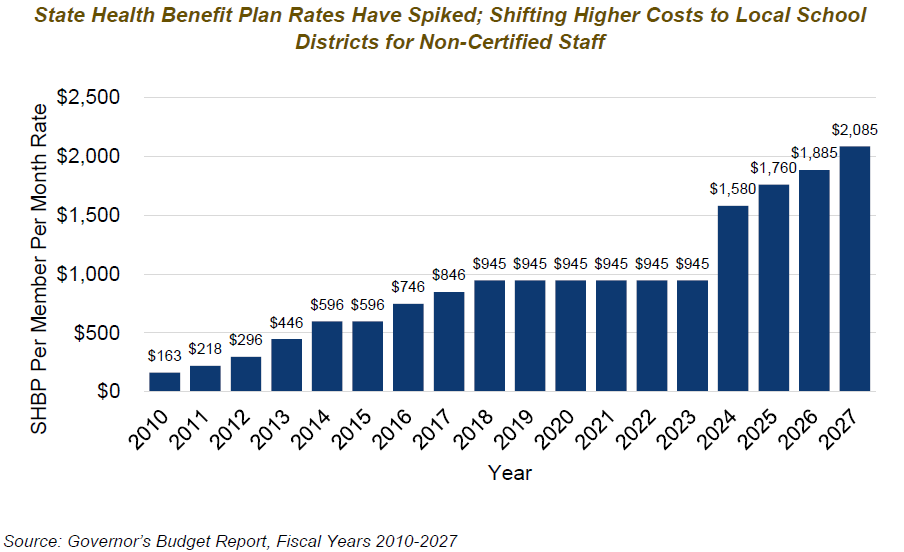

State Health Benefit Plan

The State Health Benefit Plan is the state’s health insurance coverage for teachers and public school employees in Georgia. In 2011, state lawmakers made significant cuts to funding for SHBP coverage of “non-certified” or “classified” school district employees, such as bus drivers, nurses, nutrition workers and custodians. Schools pay the employer share of health insurance premiums for an estimated 62,300 classified employees in addition to about 4,900 locally paid educators for a total of 67,200 employees.

In FY 2023, the per member per month (PMPM) rate for non-certified staff spiked from $945 to $1,580 in FY 2024. This change alone has caused considerable financial stress for local districts. In FY 2027, the per member per month (PMPM) rate is set to increase even further, growing by 8% from $1,885 to $2,028. Overall, annual costs per employee have increased from $1,953 (FY 2010) to $24,336 (FY 2027). In total, school districts will pay $1.5 billion more for SHBP costs for their employees in FY 2027 due to cost increases since FY 2010.

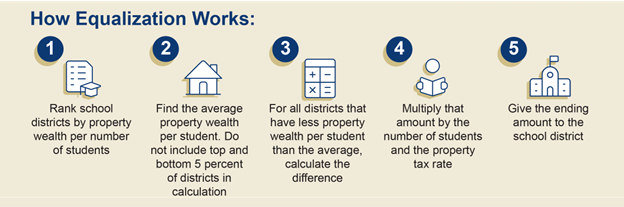

Equalization Grants

When Georgia’s Quality Basic Education (QBE) funding formula was adopted in 1985, the state equalized schools up to the 90th percentile of districts. This means that the state provided extra funds to less wealthy districts to help them nearly reach the funding levels raised by the wealthiest districts. In 2000, the legislature lowered the benchmark for equalization to the 75th percentile. After the Great Recession, Georgia lawmakers again lowered the equalization formula to where it sits currently: the state average after removing the top and bottom 5% of districts.

The FY 2027 budget includes $1.2 billion for equalization. A 25-percentage-point increase from the statewide average to the 75th percentile would cost at least $584 million. If the state invested resources to bring all school districts to the 75th percentile, these funds would help to level the playing field and ensure that all districts can provide the same standard of public education statewide.

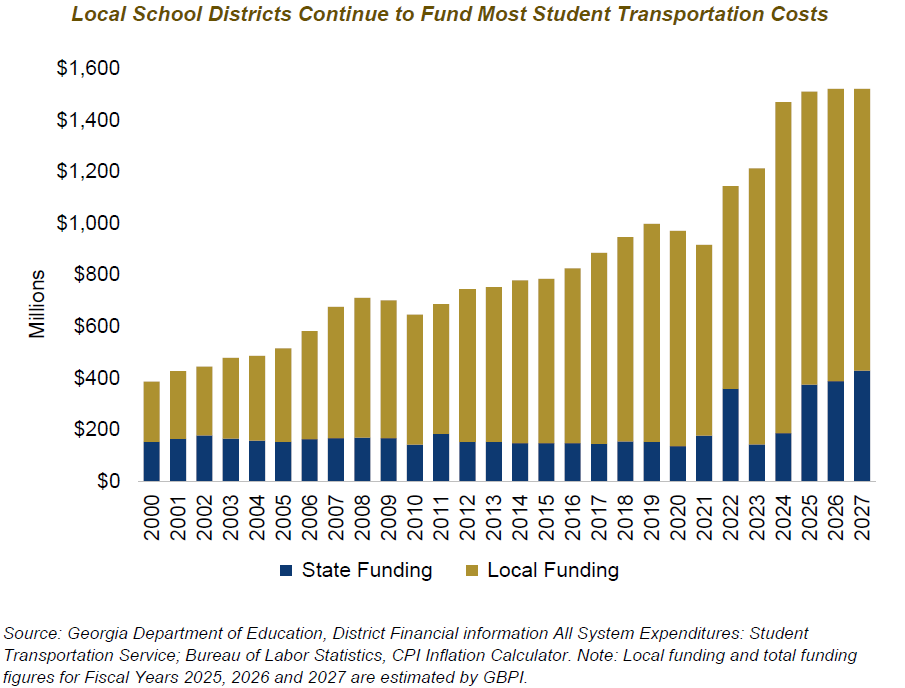

Student Transportation

In Georgia, over 930,000 students, or approximately 53% of all K-12 public school students, ride the school bus.[27] Historically, the state paid 49% of transportation costs under the QBE formula dating back to 1996.[28] However, over time, Georgia has invested considerably less funding for student transportation, leaving school districts to bridge the gap. Although the state has made progress to increase formula funding for student transportation from $163.2 million in FY 2024 to $402.6 million proposed in Gov. Kemp’s FY 2027 budget, a significant gap remains to restore a 50-50 state and local split.[29]

In FY 2027, the state plans to contribute about 28% of $1.52 billion in estimated student transportation costs through $402 million in recurring funding and $25 million in one-time funds to replace 270 school buses.[30] Closing the student transportation funding gap to 50% would cost at least $332 million annually in additional state funding.[31] This change could also help school districts to refocus resources from covering essentials to investing in strengthening instruction and offering more educational opportunities to students.

Endnotes

[1] U.S. Census Bureau. (2025, July). State and local government finances by level of government: U.S. and states: 2017 – 2023. Public sector, PUB public sector annual surveys and Census of governments, table GS00LF01. https://data.census.gov/table/GOVSTIMESERIES.GS00LF01?q=Local+Government+Finances&g=010XX00US,$0400000&nkd=GOVTYPE~003,time~2023&tableFilters=GEO_ID~VALUES(0400000US13)

[2] House Resolution 1114, as passed the Ways & Means Committee, March 3, 2026; House Bill 1116, as passed the Ways & Means Committee, March 3, 2026; Senate Bill 382 as passed by the Senate, February 3, 2026; Georgia House Budget and Research Office. (2024, July). House Bill 581 Property tax relief and reform for Georgians. https://www.legis.ga.gov/api/document/docs/default-source/house-budget-and-research-office-document-library/newsandhighlights/2024/2024_policy_brief_hb_581_property_tax_reform.pdf

[3] Kanso, D. (2025, November 17). Breaking the bank: Eliminating the state income tax harms most Georgians and increases the cost of living. Georgia Budget & Policy Institute. https://gbpi.org/breaking-the-bank-eliminating-the-state-income-tax-harms-most-georgians-and-increases-the-cost-of-living/?_gl=1*xqing0*_up*MQ..*_ga*MTg4NTYyMDQzNy4xNzY0NjA4NDky*_ga_ZWZC5HZ1YJ*czE3NjQ2MDg0OTIkbzEkZzEkdDE3NjQ2MDg1MDkkajQzJGwwJGgw#_edn15

[4] U.S. Census Bureau. (2025, September). Mortgage status by aggregate real estate taxes paid (dollars). American community survey, ACS 1-Year estimates detailed tables, table B25090, https://data.census.gov/table/ACSDT1Y2024.B25090?q=B25090&g=010XX00US$0400000&y=2024&tp=true; U.S. Census Bureau. (2025, March 28). Current population survey/housing vacancy survey; ACCG. (2026, March 3). 2026 Property tax reform: HR 1114 and HB 1116. https://www.accg.org/page.php?ID=2345

[5] U.S. Census Bureau. (2025). State and local government finances by level of government: U.S. and states: 2017 – 2023. Public sector, PUB public sector annual surveys and Census of governments, Table GS00LF01. https://data.census.gov/table/GOVSTIMESERIES.GS00LF01?q=Local+Government+Finances&g=010XX00US,$0400000&nkd=GOVTYPE~003,time~2023&tableFilters=GEO_ID~VALUES(0400000US13)

[6] Kanso, D. (2025, November 17). Breaking the bank: Eliminating the state income tax harms most Georgians and increases the cost of living. Georgia Budget & Policy Institute. https://gbpi.org/breaking-the-bank-eliminating-the-state-income-tax-harms-most-georgians-and-increases-the-cost-of-living/?_gl=1*xqing0*_up*MQ..*_ga*MTg4NTYyMDQzNy4xNzY0NjA4NDky*_ga_ZWZC5HZ1YJ*czE3NjQ2MDg0OTIkbzEkZzEkdDE3NjQ2MDg1MDkkajQzJGwwJGgw#_edn15

[7]Georgia Department of Revenue. (n.d.). Property tax homestead exemptions. https://dor.georgia.gov/property-tax-homestead-exemptions

[8] House Bill 973, as signed by Gov Kemp.

[9] Georgia Department of Revenue. (2026, January 16). 2025 Property tax administration annual report.

[10] Georgia Department of Education. (n.d.). District financial information, system revenues. https://georgiainsights.gadoe.org/dashboards/district-financial-information/

[11] Baker, B. D., M. Di Carlo, and Z.W. Oberfield. (2023). The source code: Revenue composition and the adequacy, equity, and stability of K-12 school spending. Albert Shanker Institute. https://eric.ed.gov/?q=source%3A%22Albert+Shanker+Institute%22&id=ED629096

[12] Georgia Department of Revenue. (2026, January 16). 2025 Property tax administration annual report; Georgia Department of Audits and Accounts. (2024, November). School system spending. https://www.audits.ga.gov/ReportSearch/download/31860?_gl=1*j4mi20*_ga*MTYxMDM1NDExNy4xNzMzMTg2ODQ2*_ga_8Z4RV13R5J*MTczMzE4Njg0Ni4xLjAuMTczMzE4Njg0Ni4wLjAuMA..*_ga_65FL79Y113*MTczMzE4Njg0Ni4xLjAuMTczMzE4Njg0Ni42MC4wLjA; Georgia Department of Education. (n.d.). District financial information, system revenues. https://georgiainsights.gadoe.org/dashboards/district-financial-information/

[13] Ibid.

[14] Figlio, D.N. (1998, March). Short-term effects of a 1990s-era property tax limit: Panel evidence on Oregon’s Measure 5. National Tax Journal 51, no. 1: 55–70. https://doi.org/10.1086/NTJ41789311

[15] Sorensen, L., Y. Kim, and M. Hwang. (2021, September). The distributional effects of property tax constraints on school districts. National Tax Journal 74:3, 621-654. https://doi.org/10.1086/716231

[16] Nguyen-Hoang, P., and P. Zhang. (2022, January 1). Cap and gap: The fiscal effects of property tax levy limits in New York. Education Finance and Policy 17, no. 1: 1–26. https://doi.org/10.1162/edfp_a_00327

[17] U.S. Census Bureau. (2025, July). State and local government finances by level of government: U.S. and states: 2017 – 2023. Public sector, PUB public sector annual surveys and Census of governments, Table GS00LF01, 2025, https://data.census.gov/table/GOVSTIMESERIES.GS00LF01?q=Local+Government+Finances&g=010XX00US,$0400000&nkd=GOVTYPE~002,time~2023&tableFilters=GEO_ID~VALUES(0400000US13); U.S. Census Bureau. (2023, December 19). U.S. population trends return to pre-pandemic norms as more states gain population. https://www.census.gov/newsroom/press-releases/2023/population-trends-return-to-pre-pandemic-norms.html

[18] Georgia State University, Fiscal Research Center. (2026, January). Georgia’s rankings among the states. https://frc.gsu.edu/download/georgias-rankings-among-the-states-budget-taxes-and-other-indicators-2024-2/?ind=1767721287692&filename=Rankings%20Report%202026.pdf&wpdmdl=6425&refresh=695d4f544e1dc1767722836

[19] Young, A. (2026, February 12). Overview: 2027 fiscal year budget for K-12 education. Georgia Budget & Policy Institute. https://gbpi.org/overview-2027-fiscal-year-budget-for-k-12-education/

[20] Ibid.

[21] House Resolution 1114, as passed the Ways & Means Committee, March 3, 2026; House Bill 1116, as passed the Ways & Means Committee, March 3, 2026.

[22] Georgia Department of Audits & Accounts. (2026, January 12). Georgia tax expenditure report for FY 2027. https://opb.georgia.gov/budget-information/budget-documents/tax-expenditure-reports

[23] Senate Bill 530, as introduced, February 18, 2026; Senate Resolution 811, as introduced, February 18, 2026.

[24] Ibid.

[25] Senate Bill 382 as passed by the Senate, February 3, 2026

[26] Yushkov, A. and J. Johns. (2025, April 17). Localities opt out of Georgia’s new homestead tax exemption. The Tax Foundation. https://taxfoundation.org/blog/georgia-property-tax-reform/

[27] Writer, S. (2025, December 8). K-12 Student Transportation Statistics 2024-25. School Bus Fleet. https://www.schoolbusfleet.com/news/k-12-student-transportation-statistics-2024-25

[28] Suggs, Claire. (2017, January). School districts stuck with higher busing costs in proposed formula. Georgia Budget & Policy Institute. https://gbpi.org/wp-content/uploads/2017/01/ERC-Transportation-Fact-Sheet.pdf

[29] Office of Planning and Budget. (2024, June). Budget in brief, AFY 2024 and FY 2025, Governor Brian P. Kemp; Office of Planning and Budget. (2026, January). The governor’s budget report, AFY 2026 and FY 2027, Governor Brian P. Kemp.

[30] Office of Planning and Budget. (2026, January). The governor’s budget report, AFY 2026 and FY 2027, Governor Brian P. Kemp.

[31] Georgia Department of Education. (n.d.). District financial information, student transportation service. https://georgiainsights.gadoe.org/dashboards/district-financial-information/; Bureau of Labor Statistics. (n.d.). CPI inflation calculator, June 2024 to January 2026. https://www.bls.gov/data/inflation_calculator.htm